Selling a storage facility can result in a large tax bill, with up to 40% of your gains lost to taxes like capital gains, depreciation recapture, and state income taxes. To reduce this burden, there are several strategies that let you defer or minimize taxes while reinvesting your profits:

- 1031 Exchange: Defer taxes by reinvesting sale proceeds into another property. Strict deadlines apply.

- Cost Segregation: Accelerate depreciation on assets like paving and fencing to boost cash flow upfront.

- Bonus Depreciation: Deduct 100% of qualifying asset costs in the first year, maximizing savings.

- Installment Sale: Spread tax payments over several years by receiving sale proceeds in installments.

- Deferred Sales Trust (DST): Sell your property through a trust to defer taxes and diversify investments.

Each option has specific rules and benefits. Combining strategies, like a 1031 exchange with cost segregation, can further reduce taxes. Planning ahead and consulting experts ensures you choose the best approach for your situation.

1. 1031 Exchange

A 1031 exchange (outlined under IRC §1031) offers you the chance to sell your storage facility and reinvest the proceeds into another investment property without immediately paying capital gains or depreciation recapture taxes. Instead, these taxes are deferred until you sell the replacement property. If you choose to hold onto the replacement property until your passing, your heirs may benefit from a stepped-up basis, which could eliminate the deferred tax liability altogether.

However, the process comes with strict rules and deadlines. Before your sale closes, you must work with a Qualified Intermediary (QI) to manage the proceeds in a segregated account. If you take possession of the funds yourself, the exchange will be disqualified. Once the sale is complete, you have 45 calendar days to identify potential replacement properties and 180 days to close on the purchase.

The IRS’s "like-kind" rule provides broad flexibility, allowing you to exchange into various property types. These include multifamily apartments, retail centers, raw land, triple-net-leased properties, or even a Delaware Statutory Trust (DST), which offers passive income with minimal management responsibilities. Many investors use this strategy to upgrade from a smaller Class C facility to a larger Class B or A property in a more robust market, all while preserving their equity by deferring taxes. This approach is particularly appealing for RV and boat storage owners, who often face unique asset classifications.

For RV and boat storage owners, it’s essential to separate real property from business assets before selling. Items like land, buildings, and permanent infrastructure qualify for 1031 treatment, while vehicles, inventory, reservation systems, and goodwill are taxed immediately.

The cost of hiring a QI is relatively affordable, typically ranging from $750 to $1,500. To avoid making hasty decisions during the 45-day identification period, it’s wise to begin searching for replacement properties before your current facility sale is finalized. This preparation can help you secure a better investment without feeling rushed.

sbb-itb-09b4138

2. Cost Segregation

Cost segregation shifts components of your storage facility from a 39-year depreciation schedule to shorter 5-, 7-, or 15-year schedules. Instead of waiting nearly four decades to fully depreciate assets, this strategy allows you to front-load deductions, putting money back in your pocket much sooner.

For self-storage and boat/RV facilities, this approach can be especially impactful. Studies often reclassify 20% to 40% of a facility’s depreciable basis into shorter-lived asset classes. Boat and RV storage properties, with their extensive land improvements like paving, fencing, and canopy structures, often see even higher reclassification percentages. Here’s a breakdown of how storage assets are categorized:

| Asset Category | Recovery Period | Storage Examples |

|---|---|---|

| Personal Property | 5 or 7 Years | Security cameras, keypads, gate operators, removable partitions, tenant kiosks |

| Land Improvements | 15 Years | Paving, fencing, motorized gates, exterior lighting, storm drainage |

| Structural Building | 39 Years | Foundation, load-bearing walls, roof, core plumbing/electrical |

This accelerated depreciation strategy pairs well with other tax deferral techniques, creating opportunities for even greater savings.

The financial impact can be substantial. For example, a $3 million facility could see first-year deductions jump from around $74,000 under a standard depreciation schedule to approximately $900,000 – resulting in about $333,000 in immediate tax savings. Thanks to the One Big Beautiful Bill Act (OBBBA) of 2025, which restored 100% bonus depreciation for qualifying assets placed in service after January 19, 2025, the entire reclassified cost can now be deducted in the first year. When combined with strategies like a 1031 exchange or deferred sales trust, cost segregation becomes a powerful tool for maximizing tax deferral.

