If you’re a self-storage owner considering selling, preparation is key to maximizing your facility’s value. Here’s what you need to know:

- Start Early: Begin planning 12–24 months before listing your property. This gives you time to clean up financial records, address maintenance, and optimize operations.

- Know Your Goals: Define your "walk-away number" (the minimum net amount you need after taxes and fees) and choose the right exit strategy based on your objectives – whether it’s immediate cash, ongoing income, or tax deferral.

- Exit Strategies: Options include outright sales, 1031 exchanges, installment sales, or partial equity sales. Each has unique benefits and trade-offs.

- Valuation Factors: Buyers focus on net operating income (NOI), cap rates, occupancy trends, and operational efficiency. Even a small error in financial records can significantly lower your sale price.

- Tax and Legal Considerations: Work with a tax advisor to minimize capital gains taxes and ensure your legal structure supports a smooth transfer.

- Build a Team: Engage experts like brokers, CPAs, attorneys, and advisors to guide you through valuation, marketing, and negotiations.

Planning ahead ensures you’re ready for buyer scrutiny, maximizes your sale price, and reduces stress during the process. Whether you’re selling to a REIT, private equity, or a local buyer, preparation is the foundation of a successful exit.

Clarifying Personal and Financial Goals

Knowing your exit goals from the start is critical – skipping this step can lead to rushed, poorly thought-out decisions.

Defining Your Owner Objectives

Self-storage owners often fall into distinct categories: retirees seeking steady cash flow, investors planning a 1031 exchange, estate planners, or operators ready to move on. Each of these profiles points toward a different exit strategy.

One of the first steps is to determine your walk-away number – the minimum net amount you’re willing to accept after factoring in taxes, broker fees, and transaction costs. Establishing this figure early on can help you avoid making hasty decisions when offers start rolling in.

"Let your target outcome guide your operational decisions." – RK Kliebenstein, Founder, Self Storage LLC

Your choice of buyer also plays a significant role in shaping your objectives. For instance, selling to a REIT means meeting strict institutional requirements, such as clean financial records, stabilized occupancy rates, and a polished, Class-A property presentation. On the other hand, selling to a local aggregator may only require demonstrating strong dominance in your submarket.

Once your objectives are clear, you can evaluate the trade-offs each exit option presents in terms of liquidity, risk, and control.

Balancing Liquidity, Risk, and Control

Exiting your business involves a simple but crucial trade-off: the more liquidity you want, the less control you’ll retain. For example, an outright sale provides immediate cash but ends your involvement entirely. A partial equity sale allows you to keep some ownership, partner with an investor, and potentially benefit from a larger future exit. However, it also introduces risks, such as shared decision-making and partner disagreements.

This balance affects not only your cash flow but also how buyers perceive your business and its eventual sale price.

| Exit Strategy | Liquidity | Risk Level | Level of Control |

|---|---|---|---|

| Outright Sale | High | Moderate | None |

| Partial Equity Sale | Moderate | High | Partial |

| Installment Sale | Low to Moderate | Moderate | None to Low |

| 1031 Exchange | Low | Moderate | High (new asset) |

Additionally, if your loan is assumable, verify that the buyer’s terms include releasing your personal guarantee at closing.

Setting Your Exit Timeline

With your objectives and risk preferences in mind, it’s time to set a realistic timeline for your exit. Most sales take 12–24 months from preparation to closing. Buyers and lenders will expect at least three years of clean financial statements. They’ll also review occupancy trends over a 24-month period rather than relying on a single snapshot.

