If I sell a self-storage property without a 1031 exchange, taxes can take a big bite out of my equity – often $95,000 to $140,000 on a $400,000 gain.

That’s why this topic matters. A 1031 exchange lets me defer capital gains tax, depreciation recapture, and, in many cases, state tax by moving the sale proceeds into other investment real estate. For retirement planning, that can mean more money left invested, more income options, and less day-to-day work.

Here’s the short version:

- A 1031 exchange is about deferring tax, not avoiding it forever

- The property has to be investment or business real estate

- I have 45 days to identify replacement property and 180 days to close

- If I take cash out, buy down in value, or replace less debt, part of the gain can become taxable

- I can move from active self-storage ownership into lower-touch property or a DST

- My QI must be set up before closing, or the exchange can fail

- For estate planning, a stepped-up basis at death may wipe out deferred gain under current law

A few points stand out. Self-storage owners often face a large tax bill because of years of depreciation. That problem can be even bigger after cost segregation. And for many owners near retirement, the tax issue is only part of it. The other part is simple: they want out of tenant calls, repairs, and daily oversight.

Quick comparison

| Option | Work Level | Control | Liquidity | Best Fit |

|---|---|---|---|---|

| Keep active ownership | High | High | High | Owners who still want to run property |

| Exchange into a lower-touch asset | Medium | Medium to high | High | Owners who want less work but still want direct ownership |

| Exchange into a DST | Low | Low | Low | Owners who want income and no landlord duties |

I’d treat a 1031 exchange as a retirement move first and a tax move second. The main job is to match the next property to the kind of retirement I want: more control, less work, more passive income, or a cleaner estate transfer plan.

sbb-itb-09b4138

The 1031 Rules That Determine Whether an Exchange Qualifies

Before you list the property, get clear on the IRS rules that control the exchange. If you’re planning a retirement exit, these rules help protect the tax deferral that may help fund what comes next.

Like-Kind Property, Same-Taxpayer Rules, and Investment-Use Requirements

Under IRS Regulation §1.1031(a)-3, any U.S. investment real property is like-kind to any other U.S. investment real property. That means a self-storage facility can usually be exchanged for other U.S. investment real estate, such as an apartment complex or vacant land, and still qualify.

There’s a catch, though: the property must be held for investment or for productive use in a trade or business. Personal-use property does not qualify. That includes a primary residence, and it also includes fix-and-flip property held mainly for resale.

The same-taxpayer rule is another big one. The relinquished property and the replacement property must be titled to the same taxpayer. So if you’re thinking about changing entities or shifting ownership as part of retirement, deal with that issue before the property hits the market. A title or entity change at the wrong time can throw the whole exchange off track.

Most boats don’t qualify because Section 1031 applies to real property, not movable vessels. If you think you may have an exception, get a tax advisor to review it first.

