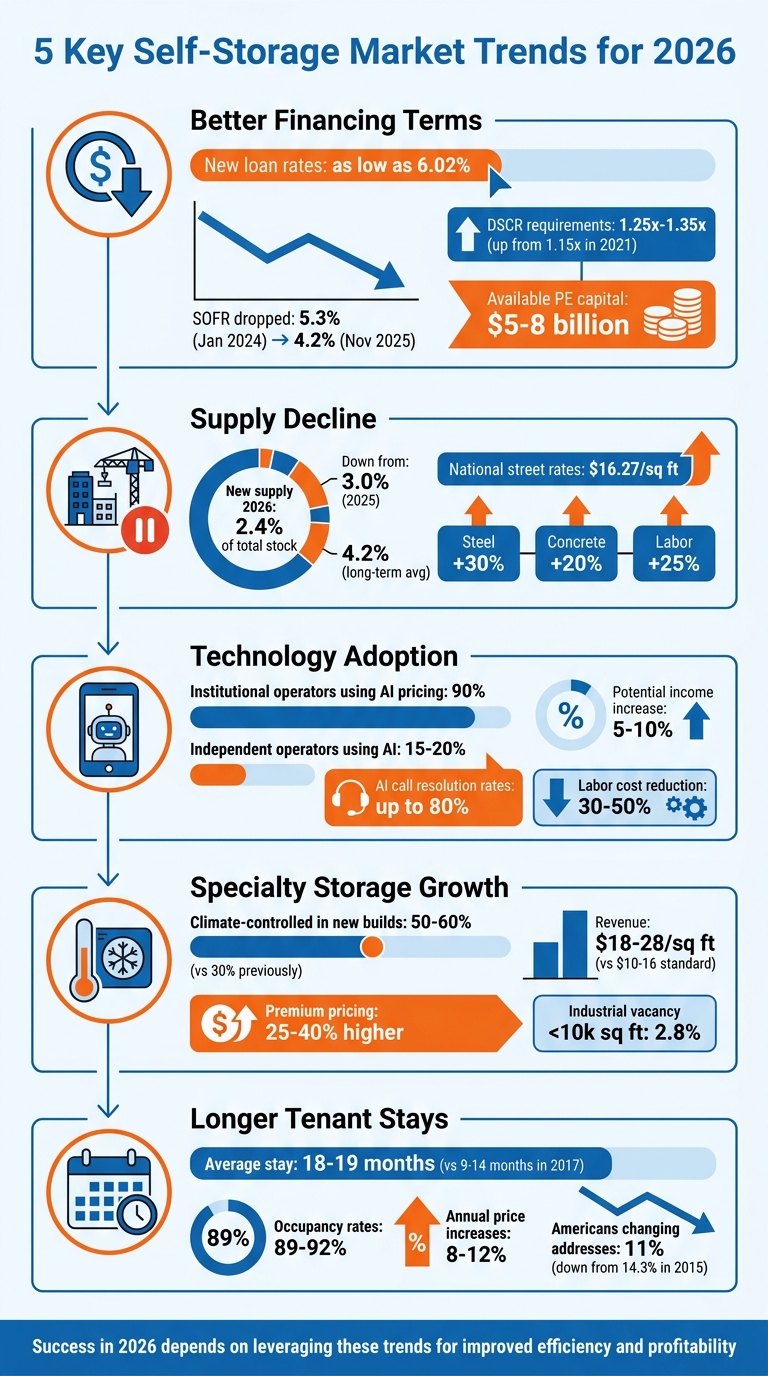

The self-storage industry is undergoing major shifts in 2026. Here’s what you need to know:

- Financing is improving: Borrowing costs are finally lower than yields, with loans as low as 6.02%. This opens up opportunities for acquisitions and refinancing.

- Construction is slowing: New supply is expected to drop to just 2.4% of total inventory, strengthening demand for existing facilities.

- Tech adoption is critical: Over 90% of institutional operators use AI-driven pricing, but only 15%–20% of independent facilities have caught up, leaving room for growth.

- Specialized storage is growing: Climate-controlled units now dominate new builds, offering 25%–40% higher rents. Specialty options like storage-industrial-flex condos are also emerging.

- Longer tenant stays: Average stays are now 18–19 months, with operators focusing on gradual rent increases and customer retention.