Your loan terms can also influence your timeline. Prepayment penalties like yield maintenance or defeasance clauses can make an early exit costly, so reviewing your loan documents should be one of your first steps. A phased approach is often the most effective way to prepare:

| Phase | Timeline | Key Activities |

|---|---|---|

| Foundation | Months 1–3 | Gather financials for the past three years, document 24-month occupancy trends, and consult a tax advisor |

| Cleanup | Months 3–7 | Address deferred maintenance and update security or management software |

| Compliance | Months 5–9 | Complete a Phase I Environmental Assessment and confirm zoning/ADA compliance |

| Marketing | Months 9–14 | Hire a broker and prepare a Confidential Information Memorandum (CIM) |

| Execution | Months 12–24 | Open a data room, negotiate LOIs, and manage due diligence and transition |

"Most self-storage owners spend decades building a cash-flowing asset, then rush the sale process and leave money on the table." – DealFlow OS

The size of your facility also impacts how you approach the sale. If your annual earnings exceed $2 million, the complexity of dealing with institutional buyers often makes hiring a full-service M&A advisor worthwhile. For facilities generating less than $500,000 annually, a curated marketplace might be a better fit, offering a faster and more straightforward process. Knowing where you stand helps you focus your time and resources effectively.

How Self-Storage Facilities Are Valued

Once you’ve established clear exit goals and aligned your objectives, the next step is understanding how your facility is valued in the current market. This knowledge is essential for setting realistic expectations and defining financial benchmarks that support your exit strategy.

Key Valuation Metrics

The cornerstone of any self-storage facility valuation is Net Operating Income (NOI) – essentially, your gross rental income minus operating expenses (excluding debt payments). From there, buyers use a capitalization (cap) rate to calculate the facility’s value. The formula is simple: Value = NOI ÷ Cap Rate. For example, if your facility generates $300,000 in NOI and the local cap rate is 7%, the estimated value would be approximately $4.28 million.

"The value of a self-storage facility is rooted in net operating income (NOI), not market conditions, and both have changed." – Jane H. Sauls, Co-Owner, Sauls Storage Group LLC

Cap rates vary widely depending on the facility’s class and location. A Class A, climate-controlled facility in a major metropolitan area might trade at cap rates between 5.5% and 6.5%, whereas older, drive-up properties in rural markets could see cap rates in the 8.0%–10.0% range.

In addition to cap rates, lenders place significant emphasis on the Debt-Service Coverage Ratio (DSCR). A DSCR of at least 1.3x is typically required to secure financing. Another common valuation tool is Discounted Cash Flow (DCF) analysis, which projects performance over 5–10 years to test assumptions about occupancy rates and rent growth.

One often-overlooked metric is the gap between physical and economic occupancy. A facility might appear strong at 95% physical occupancy, but if tenants are delinquent or rents are heavily discounted, the economic occupancy – and actual revenue – could be much lower. Buyers will scrutinize these details during due diligence, so auditing your rent roll against actual deposits is essential before listing.

Operational and Market Factors

While NOI and cap rates are critical, operational efficiency and market conditions also play a big role in determining a facility’s value. Operating expenses, for instance, significantly impact profitability. Most self-storage facilities operate with expenses ranging from 30% to 45% of gross revenue. Facilities on the lower end of this range – often those that use automation, kiosks, or smart locks – tend to command higher valuations because their NOI is stronger relative to revenue. Automation alone can reduce on-site labor costs by 30%–50%.

Market supply is another key factor. The national average for self-storage supply is about 7 to 8 square feet per capita. Markets with more than 10 square feet per capita may face oversaturation, leading to downward pressure on rents and valuations. On the flip side, rising construction costs – steel up 30%, concrete up 20%, and labor up 25% since 2020 – are creating barriers to new competition, which can help support the value of existing facilities. Buyers generally prefer facilities with occupancy rates in the 85%–92% range; anything outside this range may raise concerns.

"Buyers are no longer pricing assets solely on trailing performance. They are pricing execution risk, operational clarity, and certainty of close." – Matthew Horne, Storage Point Advisors

Getting a Professional Valuation

A strong valuation typically blends multiple methods. Professionals often combine the income capitalization approach (NOI ÷ cap rate) with a sales comparison of recent local transactions and a replacement cost analysis to set a value ceiling. For instance, if the market value of your facility approaches or exceeds the cost to build a comparable one – roughly $50–$65 per square foot for single-story construction or $90–$130 per square foot for multi-story – buyers might hesitate, as developers could choose to build new instead.