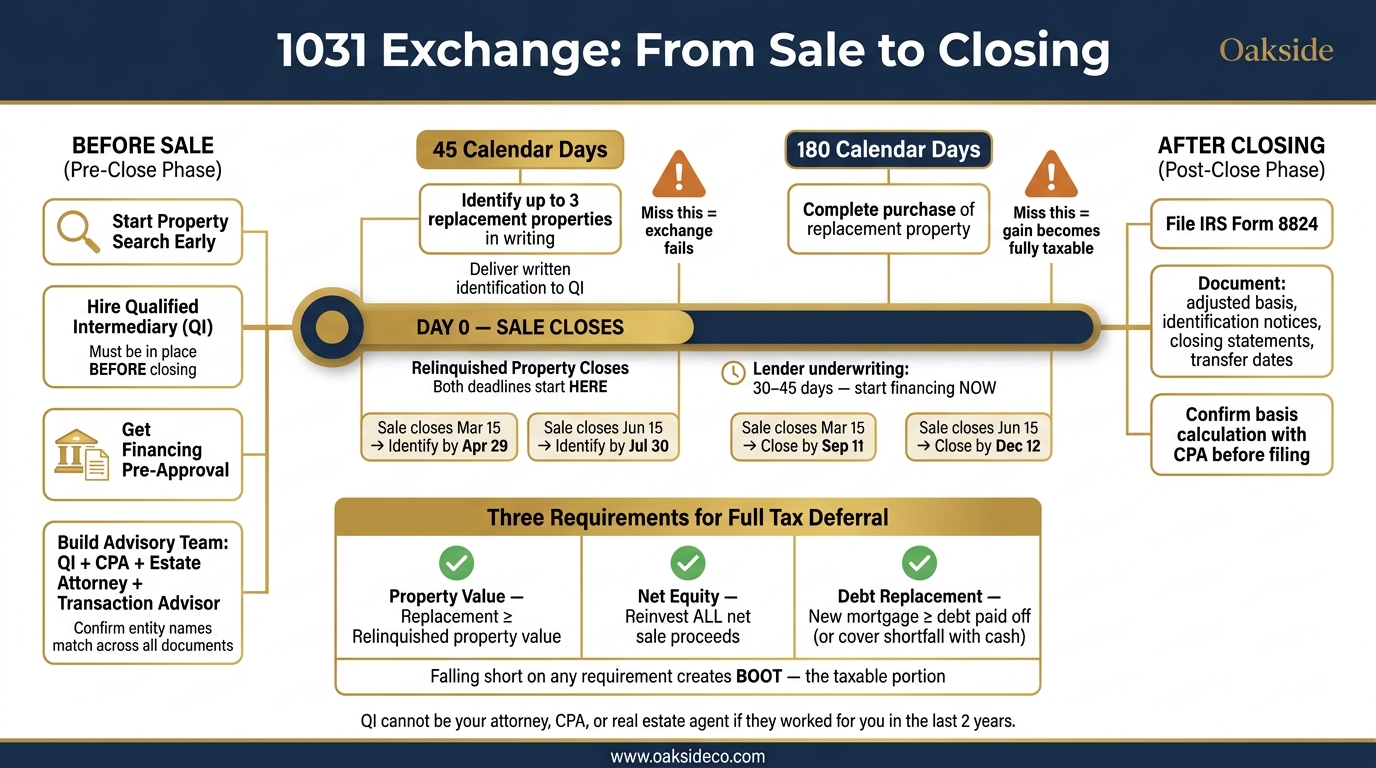

The 45-Day Identification Deadline and 180-Day Closing Window

Both deadlines start on the sale closing date.

You get 45 calendar days to identify possible replacement properties in writing and deliver that identification to your Qualified Intermediary (QI). Then you get 180 calendar days from that same closing date to finish the purchase.

This is where people get tripped up. A lot of owners wait until the sale closes before they start looking. On paper, 45 days can sound workable. In practice, it goes fast. VERY fast. Starting your search before you list gives you more room to compare options, line up financing, and avoid last-minute pressure.

That clock shapes every move that follows, from the search itself to the loan process.

How Boot, Debt Reduction, and Cash Out Can Create Taxable Gain

To get full deferral, you generally need to meet three tests: buy equal or greater value, reinvest all sale proceeds, and replace the debt.

| Requirement | Rule for Full Deferral |

|---|---|

| Property Value | Replacement must be equal to or greater than the relinquished property value |

| Net Equity | All net proceeds from the sale must be reinvested into the replacement property |

| Debt Replacement | New mortgage must equal or exceed the debt paid off, or the shortfall must be covered with additional cash |

If you fall short on any of those points, you may create boot, which is the taxable part of the exchange. Boot can show up in a few ways:

- You receive cash at closing

- You buy a replacement property for less than the sale price

- You take on less debt than you paid off on the relinquished property

This is why it helps to model the deal with a CPA before you lock in the price. A small gap in value, equity, or debt can lead to a tax bill you didn’t see coming.

With the qualification rules in place, the next move is picking the exchange structure and the replacement property that line up with your retirement plan.

Choosing the Right Exchange Structure and Replacement Property

Once you know what qualifies, the next call is how to set up the exchange and what kind of property to buy. Those two choices should line up with how you want retirement to look – not just what’s simplest to get done.

Forward, Reverse, Simultaneous, and Improvement Exchanges Compared

After the rules are clear, the next step is picking the exchange structure that fits your retirement timeline. The forward, or delayed, exchange is the most common. You sell first, then identify and buy the replacement property within the IRS deadlines. The tradeoff is simple: it comes with the most timing pressure.

