Urbanization is reshaping the storage industry in 2026. Smaller living spaces, HOA restrictions, and rising land prices are driving demand for self-storage and boat/RV storage, especially in urban areas. Here’s what you need to know:

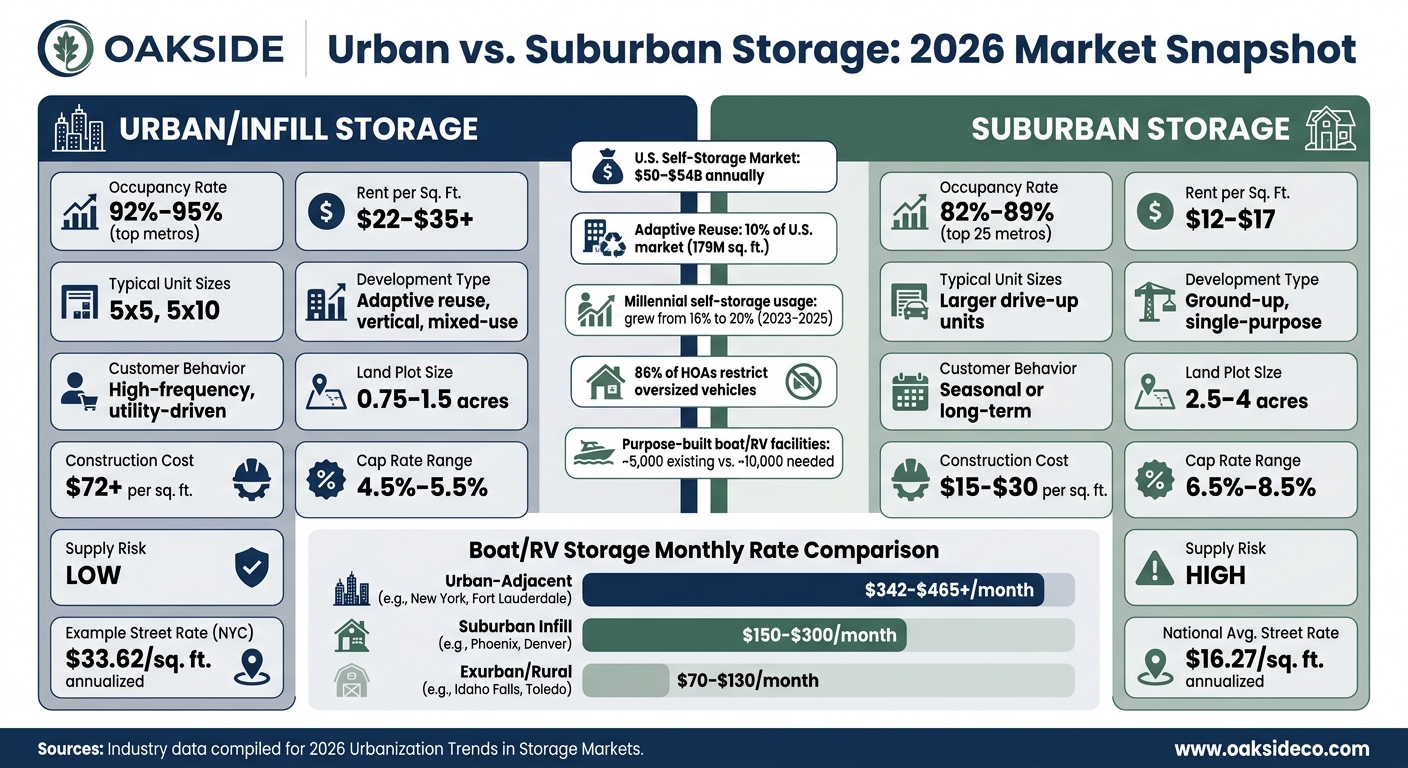

- Self-Storage Growth: The U.S. self-storage market generates $50–$54 billion annually, with Millennials and Gen Z leading the demand. Smaller units (5×5, 5×10) are highly popular in cities due to limited living space. Urban facilities see occupancy rates of 92–95%, compared to 82–89% in suburban areas.