Engaging an experienced advisor can make a significant difference. A well-managed sale process can create competitive bidding, potentially leading to price differences of 25% or more between similar facilities. Firms like Oakside Co specialize in presenting clean, market-ready financials that withstand institutional scrutiny. Starting the valuation process at least one to two years ahead of your planned sale allows time to address weaknesses and avoid giving buyers leverage during negotiations.

Preparing Your Facility for Sale

Once you’ve assessed your facility’s valuation, the next step is ensuring its value is preserved and positioned for a top-dollar sale.

Financial and Operational Review

Potential buyers and their lenders will scrutinize at least three years of profit and loss statements, tax returns, and balance sheets. Before sharing these documents, take the time to clean them up. Eliminate personal expenses – like vehicle payments or travel – that don’t pertain to the business. This ensures your operating costs accurately reflect a stabilized net operating income (NOI). Additionally, review your loan agreements for any prepayment penalties, such as yield maintenance or defeasance, which could impact the financial feasibility of a sale.

"Your profit-and-loss statement must be pristine. This means removing personal or partnership expenses that aren’t related to the self-storage business, like a vehicle payment." – RK Kliebenstein, Founder, Self Storage LLC

The stakes are high when it comes to accurate financial documentation. For instance, a $20,000 discrepancy in income could result in $120,000 in lost value at a 6x multiple. Beyond financial statements, export your current rent roll from your property management software. Double-check that unit statuses, rates, and tenant records are accurate. Also, provide 24 months of monthly occupancy history categorized by unit type.

After tidying up your financials, make sure the physical condition of your property matches that same level of precision.

Property Improvements That Add Value

Neglecting maintenance on critical areas like roofing, drainage, or pavement can lead to deal-breaking issues or significant price reductions. Addressing these problems – typically costing between $30,000 and $80,000 – before listing could prevent buyers from slashing offers by as much as $300,000.

"A facility needing $150,000 in actual work might see buyer offers reduced by $300,000 or more because of these concerns." – Matt Wess, Senior Vice President of Real Estate, MyPlace Self Storage

In addition to essential repairs, targeted upgrades can enhance your facility’s valuation. Features like keypad access systems, cloud-based video surveillance, and individual unit alarms appeal to institutional buyers and can increase your valuation multiple by 0.25x to 0.5x NOI. Similarly, LED lighting with motion sensors and energy-efficient HVAC systems for climate-controlled units lower operating costs, boosting NOI. Simple touches like fresh paint, cohesive signage, and well-maintained landscaping also create a strong first impression for appraisers and potential buyers.

If your property includes unused land or units that could be converted into climate-controlled spaces, document this potential with a feasibility analysis. Buyers who see a clear value-add opportunity may be willing to pay a higher multiple compared to a fully stabilized asset.

Once you’ve addressed operational and physical aspects, it’s time to organize your data for buyer review.

Data-Driven Pre-Sale Optimization

Prepare a virtual data room containing all essential documents, such as financials, rent rolls, occupancy history, vendor contracts, compliance records, and property condition reports. A well-organized data room can shorten the due diligence process by 30 to 60 days.

Partnering with an experienced advisory firm can make this process smoother. For example, Oakside Co offers investment-banking-level analysis to identify gaps in your facility’s financial and operational profiles. Addressing these gaps proactively ensures you’re ready to meet institutional standards during negotiations.

One critical mistake to avoid: don’t artificially boost occupancy by offering steep rent discounts right before listing. Sophisticated buyers will adjust the rent roll to reflect sustainable market rates, and undisclosed concessions can damage trust during due diligence. Ideally, plan for 12 to 24 months of preparation before listing. This timeline allows you to implement meaningful improvements without rushing decisions that could hurt your bottom line.

Choosing the Right Exit Strategy

Once your facility is ready and your financials are in order, the next big decision is how to exit. The best approach depends on factors like your financial goals, loan terms, property performance, and the current pool of buyers in the market.