The other structures each fix a different timing or control issue:

| Structure | Closing Sequence | Execution Difficulty | Timing Pressure | Retirement Problem It Solves |

|---|---|---|---|---|

| Forward (Delayed) | Sell first, then buy | Moderate | High | Standard retirement exit; when the replacement target is not yet secured |

| Reverse | Buy first, then sell | High | Low | Securing a lower-touch asset in a competitive market before your sale closes |

| Improvement | Sell first, then renovate | High | Moderate | Funding upgrades that reduce management intensity before moving into the replacement property |

| Simultaneous | Sell and buy same day | High | Extreme | Rare; requires perfect alignment of two closings |

A reverse exchange costs more – usually $3,000–$6,000, compared with $800–$1,500 for a standard delayed exchange – but it can take away the scramble. It makes sense when the replacement property is tougher to lock down than the property you’re selling. An improvement exchange can help when you want to pay for upgrades that make the next property easier to run, such as climate control or automated entry.

Once you’ve picked the structure, the replacement property should match the amount of day-to-day involvement you want after retirement.

Reinvesting into Self-Storage, Boat/RV, or Other Like-Kind Real Estate

Sticking with a familiar asset class means you can still use the operating knowledge you already have. Some owners use a 1031 exchange to consolidate. They sell several smaller properties and buy one larger, stabilized asset that’s simpler to oversee. Others shift capital into markets with lower property taxes and a friendlier regulatory climate to improve net cash flow.

At the end of the day, the replacement property should support the income you want in retirement.

When Passive Fractional Ownership May Fit Retirement Goals

If you want to step away from active management, fractional ownership may be the best fit. Delaware Statutory Trusts (DSTs) let you exchange into a fractional interest in an institutional-grade property – or a portfolio of properties – while a professional sponsor handles operations. In plain English, a DST can turn sale proceeds into professionally managed fractional real estate, but you give up control and liquidity in exchange for a more hands-off setup.

There’s a catch. DSTs are illiquid, usually with 5- to 10-year hold periods, and you give up operating control entirely. Minimum investments often start at $100,000–$250,000.

Before moving ahead, look closely at:

- The sponsor’s track record

- The fee structure

- How the exit process works

Those decisions shape how fast you need to move, how the deal gets financed, and how smoothly the exchange gets to the finish line. The next step is coordinating the exchange from sale to closing without missing deadlines.

Coordinating the Transaction from Sale to Closing

1031 Exchange Timeline for Self-Storage Owners: Key Deadlines & Steps

Execution matters just as much as structure. You need to hit every deadline, keep the right people in sync, and avoid mistakes with the funds.

Building Your Advisory Team Before the Sale Closes

Your Qualified Intermediary (QI) must be in place before the relinquished property closes. If you receive the sale proceeds directly, the exchange is disqualified. The QI holds the proceeds in escrow and helps keep the exchange in line from day one.

You’ll also want the rest of your team lined up early:

| Advisor | What They Handle in Your Exchange |

|---|---|

| Qualified Intermediary | Holds sale proceeds in escrow; prevents you from taking possession of sale proceeds and helps structure the exchange |

| Tax Advisor / CPA | Evaluates tax consequences, calculates depreciation recapture, and files IRS Form 8824 |

| Estate Planning Attorney | Aligns the exchange with succession goals and entity structure requirements |

| Transaction Advisor | Sources replacement properties and supports disposition strategy, due diligence, and investor positioning |

Your attorney should confirm that the entity names match before closing. If your retirement plan calls for an entity change, do that before closing so the exchange stays intact. And there’s one more rule that can trip people up: if your current attorney, CPA, or real estate agent has worked for you in the last two years, that person cannot serve as the QI.

Once the team is set, time becomes the big pressure point.

Identification, Due Diligence, Financing, and Closing Coordination

Both deadlines start on the sale closing date. That clock does not wait. Lender underwriting can take 30 to 45 days, which means you may have less time than you think to find a property, negotiate terms, clear due diligence, and get to closing.