Consider a real-world example: a 67,637-square-foot self-storage facility in Sebring, Florida (531 units, built in 2007). A cost segregation study by Engineered Tax Services reclassified 59.88% of its depreciable basis into 5-, 7-, and 15-year property. By 2023, this reclassification resulted in $779,167 of accumulated depreciation compared to $216,746 under the straight-line method – an increase of $562,421.

However, selling without a 1031 exchange can trigger ordinary income recapture on reclassified property, taxed at rates up to 37%. This makes cost segregation most effective when integrated into a broader exit strategy. If a study wasn’t conducted at the time of acquisition, you can still perform a "look-back" study using IRS Form 3115. This allows you to claim missed deductions in the current year without needing to amend previous returns, making it a seamless addition to your tax planning.

Oakside Co specializes in incorporating cost segregation into custom tax strategies for self-storage and boat/RV property owners, helping you boost short-term cash flow while enhancing long-term investment outcomes.

3. Bonus Depreciation

Bonus depreciation takes accelerated depreciation a step further, allowing you to deduct the full cost of qualifying assets in the year they’re put into use. For storage facility owners, this can mean a big boost in cash flow, especially when paired with a cost segregation study. This advantage has been reinforced by recent legislative updates.

Thanks to the One Big Beautiful Bill Act (OBBBA), signed into law in July 2025, 100% bonus depreciation has been permanently reinstated for qualifying property purchased after January 19, 2025. This marks a reversal of the prior phase-down. However, properties under binding contracts signed before January 20, 2025, still qualify for a reduced 40% bonus rate.

Nolen Masserman, Managing Director at Oakside, highlights the impact of this change:

"100% bonus depreciation is a game changer for storage facility owners – it enables the immediate write-off of eligible asset costs, boosting cash flow and supporting strategic reinvestments." – Nolen Masserman, Managing Director at Oakside

Boat and RV storage facilities, in particular, are well-positioned to benefit from this provision. These types of properties often include a significant amount of 15-year land improvements, such as paving, fencing, wash stations, drainage systems, and canopy structures, all of which qualify for the 100% deduction. For example, with a $5 million facility purchase, identifying $1.5 million in 5- to 15-year property could result in a $1.5 million first-year deduction.

Unlike Section 179, bonus depreciation doesn’t come with annual dollar caps or taxable income limits. This means it can create a net operating loss (NOL) that can be carried forward to offset future income. However, some states – like California, New York, and New Jersey – don’t align with federal bonus depreciation rules, which could leave you owing state taxes on income that’s federally sheltered. To navigate these complexities, it’s essential to consult a qualified CPA familiar with your state’s regulations.

4. Installment Sale

After exploring strategies like 1031 exchanges and bonus depreciation, installment sales present another option for handling significant gains. This approach allows you to defer tax liability by spreading out the recognition of capital gains over time, as you receive principal payments. Governed by IRC Section 453, installment sales typically span 3–7 years, making it easier for storage facility owners to manage large gains while potentially staying in a lower capital gains tax bracket.

Here’s how it works: Each payment is divided into three parts – taxable gain, tax-free return of basis, and interest income – using the gross profit ratio (gross profit divided by the contract price). This structure can improve after-tax outcomes by 5–15% compared to a lump-sum sale. However, there are some recapture risks to keep in mind.

If cost segregation or bonus depreciation was used, you’ll face Section 1245 recapture for equipment and fixtures, which must be paid in full during the sale year. Meanwhile, Section 1250 recapture on the building is capped at 25% and is spread out as payments are received. This is especially important for boat and RV storage facilities, which often include personal property like fencing, canopies, and security systems that depreciate quickly under Section 1245. With the reinstatement of 100% bonus depreciation under the One Big Beautiful Bill Act, sellers in 2026 could face a larger recapture cash obligation than in previous years. To prepare, ensure your down payment is sufficient to cover the first year’s tax liability before finalizing the terms of the note.