Outright Sale

An outright sale involves transferring full ownership, giving you immediate proceeds. However, the type of buyer you target will influence everything – from pricing to how you present your financials. Right now, buyers generally fall into four main categories, each with distinct priorities:

| Buyer Category | Primary Motivation | Target Asset Type |

|---|---|---|

| REITs | Scale and shareholder dividends | Class-A, stabilized assets in primary/secondary markets |

| Private Equity | Specific internal rate of return | Value-add, Certificate of Occupancy (C of O) deals |

| Family Offices | Long-term cash flow and preservation | High-quality, durable assets |

| Local Aggregators | Regional concentration | Smaller, non-institutional properties in rural/secondary markets |

For example, institutional buyers like Public Storage spent around $946 million on acquisitions in 2025, while private equity groups reportedly hold $5–$8 billion in funds reserved for self-storage investments. REITs often stick to strict criteria, focusing on stabilized, Class-A properties in markets with high barriers to entry. If your facility doesn’t meet these benchmarks, you might find better success targeting regional aggregators or family offices for a quicker, smoother transaction.

Keep in mind that your existing loan terms could impact the feasibility of a sale. On the other hand, if your loan is assumable, it could make your property more appealing by helping buyers sidestep higher financing costs.

If selling outright doesn’t fit your goals, there are other options to explore.

Partial Exit Options

A full sale isn’t always the best fit, especially if timing or other goals are a concern. Partial exits allow you to sell a portion of equity, bringing in capital while still retaining operational control. This strategy is often paired with refinancing, giving you liquidity and resources to expand while keeping a hand in the business.

Another option is third-party management (3PM). Companies like CubeSmart and Extra Space typically charge management fees of 6% to 8% of gross revenue, and facilities under professional management often experience a 10% to 25% boost in NOI within 12 to 24 months. While an outright sale provides immediate liquidity, 3PM lets you hold onto the asset, improve its performance, and potentially secure a better deal down the road.

If your facility has growth potential, scaling your portfolio could lead to even greater returns.

Portfolio and Scaling Strategies

Growing your portfolio before exiting can significantly increase your property’s valuation. Small, single-facility operators usually sell at 5× to 8× NOI, whereas institutional-grade portfolios can command multiples of 10× to 15× NOI. A 1031 exchange is a useful tool for reinvesting proceeds into larger assets while deferring capital gains taxes. Additionally, buying underperforming facilities and boosting their performance through better management and marketing can add real value when it’s time to sell.

As RK Kliebenstein, Founder of Self Storage LLC, advises:

"Your desired outcome should dictate every decision you make while holding the asset. Thinking about this financial goal forces you to reverse-engineer your entire operation."

Whether you decide on an outright sale, bring in a partner, or scale for a bigger exit, the key is to align your strategy with your long-term financial goals.

Tax, Legal, and Estate Considerations

After tackling operational and financial preparation, it’s equally important to address tax, legal, and estate matters. These factors can significantly impact the value you retain from a sale if not handled early in the process.

Tax Implications and Planning Strategies

Selling commercial property comes with a variety of tax obligations. For starters, federal long-term capital gains tax applies to the appreciation above your adjusted cost basis, with rates reaching up to 20%. Then there’s depreciation recapture, which is often overlooked but typically taxed at 25% on prior deductions. High-income earners may also face an additional 3.8% Net Investment Income Tax. State taxes add another layer of complexity, with wide variations depending on location. For instance, in California, gains exceeding $1 million can be taxed at a combined state rate of 14.3%. To put this into perspective, a $5 million sale with a $3 million gain could see nearly 25% of the gross sale price consumed by federal and state taxes.

As Paulo Aguilar, CFA, CAIA, from Wealthstone Group, points out:

"Tax outcomes are determined well before the sale."

One of the most effective tools for managing these taxes is a 1031 exchange, which allows you to defer capital gains, depreciation recapture, and state taxes by reinvesting the proceeds into a qualifying replacement property. Aguilar emphasizes:

"Tax deferral works best when it supports a broader investment strategy, not when it is used as a last-minute fix."