- Boat/RV Storage Challenges: With over 25 million U.S. households owning boats or RVs, urban storage demand far exceeds supply. Urban-adjacent storage is convenient but expensive, while exurban options are cheaper but less accessible.

- Vertical Development: High land costs and zoning restrictions are pushing developers to build multi-story facilities or repurpose existing buildings. Adaptive reuse now accounts for 10% of the self-storage market.

- Technology Integration: Urban storage facilities are leveraging AI, dynamic pricing, and smart security systems to streamline operations and meet customer needs.

- Investor Focus: Institutional investors are prioritizing urban markets with supply constraints, higher rents, and lower competition risks.

Urbanization is redefining storage markets, creating opportunities for developers, operators, and investors to meet growing demand.

Urban vs. Suburban Storage: 2026 Market Snapshot

Trend 1: Smaller Urban Homes Are Driving Demand for Self-Storage

Shrinking Apartment Sizes and Who Is Renting Them

City living often means trading space for convenience. Urban renters are opting for smaller apartments in walkable neighborhoods, giving up extra bedrooms and square footage. This shift has fueled a growing need for self-storage to make up for the lost space. Millennials are at the forefront of this trend, with their self-storage usage climbing from under 16% to nearly 20% between 2023 and 2025. Gen Z is also joining in, with usage increasing from 15.8% to 16.4% during the same period.

Interestingly, it’s not just personal items filling up these storage units. Around 30% of urban storage demand now comes from businesses. Solopreneurs, freelancers, and e-commerce sellers are using storage units to house inventory and streamline last-mile logistics. In these dense urban areas, self-storage has become a practical solution for both individuals and businesses alike.

Why Small Storage Units Are in High Demand in Cities

With less living space available, compact storage units are becoming a necessity. In bustling urban markets, smaller units like 5×5 and 5×10 are the most popular. They strike a balance between affordability and convenience, making them perfect for storing seasonal items, extra furniture, or even business supplies. For many renters, these units act as a substitute for the "garage" that their high-rise apartments lack.

Adding to the appeal, many urban buildings don’t offer dedicated storage spaces, and HOA rules often limit what can be stored on-site. Climate-controlled units are especially popular in cities, offering protection for sensitive items. These units come at a premium, costing 25% to 40% more per square foot compared to traditional drive-up storage.

Urban Infill vs. Suburban Storage: How They Compare

Urban and suburban storage options cater to different needs and lifestyles. Urban renters tend to visit their storage units more frequently, treating them as an extension of their home. Suburban customers, on the other hand, are more likely to use storage for seasonal or long-term purposes.

| Feature | Urban Infill Storage | Suburban Storage |

|---|---|---|

| Occupancy Rate | 92%–95% in top metros | 82%–89% in top 25 metros |

| Rent per Sq. Ft. | $22–$35+ | $12–$17 |

| Typical Unit Size | 5×5, 5×10 | Larger units with drive-up access |

| Customer Behavior | High-frequency, utility-driven | Seasonal or long-term |

| Development Type | Adaptive reuse, vertical, mixed-use | Ground-up, single-purpose |

These distinctions highlight how urban storage is designed to meet the needs of frequent users in tight spaces, while suburban storage focuses on larger, more traditional layouts for occasional use.

sbb-itb-09b4138

Trend 2: Land Scarcity Is Pushing Storage Developments Vertical

High Land Values and Growing Competition in Urban Markets

As cities expand and land becomes harder to find, storage developers are being forced to think differently. The result? Taller buildings and creative reuse of existing spaces.