Installment sales also offer flexibility in deal structuring. Seller notes typically account for 10–30% of the purchase price, with interest rates ranging from 5–9%, as long as they meet or exceed the IRS Applicable Federal Rate to avoid falling into the Original Issue Discount trap. This structure can help bridge valuation gaps, attract buyers who may not qualify for traditional financing, and provide a steady income stream. Unlike a 1031 exchange, it eliminates the stress of the 45-day property identification deadline. The downside? Acting as the lender comes with credit risk, so thoroughly screening potential buyers is crucial.

5. Deferred Sales Trust

The Deferred Sales Trust (DST) is a powerful tool for property owners looking to defer taxes while maintaining control over reinvestment and income timing. Using IRC Section 453, this strategy allows you to spread out capital gains tax payments over time, offering a flexible alternative to other tax deferral methods. For owners of self-storage facilities or boat/RV properties with significant appreciation, the DST can be an excellent option for managing a sale.

Here’s how it works: Before closing the sale, you transfer your property into an irrevocable trust managed by an independent trustee. The trust then sells the asset and holds the proceeds. In return, you receive payments through a promissory note over a period of 10–20 years. The key tax advantage? You only pay capital gains tax on the principal portion of each payment as you receive it, rather than on the entire gain upfront. For instance, on a $5 million sale with a $1 million cost basis, this could mean deferring approximately $952,000 in federal taxes that would otherwise be due immediately.

One standout benefit of a DST compared to a 1031 exchange is the freedom to diversify investments. Once the trust holds the proceeds, the funds can be reinvested in a variety of assets, such as stocks, bonds, REITs, or even new business ventures. This flexibility allows you to sell at a market peak, reinvest in diverse assets, and later re-enter the real estate market when prices are favorable – all without the strict timing rules of a 1031 exchange.

"DSTs let you invest proceeds while controlling tax timing and amounts." – Mallon FitzPatrick, CFP®, AEP®, CLU®, Robertson Stephens

However, setting up a DST can be complex and comes with notable costs. Expect to pay legal and setup fees of about 1.5% on the first $1 million of the sale price and 1.25% on amounts above that. Additionally, there’s an annual fee of around 0.5% for the trustee and up to 1% for investment advisory services. This strategy is most effective for transactions with at least $1 million in net proceeds and $1 million in capital gains, where the tax savings can outweigh these costs. It’s also essential to ensure the trustee is independent – otherwise, the IRS may disqualify the deferral. Keep in mind that depreciation recapture is taxed as ordinary income in the year of sale and cannot be deferred.

Nolen Masserman, Managing Director at Oakside, highlights that for owners of highly appreciated self-storage or boat/RV properties, a DST can provide a smooth exit without the reinvestment pressure of a 1031 exchange. When paired with a well-planned disposition strategy, it’s worth exploring. Oakside’s advisory team can help evaluate whether the potential tax savings justify the setup costs based on your specific situation and goals.