Additionally, it’s wise to review loan documents for potential prepayment penalties, as these can reduce your net proceeds if overlooked.

Legal Structure and Succession Planning

The legal structure of your business plays a crucial role in both taxation and the ease of ownership transfer. For example, whether your sale is structured as an asset sale or a stock sale can have major tax implications, depending on whether your business operates as an LLC, S-corp, or C-corp. Disorganized corporate records – like missing operating agreements or unsigned meeting minutes – can delay or even derail a deal.

Succession planning is especially vital for family-owned businesses. Statistics show that fewer than 30% of family businesses make it to the second generation, and a staggering 83% of business owners lack a written exit plan. Establishing formal governance, clear decision-making authority, and a buy-sell agreement can prevent disputes and keep the sale process on track.

From an estate planning perspective, the stepped-up basis under IRC 1014 is a powerful strategy. If the property is held until death, heirs receive a basis reset to the fair market value, effectively eliminating capital gains taxes and depreciation recapture. Another smart move is pre-sale gifting of ownership interests before signing a Letter of Intent. This allows assets to be valued at current earnings rather than the higher sale price, potentially lowering gift tax exposure.

By addressing these tax and legal considerations now, you’ll lay the groundwork for assembling a dedicated advisory team to guide the process.

How Advisory Teams Support the Process

Navigating the tax and legal complexities of a self-storage exit requires a well-coordinated team. This typically includes a transaction CPA, an M&A attorney, and a wealth advisor, all working together to align the deal structure and timeline. Firms like Oakside Co, a national commercial real estate advisory group, specialize in ensuring every phase of the sale – from structure to timing – is optimized to minimize costs and avoid surprises, helping owners achieve a smooth and efficient close.

sbb-itb-09b4138

Building Your Exit Planning Team

A successful exit hinges on assembling the right advisory team. While financial, operational, and compliance prep lays the groundwork, your team will be the driving force behind executing the sale effectively.

Key Roles on Your Advisory Team

Your exit planning team should include specialists who cover valuation, legal, operational, and financial aspects. Here’s a breakdown of the key players:

- Self-storage broker or M&A advisor: This expert handles the initial valuation, creates the Confidential Information Memorandum (CIM), identifies and qualifies buyers, and oversees a controlled auction process to encourage competitive bidding. A skilled broker can boost your final sale price by 10–20% through proper deal structuring and buyer selection.

- CPA (Certified Public Accountant): Goes beyond standard bookkeeping to uncover owner add-backs that normalize your NOI and structures the deal to reduce tax exposure. This role is critical for strategies like 1031 exchanges and installment sales.

- Commercial real estate attorney: Ensures the legal framework of the deal is solid, whether it’s a real estate or business sale. They also handle title issues, confirm zoning compliance, and negotiate the purchase agreement.

- Third-party consultants: These professionals – such as engineers, environmental experts, and ADA auditors – identify compliance risks early, preventing potential deal-breaking issues during due diligence. They also manage necessary assessments and reviews.

- Financial planner: Focuses on post-sale wealth management and reinvestment strategies, including estate planning for highly appreciated assets.

If your facility generates annual earnings above $2 million or involves multiple sites, a full-service M&A advisor is often a better choice than a listing platform. These advisors provide tighter confidentiality, phased buyer disclosure, and hands-on management for complex transactions.

For example, firms like Oakside Co combine investment-banking-level analysis with a national network of investors. This approach ensures precise pricing and access to a pool of qualified buyers, which can be a game changer for sellers.

Exit Planning Timeline

Once your advisory team is in place, coordinating their efforts within a structured timeline is essential. A typical self-storage exit takes 12 to 24 months from initial planning to closing. Rushing any step often leads to price reductions during due diligence.

Matthew Horne of Storage Point Advisors emphasizes the importance of preparation, stating:

"The difference between activity and execution is preparation."