These trends highlight a shift toward smarter operations, better financing, and a stronger focus on customer needs. Success in 2026 will depend on leveraging these changes to improve efficiency and profitability while staying competitive in a tightening market.

5 Key Self-Storage Market Trends for 2026: Statistics and Opportunities

The Self Storage “Reversal” Starts in 2026

sbb-itb-09b4138

1. Better Financing Terms and Positive Leverage

For the first time in two years, borrowing costs have dipped below property valuation levels. New self-storage loans are being issued with rates as low as 6.02% [8], while the Secured Overnight Financing Rate (SOFR) dropped from 5.3% in January 2024 to 4.2% by November 2025 [11]. This change means debt can now boost the performance of deals instead of dragging them down. It’s a shift that’s influencing how deals are structured and how strategies are crafted in the market.

"This shift creates ‘positive leverage,’ where debt enhances a deal’s performance instead of weighing it down." – Ryan Gibson, Chief Investment Officer, Spartan Investment Group [8]

This shift in financing is also pushing overleveraged owners to sell, creating acquisition opportunities for buyers who can secure favorable terms and focus on properties with strong fundamentals.

Impact on Market Fundamentals

The return of positive leverage is transforming how deals are made. With cheaper capital, the gap between buyers and sellers is narrowing, leading to more transactions. For example, in April 2026, a self-storage facility in Island Park, New York, secured an $11.5 million recapitalization loan, demonstrating lenders’ continued interest in self-storage investments despite economic challenges [2].

Banks and private lenders now have significant liquidity and are actively pursuing self-storage investments [8]. However, underwriting standards have tightened. Debt service coverage ratios (DSCR) now range from 1.25x to 1.35x, up from 1.15x in 2021 [1]. This ensures that deals are supported by actual cash flow rather than overly optimistic rent growth projections.

Opportunities for Revenue Growth

Improved financing terms are directly aiding revenue growth by lowering debt servicing costs. Owners burdened by expensive bridge loans now have the chance to refinance under better terms, which can boost their net operating income (NOI) [2][8]. A 1% Federal Reserve rate cut between September 2025 and early 2026 has further accelerated this trend [3].

"The maturity wall that’s causing real pain for overleveraged owners is simultaneously creating one of the best acquisition windows the industry has seen in a decade." – White Label Storage [2]

Institutional investors are taking advantage of these conditions, as evidenced by recent multi-million-dollar deals. Private equity firms reportedly have between $5 billion and $8 billion in available capital earmarked for the sector [1]. Additionally, investors are targeting facilities still reliant on outdated systems, such as manual pricing and paper leases. By modernizing these properties, they can achieve incremental revenue increases of 5% to 10% [1].

Relevance to Self-Storage Owners and Investors

The combination of better financing terms and market distress is creating tangible opportunities. Investors can use positive leverage to focus on constrained locations with steady population growth while steering clear of oversupplied markets. On top of that, 100% bonus depreciation in 2026 offers a tax incentive, allowing investors to deduct a significant portion of property costs in the first year of acquisition [8].

For sellers, having clean financial records and transparent operating data is crucial to attracting institutional buyers, as the market now prioritizes accuracy over optimistic projections [10]. Buyers, on the other hand, should stress test their underwriting by accounting for flat rent growth and rising insurance and tax costs. This ensures that deals remain viable even if rates stay elevated.

"In 2026, the focus will be on recalibration. Self-storage investors are stepping into a phase in which capital is accessible, debt is more affordable and the fundamentals of strong markets carry greater weight." – Ryan Gibson, Chief Investment Officer, Spartan Investment Group [8]

2. Supply Decline Strengthening Market Conditions

The pace of self-storage construction has slowed significantly. By 2026, new supply is projected to account for just 2.4% of total stock, down from 3.0% in 2025 and well below the long-term average of 4.2% [3]. This slowdown is especially beneficial for overbuilt markets, particularly in Sunbelt cities like Atlanta, Phoenix, and Orlando [12]. Combined with improved financing conditions, this reduction in new developments is bolstering demand for existing facilities.