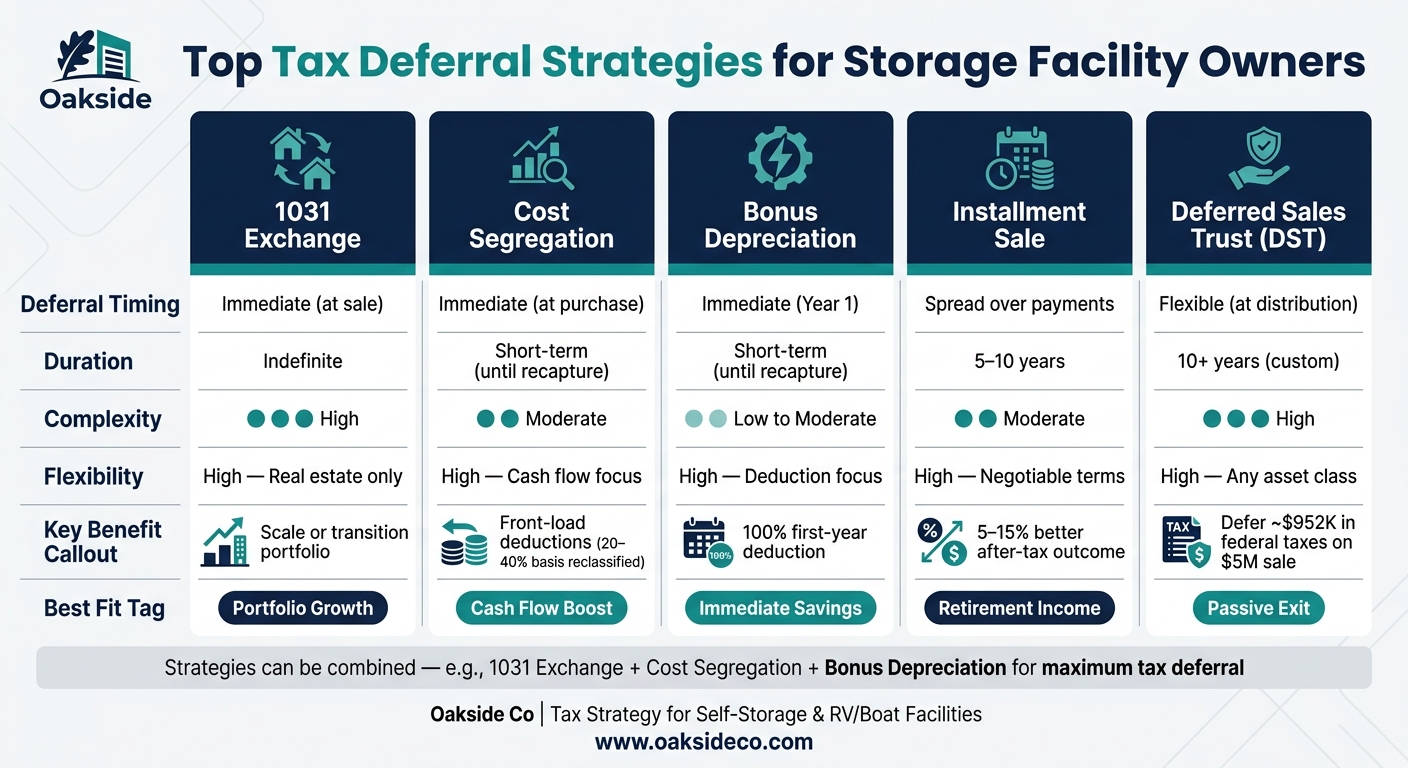

Comparison Table

Top Tax Deferral Strategies for Storage Facility Owners: Side-by-Side Comparison

These strategies vary in timing, duration, complexity, and flexibility. Here’s a quick breakdown to help you compare them:

| Strategy | Deferral Timing | Duration | Complexity | Flexibility | Best Fit for Storage/RV Owners |

|---|---|---|---|---|---|

| 1031 Exchange | Immediate (at sale) | Indefinite | High | High – real estate only | Great for scaling or transitioning portfolios |

| Cost Segregation | Immediate (at purchase) | Short-term (until sale/recapture) | Moderate | High – cash flow focus | Excellent fit; includes many 5-, 7-, and 15-year assets in storage facilities |

| Bonus Depreciation | Immediate (Year 1) | Short-term (until sale/recapture) | Low to Moderate | High – deduction focus | Perfect for site improvements like paving, fencing, and electrical systems |

| Installment Sale | Spread over payments | Life of loan (typically 5–10 years) | Moderate | High – negotiable terms | Suited for retiring owners seeking steady income |

| Deferred Sales Trust | Flexible (at distribution) | Custom (often 10+ years) | High | High – applies to any asset class | Best for owners looking to exit active management |

A few trends become clear when comparing these strategies. The more flexible options, like 1031 exchanges and Deferred Sales Trusts, often come with higher complexity and require professional guidance to execute effectively. On the simpler side, bonus depreciation is straightforward but has a shorter benefit window, as depreciation recapture occurs when the asset is sold.