The table below outlines the five phases of a typical exit process, along with the contributions of each team member at every stage:

| Phase | Timeline | Team Activities |

|---|---|---|

| Phase 1: Financials | Months 1–3 | CPA finalizes valuation and reviews 1031 options; tax advisor aligns deal structure with owner goals. |

| Phase 2: Operations | Months 3–7 | Third-party consultants conduct property condition assessments; broker documents operational improvements for the CIM. |

| Phase 3: Compliance | Months 5–9 | Environmental experts and ADA auditors handle assessments; attorney clears title issues and confirms zoning. |

| Phase 4: Marketing | Months 9–14 | Broker prepares CIM and targets qualified buyers; advisor identifies expansion opportunities to enhance pricing. |

| Phase 5: Execution | Months 12–24 | Full team manages the data room, LOI negotiations, due diligence, and transition planning. |

To speed up due diligence by 30–60 days, pre-load a virtual data room with three years of audited financials, rent rolls, and vendor contracts. This can be a huge advantage when buyers are comparing multiple opportunities simultaneously.

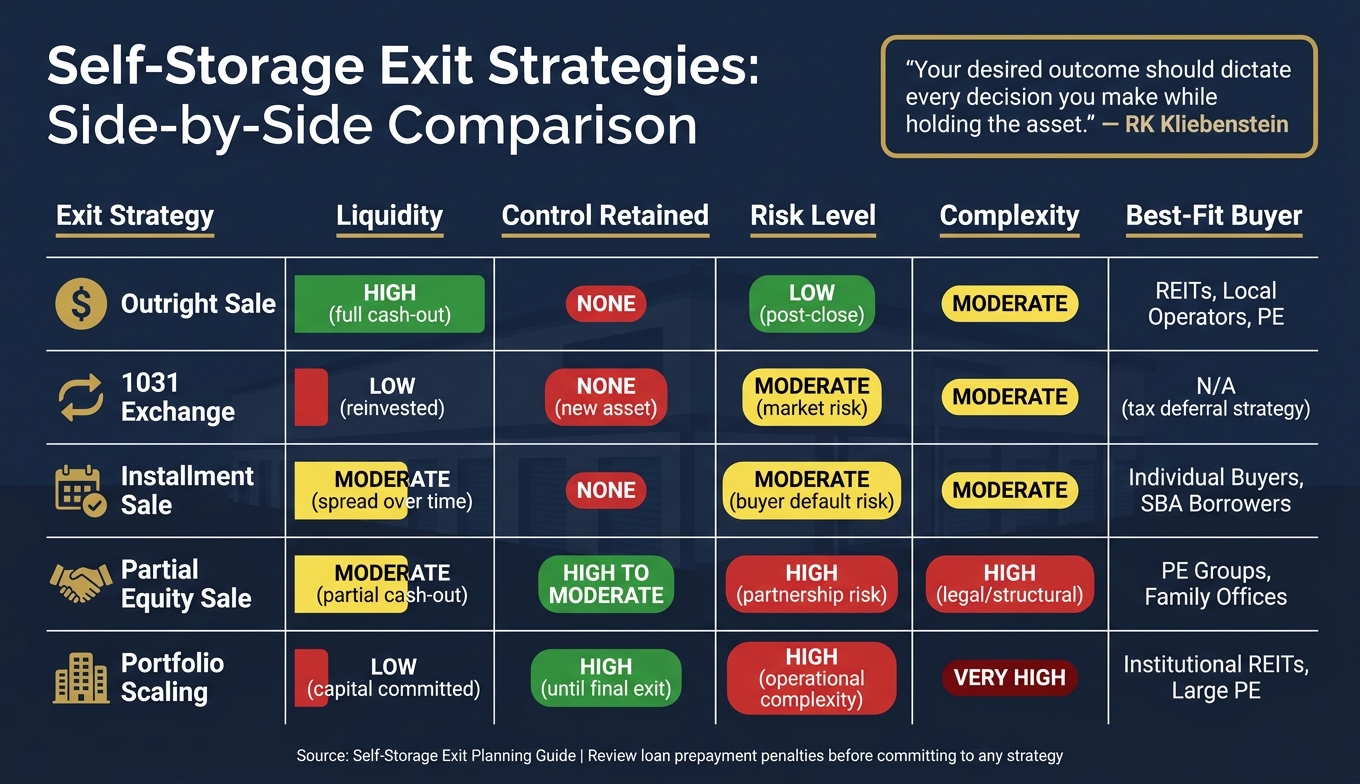

Comparing Exit Options Side by Side

Self-Storage Exit Strategies Compared: Liquidity, Risk & Control

This section lays out the most common exit strategies, helping you align your personal objectives with the best-fit approach. Each option comes with its own set of trade-offs, impacting factors like taxes, control, and future income.

As RK Kliebenstein wisely puts it:

"Your desired outcome should dictate every decision you make while holding the asset."

The five primary exit strategies offer varying levels of liquidity, control, risk, and complexity. For example, an outright sale provides maximum liquidity but eliminates future income streams. A 1031 exchange allows you to defer capital gains taxes, but it requires reinvestment within a strict 180-day window. Opting for an installment sale spreads tax liability over time and may attract more buyers, though it exposes you to the risk of buyer default. A partial equity sale lets you retain some control by partnering with private equity groups or family offices; however, shared decision-making is required. Finally, portfolio scaling, which involves aggregating multiple facilities into a platform, can lead to higher institutional valuations but requires significant operational effort and ties up capital for longer periods.

Exit Strategy Comparison Table

| Strategy | Liquidity | Control Retained | Risk Level | Complexity | Best-Fit Buyer |

|---|---|---|---|---|---|

| Outright Sale | High (full cash-out) | None | Low (post-close) | Moderate | REITs, local operators, PE |