Impact on Market Fundamentals

With fewer new projects in the pipeline, existing facilities are in a stronger position to meet demand. Occupancy rates across the industry are stabilizing as self-storage construction inventory declined to 2.5% in early 2026, reflecting a 0.1% monthly drop [12]. This trend gives operators breathing room to manage occupancy levels more effectively. That said, self-storage remains a highly localized business. While national trends are encouraging, individual submarkets may still face challenges if local supply exceeds demand within a three-mile radius [4].

"The slowdown in construction will give existing properties a chance to stabilize and regain pricing power in stronger markets." – Ryan Gibson, Chief Investment Officer, Spartan Investment Group [8]

Occupancy stabilization also highlights how reduced supply strengthens the competitive position of operators equipped with modern systems and strategies.

Opportunities for Revenue Growth

As occupancy rates level out, the focus is shifting toward revenue growth. The easing of supply pressures is creating room for recovery. By early 2026, national advertised street rates reached $16.27 per square foot [12]. Meanwhile, same-store revenue growth for major REITs like Extra Space and SmartStop showed signs of stabilization, with both reporting 0.4% growth in Q4 2025 [12].

One of the factors driving this recovery is the increase in tenant retention. Average tenant stays have extended to 18–19 months, compared to just 9–14 months in 2017 [3]. Longer stays reduce turnover costs and provide opportunities for gradual rent increases, further supporting revenue growth.

On the development side, rising costs for materials and labor are adding to the constraints on new supply. Since 2020, the cost of steel has increased by 30%, concrete by 20%, and labor by 25% [1]. Additionally, stricter zoning regulations in more than 50 cities, including Atlanta, Chicago, and New York, are making it harder to launch new projects [1].

Relevance to Self-Storage Owners and Investors

The decline in new supply presents a strategic edge for operators who can adapt to these market shifts. Remaining vigilant about local market conditions – especially within a three-mile radius – is critical for understanding competitive dynamics [3].

For operators, focusing on tenant retention and implementing data-driven pricing strategies can help maximize the value of existing customers. With fewer new facilities available, tenants are more likely to stay when offered quality service and reasonable rate adjustments. For investors, targeting properties in supply-constrained areas with zoning and land scarcity barriers can provide a natural buffer against future competition [4] [8]. By prioritizing these strategies, both operators and investors can position themselves to thrive in the evolving self-storage market.

3. Technology Becoming Standard Operating Requirement

Technology has become a non-negotiable in the self-storage industry. By 2026, the divide between operators using advanced systems and those stuck with outdated processes has grown significantly. Over 90% of institutional facilities now rely on dynamic pricing, compared to just 15%–20% of independent operators [1]. Facilities that fail to adopt modern technology are missing out on an additional 5%–10% in income [1].

Adoption of New Practices

The shift toward remote and hybrid management models is changing how facilities operate. For example, 10 Federal Storage reported running 120 properties entirely through automation by February 2026. Their AI call resolution rates jumped from 10% to nearly 80% over the same period [6]. Meanwhile, Copper Storage Management oversees 150 active locations using a hybrid model that combines remote management with scheduled maintenance visits. Their approach treats the customer’s smartphone as the main tool for tasks like rentals and payments [6].

"Your phone is a better, faster kiosk than anything on the market." – Brett Copper, President, Copper Storage Management [6]

AI is also revolutionizing revenue management. OnTrac Storage, for instance, onboarded seven third-party management facilities in just two weeks in early 2026, thanks to AI-driven pricing and call automation. This process, which used to take months, now happens in minutes. These advancements are driving market efficiency and consolidation [6].

Impact on Market Fundamentals

The benefits of technology go far beyond saving labor costs. Smart lock and access systems can cut onsite labor expenses by 30%–50% [1]. AI digital assistants now handle over 50% of inbound calls for many operators, with some reaching 80% [6]. This efficiency allows mid-sized operators to manage portfolios that once required the resources of large REITs, further accelerating consolidation in the industry [6][1].

Customer expectations have also shifted. Around 40% of customers now prefer a fully touchless, self-service experience [6]. Features like 24/7 online rentals, digital leases, and mobile account management are no longer perks – they’re baseline requirements. Operators that don’t offer these conveniences risk losing serious customers to competitors who do [7].