That’s why financing pre-approval should start during the identification phase, not after it. Waiting too long can put the whole exchange in a bind.

Use the Three-Property Rule to identify up to three replacement properties, no matter their value. This gives you some breathing room. If your top choice falls apart during due diligence, you’re not left scrambling at the last minute.

Here’s how the 2026 calendar works in practice:

| If Your Sale Closes On | Identify Replacement By | Close Replacement By |

|---|---|---|

| Mar 15, 2026 | Apr 29, 2026 | Sep 11, 2026 |

| Jun 15, 2026 | Jul 30, 2026 | Dec 12, 2026 |

Miss either deadline and the gain becomes taxable, unless a federal disaster exception applies.

Reporting the Exchange and Documenting Compliance

After closing, the focus shifts from getting the deal done to proving it was done the right way. File Form 8824 after closing. That form documents the like-kind treatment, adjusted basis carryover, and any boot received.

Your CPA should keep a clear record of:

- Adjusted basis records for both properties

- Written identification notices sent to the QI

- Closing statements

- The dates of each transfer

Those records matter if the IRS ever questions the exchange. Before the return is filed, confirm the basis calculation and filing details with your tax professional.

Retirement Tradeoffs, Succession Planning, and Key Takeaways

Active Ownership, Lower-Management Assets, and Passive Ownership: A Side-by-Side Look

Retirement goals aren’t all the same. Some owners still want control and growth. Others want income without the daily grind. That’s why the replacement property you pick should match the amount of work you want in retirement.

| Ownership Type | Management Burden | Income Control | Liquidity | Best Fit |

|---|---|---|---|---|

| Active ownership | High – tenants, repairs, vacancies | Full operational control | Sell at your discretion | Growth-focused owners still willing to manage |

| Lower-management asset | Moderate – oversight only | Strong, with less day-to-day work | Sell at your discretion | Owners wanting a simpler asset with less management drag |

| DST | Zero – sponsor manages everything | No operating control | Illiquid (typically 5–10 year hold) | Income-focused owners ready to exit landlord duties entirely |

DSTs can work well for retirees who want income without operations. But there’s a tradeoff: you give up control and liquidity in exchange for less work.

Once you’ve settled on the workload you want, the next step is just as important: decide what role the asset should play for your heirs.

How 1031 Planning Connects to Estate and Succession Decisions

A stepped-up basis at death can erase deferred gain under current law.

Before closing, make sure your entity structure matches across all documents. Small mismatches can create big headaches later. If you plan to transfer ownership to a trust or heirs, handle that move before the exchange closes, not after. An estate attorney can help line up the exchange with your succession plan.

What to Confirm Before Starting an Exchange

Before you move ahead, do one last check against your retirement plan:

- Goal: Define the goal: income, simplicity, estate transfer, or all three.

- Reinvestment: Confirm full reinvestment works with your cash needs.

- Debt: Confirm debt replacement works with your financing.

- Deadlines: Calendar the 45-day and 180-day deadlines.

- Team: Line up your QI, CPA, and estate attorney before closing.

A well-structured exchange can keep more equity invested and support both retirement income and later estate transfer.

FAQs

How much tax can a 1031 exchange defer?

A 1031 exchange can defer capital gains taxes, including depreciation recapture. That can sharply reduce the tax bill when you sell.

How much you defer depends on two main things:

- How much the property has gone up in value

- Your own tax situation

So while the tax savings can be meaningful, the exact amount will vary from one owner to the next.

What replacement property fits my retirement goals?

Choose a replacement property that fits your long-term retirement plan, whether you’re focused on growth, income, or estate planning. If your goal is steady retirement cash flow, high-quality self-storage or boat and RV storage assets can be a strong fit.

Your pick should also match how hands-on you want to be and how you’re thinking about legacy planning. Oakside puts the focus on tailored, data-driven strategies to help match a like-kind property to your retirement timeline and goals.

What mistakes can ruin a 1031 exchange?

Common mistakes include:

- Missing strict deadlines to identify or close on replacement properties

- Not using a qualified intermediary

- Failing to meet like-kind property requirements

Slip up on any of these, and the exchange can become a taxable event. In some cases, you may also face penalties.