| 1031 Exchange | Low (reinvested) | None (new asset) | Moderate (market risk) | Moderate | N/A (tax strategy) |

| Installment Sale | Moderate (spread over time) | None | Moderate (buyer default) | Moderate | Individual buyers, SBA borrowers |

| Partial Equity Sale | Moderate (partial cash-out) | High to Moderate | High (partnership risk) | High (legal/structural) | PE groups, family offices |

| Portfolio Scaling | Low (capital remains committed) | High (until final exit) | High (operational complexity) | Very High | Institutional REITs, large PE |

This side-by-side comparison highlights the critical trade-offs involved in each strategy. For instance, tax structuring plays a key role in maximizing net proceeds. Before committing, review your loan terms to check for prepayment penalties like yield maintenance or defeasance, as these costs can significantly impact the profitability of a sale.

Ultimately, choosing the right exit strategy requires careful alignment with both your financial and operational goals. Collaborating with a seasoned advisory team is essential to navigating these complexities. Firms like Oakside Co can provide the data-driven insights and personalized guidance needed to ensure your exit strategy aligns with your long-term objectives.

Closing the Deal and Moving Forward

With your exit strategy in place, it’s time to focus on finalizing the deal and preparing for a smooth transition.

Final Due Diligence and Negotiation

Once you’ve accepted a Letter of Intent (LOI), the due diligence process ramps up significantly. Buyers will scrutinize details like 24-month occupancy trends, effective rent per square foot compared to market benchmarks, lien sale compliance records, and your technology infrastructure. Additionally, a clean Phase I Environmental Site Assessment (ESA) is a must for lenders – any unresolved environmental issues could derail the deal during escrow.

Before due diligence begins, ensure your Virtual Data Room (VDR) is fully stocked with all necessary documents, including financial statements, rent rolls, legal agreements, and operational records. A well-organized VDR can cut the due diligence timeline by 30–60 days. Pay particular attention to the accuracy of the current rent roll, as this directly impacts valuation.

Negotiations at this stage often center on deal structure rather than the headline price.

"A slightly lower price with stronger certainty often produces a better outcome than a headline number that collapses later." – Matthew Horne, Storage Point Advisors

Key points to negotiate include earnest money terms, diligence timelines, extension clauses, and how risks are allocated between buyer and seller. Buyers may use undisclosed issues uncovered during due diligence as leverage, often seeking discounts that are two to three times the actual cost of repairs.