Urban developers now work with much smaller plots – sometimes as little as 0.75 to 1.5 acres – leading to vertical storage facilities with 3 to 7 floors. Compare this to suburban storage developments, which typically need 2.5 to 4 acres for drive-up access. The cost difference is staggering: climate-controlled urban storage runs over $72 per square foot, while suburban drive-up facilities cost only $15–$30 per square foot. However, in cities like Los Angeles ($13.11/sq. ft. annualized), San Francisco ($11.74/sq. ft.), and New York ($11.07/sq. ft.), higher rents make these costs feasible.

Zoning regulations are also tightening. Chicago, for example, banned new self-storage facilities in most business and downtown areas starting May 2025. Denver prohibits new builds within a quarter mile of light rail stations, and Providence, Rhode Island, has completely banned new self-storage developments. These restrictions are forcing developers to find creative alternatives, such as multi-story buildings or repurposing existing structures.

Multi-Story Builds and Adaptive Reuse Projects

When building from the ground up becomes too expensive or complicated, repurposing existing buildings – known as adaptive reuse – offers a practical solution. This approach can cut development costs by 37%–50% per square foot compared to new construction. It also speeds up the process, as repurposed projects often avoid the lengthy permitting delays that can stretch 6 to 18 months for new builds.

Adaptive reuse is gaining traction, now accounting for about 179 million square feet – or 10% – of the U.S. self-storage market. In some cities, like Chicago, 100% of new storage projects fall into this category. Chicago alone has converted 4.4 million square feet of space into storage, representing 36% of its local inventory.

A standout example is Stuf Storage’s collaboration with landlords like Vornado and Hines. They transformed underused office spaces, such as the windowless cores of buildings, into high-demand storage solutions. One project at 47 William Street in Manhattan’s Financial District highlights this trend.

However, not all buildings are created equal. Office buildings often need structural upgrades to meet the 125–150 pounds per square foot load requirements typical for storage facilities. Retail spaces, especially large "big box" stores with clear heights of 22 feet or more, are easier to convert. These spaces can accommodate mezzanines and multi-level storage without major structural changes.

Another example comes from Los Angeles, where Banner Storage Group completed Catalina Self-Storage in Koreatown in November 2025. Built on just 0.56 acres, this seven-story, 1,500-unit facility sits above an active LA Metro Purple Line tunnel. The project took over two years to gain approval due to strict structural load limits, which made heavier uses like multifamily housing unfeasible.

Boat/RV Storage Options in Urban Settings

Boat and RV storage developers face similar challenges in urban areas, where oversized vehicles require more room than is typically available. To address this, many are turning to dry-stack storage, a vertical system where forklifts stack boats in multi-level indoor facilities. This setup maximizes space while keeping vehicles accessible.

The demand for these solutions is growing. The U.S. dry-stack boat storage market was valued at $390.5 million in 2024 and is expected to reach $773.9 million by 2030, with a compound annual growth rate (CAGR) of 12.2%. In urban-adjacent coastal markets, these facilities are often the only option for boat owners who want convenient access without traveling far from the city.

But these facilities don’t come cheap. Outdoor paved stalls cost about $15 per square foot, while multi-level, climate-controlled boat storage can exceed $72 per square foot. Despite the steep costs, vertical storage remains the most practical way to meet the growing demand in areas where land is at a premium. This trend is reshaping the way urban storage solutions are designed and valued.

Trend 3: Urban Living Is Complicating Boat and RV Storage

Boat and RV Ownership Trends in Urban and Suburban Areas

Boat and RV ownership in the U.S. is still widespread, but the dynamics are shifting. Younger buyers are entering the market, with the median age of RV owners dropping from 53 in 2021 to 49 in 2025. Many of these younger owners live in suburban or urban areas where space is limited, making it harder to store large vehicles at home. Adding to the challenge, RVs are getting larger. Class A motorhomes can now stretch up to 45 feet, and features like slide-outs add even more width. Meanwhile, newer residential developments often have tighter side-yard setbacks – some as narrow as 7.5 feet. These factors are pushing owners to consider off-site storage options, balancing proximity against cost.