Storage and RV/boat facilities have a unique advantage: they can leverage accelerated depreciation for specific assets like fencing, paving, and specialized systems. This isn’t something you typically find in other types of commercial properties.

It’s also worth noting that these strategies can be combined. For example, you could execute a 1031 exchange into a new property, conduct a cost segregation study, and apply bonus depreciation to create significant paper losses in the first year. Combining strategies like this can significantly lower your overall tax burden.

The right choice depends on your tax situation, investment goals, and timeline for exiting active management. As Cameron Vale, President at Oakside, points out, the most effective results often come from thoughtfully layering these strategies. It all starts with understanding how each one fits into your broader plan.

Conclusion

Each approach works best depending on where you are in your investment journey – whether you’re aiming to expand your portfolio, maintain consistent cash flow, or prepare for an exit.

Your strategy should align with both your immediate financial needs and long-term objectives. For example, reinvesting earnings might help you grow your portfolio, while creating a reliable income stream could be ideal for retirement. If you’re in a high-income bracket, tools like bonus depreciation can provide a noticeable reduction in your tax burden right away.

One thing is clear: timing is everything. Planning ahead allows you to take full advantage of the tax deferral options discussed. As Nolen Masserman, Managing Director at Oakside, emphasizes:

"Tax planning should begin years ahead of your sale so that tax liability is never an unexpected hurdle at closing." – Nolen Masserman, Managing Director at Oakside

Ideally, you should start planning 6 to 12 months before selling. This timeline gives you enough room to structure your strategy effectively and avoid expensive errors. A well-thought-out plan can save you hundreds of thousands of dollars in unnecessary taxes.

This is where working with an expert advisor can truly pay off. Oakside Co specializes in self-storage and boat & RV assets, offering detailed investment-banking-level analysis and customized, data-driven strategies. Their expertise helps owners choose and implement the best approach for their goals, property types, and timelines. Whether combining strategies like a DST and a 1031 exchange or navigating complex decisions, expert guidance ensures everything runs smoothly. Thoughtful planning and professional advice can make a significant difference.

FAQs

Which strategy fits my exit plan: 1031 exchange, installment sale, or a Deferred Sales Trust?

Choosing the right strategy comes down to your priorities around liquidity, control, and management. A 1031 exchange allows you to defer taxes by reinvesting the proceeds into "like-kind" real estate, which can include passive investments like a Delaware Statutory Trust. Alternatively, an installment sale lets you spread out your tax liability over time, provided you’re comfortable taking on the role of the lender. According to Oakside leaders, the key to success lies in clearly defining your goals and finding the right balance between liquidity and control.

How do cost segregation and 100% bonus depreciation affect depreciation recapture when I sell?

Cost segregation and 100% bonus depreciation are powerful tools for accelerating tax deductions during the early stages of property ownership. However, they don’t erase tax obligations – they simply delay them. When it’s time to sell, the IRS steps in to recapture this depreciation:

- Section 1245 assets (like fixtures) are taxed as ordinary income, with rates reaching up to 37%.

- Section 1250 assets (real property) face a maximum tax rate of 25%.

Understanding these distinctions is key to managing the financial impact when selling your property.

What are the biggest 1031 exchange pitfalls (timelines, QI rules, and asset separation)?

Navigating a 1031 exchange can be tricky, especially if you overlook some of the strict rules set by the IRS. One major challenge is adhering to the tight deadlines. You must identify potential replacement properties within 45 days and complete the purchase within 180 days – or by your tax return due date, whichever comes first.

Another common issue is entity consistency. The same taxpayer or entity that sells the original property must also purchase the replacement property. Failing to maintain this consistency can disqualify the exchange.

Lastly, avoid taking constructive receipt of the sale proceeds. To meet IRS requirements, the funds must stay with a Qualified Intermediary throughout the entire process. Skipping this step could jeopardize the exchange.