Once these steps are complete, the focus shifts to ensuring a smooth operational transition.

Managing the Operational Transition

A seamless transition is critical to maintaining stability and avoiding last-minute deal complications. Develop a 30–60 day transition plan that covers tenant communications, vendor relationships, system access, and operational procedures.

If you have key staff, consider offering stay bonuses tied to their employment for a defined post-closing period, typically 90–180 days. This reassures buyers that the business will remain stable and operational. For deals involving SBA 7(a) loans, lenders often require a seller training or transition period of 30–90 days, so planning ahead can help avoid unexpected delays.

Make sure to review all vendor and customer contracts for change-of-control clauses. Contracts that automatically terminate upon a sale can create significant liabilities if not addressed before closing.

Post-Exit Financial Planning

Closing the sale is just the beginning of a new chapter in financial planning. Address tax considerations immediately, using tools like 1031 exchanges into Delaware Statutory Trusts (DSTs) or installment sales. These strategies can help you retain 15–30% more of your net proceeds, depending on your cost basis and holding period.

If the buyer is assuming an existing loan, ensure you receive written confirmation from the lender that your personal guarantee has been released. Without this release, you could remain liable if the buyer defaults on the loan.

"An assumption doesn’t automatically relieve you of your personal guarantee. If the new buyer defaults on the loan, the lender could potentially still pursue you as the original guarantor." – RK Kliebenstein, Founder, Self Storage LLC

To navigate the post-sale phase effectively, work with a coordinated team that includes your CPA, estate attorney, and wealth manager. Firms like Oakside Co offer investment-banking-level analysis for transactions, but your post-sale financial strategies should align with your long-term wealth and legacy goals.

Conclusion: Key Takeaways for Self-Storage Exit Planning

A well-thought-out exit plan is the cornerstone of maximizing the sale value of your self-storage facility. Owners who start preparing 12–24 months before listing their property tend to achieve better results. This preparation includes cleaning up financial records, documenting operations, addressing deferred maintenance, and structuring a tax strategy ahead of time.

The stakes are high. For example, a $20,000 income discrepancy or deferred maintenance issues can significantly impact the final sale price – potentially reducing it by $120,000 or even $300,000, depending on valuation multiples. These numbers highlight why early, detailed planning is essential.

"Buying a property without knowing how you’ll divest from it leaves profit on the table." – RK Kliebenstein, Founder, Self Storage LLC

It’s critical to establish your tax strategy, legal structure, and transition plans well before listing your property. Whether you’re considering a 1031 exchange, an installment sale, or an all-cash deal, having a clear strategy in place early is non-negotiable. The right plan, combined with expert guidance, can make all the difference. Partnering with a team of professionals – such as a CPA, attorney, and experienced advisors like Oakside Co – ensures a seamless process from start to finish.

"A successful deal is engineered, not hoped for." – Matthew Horne, Storage Point Advisors

FAQs

What’s my real walk-away number after taxes and fees?

Your real walk-away number is the amount you’ll actually pocket after accounting for taxes, broker fees, transaction costs, and other related expenses. It’s important to calculate this ahead of time so you can see if it matches your desired after-tax proceeds. Having this clarity helps you set realistic expectations and make smarter decisions throughout the sale process.

What valuation gaps most often lower my sale price?

Valuation gaps that can drag down your sale price often stem from differences between your stabilized net operating income (NOI) and the actual income your property is generating. On top of that, deferred maintenance and upcoming capital expenditures can make your property seem less appealing to potential buyers. Tackling these problems ahead of time can go a long way in helping you secure a better sale price.

When does a 1031 exchange beat an outright sale?

A 1031 exchange can be a smarter choice than a direct sale if you’re looking to defer capital gains taxes while reinvesting the proceeds into a like-kind property. This approach helps you retain more capital, opens the door to higher-value opportunities, and supports specific financial or investment goals – as long as you adhere to the strict timelines required for the exchange.