Urban-Adjacent vs. Exurban Boat/RV Storage: A Comparison

As demographics shift, boat and RV owners are increasingly weighing convenience against affordability when choosing storage solutions. Here’s how the options stack up:

Urban-adjacent storage facilities, located near dense residential areas in cities like Phoenix, Denver, and Austin, offer unmatched convenience but come at a premium. For instance, average monthly rates are $465 in New York, $447 in Fort Lauderdale, and $342 in San Diego. These facilities often include amenities like wash bays, 30-amp power hookups, and wide drive aisles, justifying their higher costs.

On the other hand, exurban storage facilities – typically 30 to 60 minutes outside city centers – are much more affordable. In markets like Idaho Falls, Idaho ($99/month) and Toledo, Ohio ($102/month), rates can drop below $100/month. However, the trade-off is the time and effort required to retrieve the vehicle, which might discourage frequent use.

| Storage Location | Avg. Monthly Rate | Key Trade-Off |

|---|---|---|

| Urban-Adjacent (e.g., New York, Fort Lauderdale) | $342 – $465+ | High cost, maximum convenience |

| Suburban Infill (e.g., Phoenix, Denver) | $150 – $300 | Balanced access and pricing |

| Exurban/Rural (e.g., Idaho Falls, Toledo) | $70 – $130 | Lowest cost, longest travel time |

How HOA Rules and Parking Limits Are Affecting Storage Demand

Regulations from HOAs and municipalities are tightening, leaving many owners with no choice but to seek off-site storage. Over half of all HOAs in the U.S. prohibit parking boats, trailers, and RVs in driveways or yards. In Florida, HB 1203, effective July 1, 2024, explicitly allows HOAs to enforce such bans when vehicles are visible from the street or common areas. Cities are also stepping up restrictions. In 2024, Los Angeles added 30 streets to its RV parking ban list, while San Jose launched a $3.3 million pilot program in 2026 to enforce oversized-vehicle restrictions. Charleston, South Carolina, limits trailers longer than 20 feet to just one hour of parking on residential streets.

These rules are exacerbating the gap between boat and RV ownership and available storage. Currently, there are fewer than 5,000 purpose-built facilities nationwide, but industry estimates suggest the need for closer to 10,000. The growing demand for off-site storage highlights the strain urbanization is placing on storage markets, setting the stage for operational and investment strategies in the trends to come.

Trend 4: Technology Is Changing How Urban Storage Facilities Operate

Smart Storage Tools Gaining Ground in Urban Facilities

Urban storage facilities are increasingly turning to technology to tackle rising operational costs and limited staffing. For example, 10 Federal Storage now uses an AI-powered system to handle nearly 80% of inbound calls – a dramatic leap from just 10% in early 2025. This shift allows staff to focus on more complex customer needs. Meanwhile, dynamic pricing algorithms are becoming a game-changer. These tools adjust rates daily by analyzing data like real-time occupancy, competitor pricing, and rental trends. This approach has helped Extra Space Storage maintain an impressive Q1 2026 same-store occupancy rate of 93.0%. These tech advancements are reshaping how urban storage facilities cater to the unique needs of city dwellers.

How Urban Storage Facilities Are Adapting for City Customers

Beyond smart tools, urban storage facilities are rethinking how they interact with customers and handle security. Given that many city renters prefer managing their storage entirely through smartphones, online leasing has become a must-have feature. For instance, SmartStop Self Storage saw over 10,000 online reservations in April 2026, marking a 25% year-over-year increase. While some customers opt for a fully digital experience, others still value having the option for in-person assistance when needed.

Security is another area getting a tech upgrade, especially in densely populated urban areas. Facilities are deploying advanced systems like license plate recognition, individual unit alarms, motion-activated lighting, and AI-powered video analytics. These tools not only enhance security but also streamline operations. In one case, OnTrac Storage used AI to analyze gate logs, quickly identifying the access point used by a theft ring and significantly cutting down on manual review time.