Relevance to Self-Storage Owners and Investors

Just like financing and supply trends, technology is reshaping the self-storage landscape. For operators, the takeaway is clear: adopt dynamic pricing and automate repetitive tasks to stay competitive. Start small by testing new tools at a few facilities before rolling them out portfolio-wide. Any new technology should prove its ROI within six months [6]. For investors, properties with outdated systems present immediate opportunities to boost NOI by implementing modern technology [1].

"AI is only valuable if it amplifies the parts of the job that humans are best at. We’re not interested in replacing people. We’re trying to eliminate the noise around them." – Brian Oakley, Vice President of Technology, 10 Federal Storage [6]

In today’s increasingly consolidated market, technology is the key to competitive pricing, operational efficiency, and delivering the seamless experiences customers now expect.

4. Growth in Specialty Storage Options

The self-storage industry is expanding to meet specialized needs, with climate-controlled units now making up 50%–60% of new constructions, compared to just 30% previously [1]. This shift reflects a growing demand for storing high-value items like electronics, wine, and business inventory, moving beyond traditional overflow storage. These changes align with broader trends in financing, supply, and technology within the market.

Opportunities for Revenue Growth

Climate-controlled units offer a significant financial advantage, commanding a 25%–40% higher price than standard drive-up units. On average, these units generate $18–$28 per square foot, compared to $10–$16 for traditional options [1]. Small businesses, in particular, are driving demand for larger, more flexible storage solutions. With industrial building vacancies under 10,000 square feet at a mere 2.8% as of mid-2025, many contractors, online sellers, and caterers are turning to self-storage as micro-industrial spaces [15].

"As consumers store higher-value items – such as electronics, wine, and collectibles – rather than just ‘garage overflow,’ they have proven willing to pay a higher premium for strict humidity and temperature regulation." – R.J. Hottovy, Head of Analytical Research, Placer.ai [14]

A new category of storage has also emerged: storage-industrial-flex condos. These units, ranging from 1,000 to 2,000 square feet, are sold to private owners and come equipped with electrical and water hookups for customization [15]. Though this segment accounts for less than 5% of the market, it appeals to affluent collectors and small businesses priced out of traditional industrial real estate [15].

Relevance to Self-Storage Owners and Investors

For self-storage operators, adapting to these trends offers a pathway to increased revenue. Retrofitting existing units to include climate-controlled options can help capture higher earnings per square foot. As demand evolves and profit margins tighten, diversifying unit offerings becomes essential. Targeting commercial tenants – like online entrepreneurs and contractors – through tailored marketing strategies can open up new revenue streams. For new developments, prioritizing fully climate-controlled facilities aligns with current market demand and attracts institutional buyers seeking premium properties [1][14].

Additionally, focusing on tenants who view storage as a long-term lifestyle solution – those who treat it as an extension of their homes – can lead to longer stays and reduced sensitivity to rent increases. These "sticky" tenants represent a valuable demographic for operators looking to ensure steady, reliable income [14].

5. Longer Tenant Stays and Controlled Pricing

Impact on Market Fundamentals

Tenant stays have stretched from 9–14 months to 18–19 months, thanks to persistently high mortgage rates and a sluggish housing market [3]. With only 11% of Americans changing addresses – down from 14.3% in 2015 – there are fewer life transitions, which means fewer move-outs from storage facilities [8].

This shift has kept national occupancy rates steady between 89% and 92% since early 2024. Storage units have effectively become a semi-permanent extension of the home, especially in pricey metropolitan areas [16][8]. While street rates for new customers have flattened, showing just +0.3% year-over-year growth in early 2026 [1], the stability in occupancy provides a foundation for fresh revenue strategies.

Opportunities for Revenue Growth

Although new move-in rates dropped to $79.44 in 2025 [7], operators have compensated by implementing annual price increases of 8%–12% for long-term tenants [1]. These "sticky" customers, often tied to their housing situations, are more likely to accept gradual price hikes than deal with the hassle of relocating their belongings [14].

"Because these tenants were also locked into their housing situations, they proved incredibly ‘sticky’ – accepting the price hikes rather than going through the hassle of moving their goods." – R.J. Hottovy, Placer.ai [14]

The challenge lies in balancing street rates with achieved rates to safeguard net operating income, even as new customer acquisition slows. Building on these gradual increases, operators are now rethinking their post-move-in pricing strategies.