Digital Tools in Urban Boat/RV Storage Operations

The wave of digital innovation is also transforming boat and RV storage operations, aligning with trends seen in self-storage. Approximately 36.7% of these facilities – about 3,823 locations – now offer confirmed 24/7 access via cloud-based gate systems. Some premium facilities near urban areas are taking it a step further by using digital reservation platforms to provide bundled concierge services. These services can add an extra $50 to $150 in monthly revenue per tenant, helping operators achieve NOI margins of 70% to 74%.

Trend 5: Institutional Investors Are Rethinking Urban Storage Portfolios

Urban vs. Suburban Storage: What Investors Are Prioritizing

The performance gap between urban and suburban storage markets is becoming impossible to overlook. Institutional investors are now leaning toward supply-constrained gateway cities rather than Sunbelt suburbs, where an influx of new developments has led to falling rents. Meanwhile, Midwest and Northeast metros are showing modest but steady rent increases.

The numbers tell the story. In New York City, annualized street rates average $33.62 per square foot – more than twice the national average of $16.27 per square foot. Urban areas like New York benefit from high land costs and strict zoning laws, which create barriers to new competition. Suburban markets, lacking these protections, face greater risks from oversupply.

| Market Type | Rent Trend | Supply Risk | Cap Rate Range |

|---|---|---|---|

| Urban/Gateway | Stabilizing/Positive | Low | 4.5%–5.5% |

| Suburban/Sunbelt | Negative/Compressed | High | 6.5%–8.5% |

(Source:)

To break into dense urban markets, investors are increasingly turning to adaptive reuse projects. For instance, Stuf Storage has teamed up with institutional landlords to transform underutilized office spaces into tech-enabled storage facilities in major cities. This approach not only avoids many zoning challenges but also monetizes otherwise idle real estate.

How Underwriting Changes for Urban Storage Projects

Urban storage investments come with unique challenges that demand a tailored underwriting strategy, particularly when it comes to navigating regulatory hurdles and revenue models. Unlike suburban ground-up developments, urban projects must account for entitlement risks. For example, in May 2025, the Chicago City Council passed an ordinance restricting self-storage construction in most business and downtown zones to prioritize housing and job-creating developments. Cities like Providence and New York have introduced similar measures.

Another key focus for underwriters is the growing disparity between in-place contract rents and advertised street rates. By Q4 2025, this gap had widened to 69% for some operators. This dynamic makes Existing Customer Rate Increases (ECRIs) an essential tool for boosting revenue, rather than a secondary option. Additionally, higher replacement costs in urban environments significantly impact both initial investment and long-term financial planning.

"What investors are betting is that the low rent growth we’ve seen and the supply constraints will drive above-average rental growth over the next five to seven years." – Nolen Masserman, Managing Director at Oakside

Despite these complexities, institutional confidence in the sector remains strong. In March 2026, Public Storage announced a $10.5 billion all-stock acquisition of National Storage Affiliates (NSA), signaling that large-scale consolidation remains a key strategy.

These challenges highlight the importance of strategic advisory solutions for navigating urban storage investments.

How Oakside Supports Urban Storage Portfolio Decisions

Investing in urban storage requires more than just market knowledge. It calls for precise, data-backed analysis at every stage. Oakside Co partners with institutional investors to simplify the complexities of urban storage deals, from assessing entitlement risks in regulated markets to evaluating revenue assumptions based on rent spread trends.

"Urban storage assets don’t underwrite like suburban deals. The regulatory environment, the replacement cost, and the rent structure all require a different lens – and that’s exactly where having the right advisory team changes the outcome." – Nolen Masserman, Managing Director at Oakside

Oakside’s in-depth, investment-banking-level analysis helps clients identify truly supply-constrained urban assets and anticipate potential zoning delays that could derail deals. For institutional clients managing acquisitions or dispositions in gateway markets, these insights directly shape pricing strategies, holding periods, and exit plans.

Conclusion: Key Takeaways on 2026 Urbanization Trends in Storage

How Urbanization Creates Demand and Drives Change in Storage Markets

Urbanization is pushing storage demand to new heights. Smaller apartments, stricter zoning laws, and HOA restrictions are making storage solutions more essential than ever. For example, 86% of HOAs restrict oversized vehicles on residential properties, and around 77 million Americans live in community associations. This creates a strong foundation for demand, not just for traditional self-storage but also for specialized options like boat and RV storage.

By 2026, the way storage facilities are built is shifting. Instead of relying on traditional ground-up construction, developers are turning to adaptive reuse projects in densely populated areas. Companies like DXD Capital are even designing storage facilities that mimic residential townhomes to better align with local aesthetics and win municipal approval. The days of plain, windowless storage buildings are quickly fading.

What These Trends Mean for Storage Investment Strategies

These changes in demand are reshaping the way investors approach storage markets. Supply constraints are becoming a major advantage, especially in high-cost, heavily regulated areas like New York, where street rates have reached $33.62 per square foot. Meanwhile, the RV and boat storage market is expanding at a 12.5% annual growth rate through 2031, driven by a supply gap that requires significant growth to meet demand.

For investors, focusing on the right asset types and locations is key. Urban-adjacent facilities, such as micro-storage infill projects, vertical multi-story builds, and HOA-friendly RV and boat storage options, are outperforming older suburban drive-up facilities. Additionally, revenue management strategies are evolving, with ECRIs (Enhanced Cost Recovery Initiatives) now playing a central role in boosting net operating income.

Closing Thoughts from Oakside Co

Urban storage investments come with unique challenges, from navigating entitlement hurdles to dealing with higher replacement costs. These risks require carefully tailored strategies.

Cameron Vale, President at Oakside, puts it this way:

"The investors who will outperform in this cycle are the ones who understand that urban storage isn’t just a real estate play – it’s an infrastructure play. And infrastructure in supply-constrained markets doesn’t stay cheap for long." – Cameron Vale, President at Oakside

Oakside Co collaborates with institutional clients to simplify the complexities of urban storage investments. Whether it’s assessing adaptive reuse opportunities in regulated markets, testing revenue assumptions against rent trends, or preparing assets for optimal sale, having the right advisory partner isn’t just helpful – it’s a critical advantage in this competitive landscape.

FAQs

Why are urban storage rents so much higher than suburban?

Urban storage rents tend to be higher because of the limited availability of facilities in densely populated areas. Challenges like zoning restrictions, entitlement risks, and a lack of suitable land make it difficult to develop new properties. According to Nolen Masserman, Managing Director at Oakside, this shortage, paired with elevated land values and operating costs, gives operators the ability to maintain stronger pricing. In contrast, suburban markets often face oversupply and heightened competition, which can drive rents down and force operators to offer concessions.

How do zoning bans change where new storage can be built?

More and more municipalities are reshaping their zoning rules, prioritizing land for housing or commercial purposes. This shift often pushes self-storage developments into industrial zones, limiting where these facilities can be built. In some cases, storage projects are outright banned near transit hubs, further narrowing available options.

Nolen Masserman, Managing Director at Oakside, explains that these zoning challenges are driving investors to get creative. Instead of focusing solely on standalone facilities, many are turning to adaptive reuse or mixed-use projects to navigate stricter approval processes. These approaches allow developers to work within zoning constraints while meeting local demands.

Is urban-adjacent boat/RV storage worth the higher monthly cost?

Yes, paying extra for storage near urban areas often makes sense. In densely populated regions, limited garage space and restrictions from HOAs on parking in driveways or yards make off-site storage a necessity. These facilities are convenient and easy to access, fitting smoothly into everyday routines. As Oakside Co points out, being close to residential neighborhoods boosts demand, maintaining strong pricing and long-term value for these sought-after, often undersupplied properties.