Adoption of New Practices

Operators are shifting from aggressive post-move-in price hikes to retention-focused pricing [9]. This approach helps mitigate tenant churn in a low-demand environment and reduces regulatory risks, as several states have begun scrutinizing extreme pricing practices [2].

To support these extended tenant relationships, 78% of operators plan to stand out by offering superior customer service in 2026 [17]. Investments in automation, like smart-lock systems and AI-assisted support, are becoming common. At the same time, operators are maintaining a personal touch for more complex issues [9]. The goal is to elevate storage from a "grudge purchase" to an essential service, justifying premium pricing through a better overall experience.

Relevance to Self-Storage Owners and Investors

Longer tenant stays are transforming how operators and investors approach revenue management. Lifetime customer value is increasing, making retention strategies far more valuable than aggressive efforts to acquire new customers [5]. Business intelligence tools are becoming essential for identifying specific opportunities to adjust rates within the current tenant base, rather than relying on broad national averages [9].

"Tenants are staying longer than ever, most likely due to housing affordability issues and changing demographics… Retaining existing customers is crucial, as the lifetime value of each customer goes up and up!" – Tyler McDowell, StoragePug [5]

Operators should keep a close eye on local migration patterns and mortgage trends to adjust pricing strategies proactively [8]. In oversupplied markets, particularly in the Sunbelt, the focus should be on maintaining occupancy and improving operational efficiency rather than pushing for aggressive rent increases until the excess capacity is absorbed [13][14]. Success in 2026 will hinge on recognizing that pricing discipline and customer experience are now the main drivers of profitability, underscoring how industry consolidation and technological advancements are shaping competitive advantages.

Conclusion

The trends we’ve discussed offer a clear guide for navigating the evolving self-storage industry in 2026. With better financing terms now available, operators can refinance older high-rate loans, using debt as a tool to boost returns rather than hinder them.

A tighter supply outlook also strengthens the competitive advantages we explored earlier. While new construction will slow down, creating opportunities for existing operators, it’s still essential to keep a close eye on local market conditions.

When it comes to technology, there’s no room for hesitation. Independent operators relying on static pricing models could be missing out on 5%–10% of potential revenue compared to those using AI-driven systems [1]. Start by adopting dynamic pricing, automating collections, and ensuring your website supports mobile move-ins. These upgrades don’t require huge capital investments but do demand a commitment to modernization.

Shifting tenant behavior and premium storage options are opening up new revenue streams. For example, climate-controlled units can charge 25%–40% higher rents [1], and longer tenant stays allow for gradual rate increases without risking move-outs. Prioritize tenant retention, enhance customer service to justify premium rates, and explore high-demand niches like RV or boat storage.

The key to success in 2026 lies in combining a disciplined strategy with sharp local market insights. Stay informed about your market, embrace modern technology, and focus on retaining your current tenants – they’re your most valuable resource. The opportunity is here now, but it won’t last forever.

FAQs

How do I tell if my local market is still oversupplied?

Wondering if your local self-storage market has too many units? Keep an eye on these key indicators:

- Local supply and demand: Look at new construction activity. Nationally, new builds accounted for 2.4% of total inventory recently.

- Rent trends: Street rates dropped 0.2% year-over-year as of January 2026. Falling rents can be a warning sign.

- Occupancy rates: The average occupancy was 77% in late 2025. If occupancy in your area is declining, it could point to oversupply.

When you notice falling occupancy or rent growth turning negative, it’s often a sign that your local market might have more storage units than it needs.

Which tech upgrades deliver the fastest ROI for a small facility?

If you’re looking to boost efficiency and see quick returns, consider investing in AI-powered tools, centralized management software, and streamlined operational systems. These technologies are designed to simplify daily operations, enhance customer experiences, and reduce unnecessary friction in your workflows.

When choosing upgrades, prioritize tools that make your operations smoother and more intuitive. The right solutions can not only save time but also help you deliver better service – leading to happier customers and stronger returns.

Should I add climate-controlled units or other specialty storage?

Modernizing your storage facilities with climate-controlled units or specialty storage options could be a smart move for 2026. Trends indicate that features like these attract buyers and make your property stand out in a competitive market. Plus, investing in these upgrades can boost your property’s value while catering to the increasing demand for more advanced and specialized storage solutions.