The self-storage industry is rapidly consolidating, with large institutional players like REITs and private equity firms acquiring smaller, family-owned facilities. Independent ownership has dropped from 82%-85% in 2010 to around 70%-72% in 2025, with projections suggesting further declines to 60%-65% by 2030. This shift is reshaping how sellers approach exit strategies, presenting both opportunities and challenges.

Key takeaways:

- Institutional Buyers Are Driving Demand: Large players prioritize facilities with operational inefficiencies they can improve, often paying premiums for properties with growth potential.

- Market Consolidation Is Accelerating: Major acquisitions, like Public Storage’s $10.5 billion deal for National Storage Affiliates in 2026, highlight the trend.

- Timing Matters: The market is transitioning from oversupply to stabilization, with mid-2026 to 2027 being a favorable window for sales as demand remains strong.

- Local Factors Are Critical: Supply constraints, zoning restrictions, and housing market trends heavily influence valuations and timing.

To maximize exit value, sellers should focus on improving operations, aligning with institutional standards, and timing their sale based on market conditions. Engaging specialized advisors can also help navigate this evolving landscape effectively.

Trends Driving Consolidation in Storage

Fragmented Ownership and Institutional Growth

The U.S. self-storage market is undergoing a rapid transformation, shifting from its traditionally fragmented structure toward greater consolidation. Back in 2010, independent operators controlled around 82%–85% of the market. Fast forward to today, the "Big Five" players – Public Storage, Extra Space, CubeSmart, Life Storage, and National Storage Affiliates – now account for nearly 35% of the total market, more than doubling their share from 15% a decade ago.

One of the key factors driving this shift is generational turnover. Many of the original owners who built facilities during the 1980s and 1990s are aging into their 60s, 70s, and beyond. With fewer family members willing to take over these businesses, selling has become the most logical path forward.

Adding to this trend is the performance gap between independent operators and larger institutional players. Institutional operators, leveraging AI-driven dynamic pricing at over 90% of their facilities, generate 10%–20% more revenue per square foot compared to independents, who have adopted such technology at a much lower rate of 15%–20%. This widening disparity is pushing more independent owners to sell, reshaping the ownership landscape and fueling the consolidation trend.

M&A Activity and Recent Transactions

The wave of mergers and acquisitions (M&A) is a clear sign of the market’s ongoing consolidation. One of the most notable deals came in March 2026, when Public Storage (PSA) announced its acquisition of National Storage Affiliates Trust (NSA) in an all-stock transaction valued at approximately $10.5 billion. Set to close in Q3 2026, this deal will add over 1,000 properties and 69 million rentable square feet to PSA’s portfolio. Once completed, PSA will oversee more than 4,500 facilities, with a combined enterprise value of $77 billion. The company has also secured $4 billion in financing to refinance NSA’s existing debt.

"With the launch of the PS4.0 strategic vision focused on accelerated per share earnings and cash flow growth, this transaction will enable us to strategically and accretively expand our platform with assets that are highly complementary with our portfolio." – Joseph D. Russell Jr., CEO, Public Storage

Specialty storage is also seeing consolidation. In February 2026, Go Store It Self Storage, a subsidiary of Madison Capital Group, acquired a four-property boat and RV storage portfolio in the Richmond-Katy area of Houston, Texas. This portfolio, which includes 705 units (560 of them covered or enclosed) and was 94% occupied at the time of sale, was funded through a $250 million joint venture with GEM Realty Capital.

How Capital Markets Are Influencing Consolidation

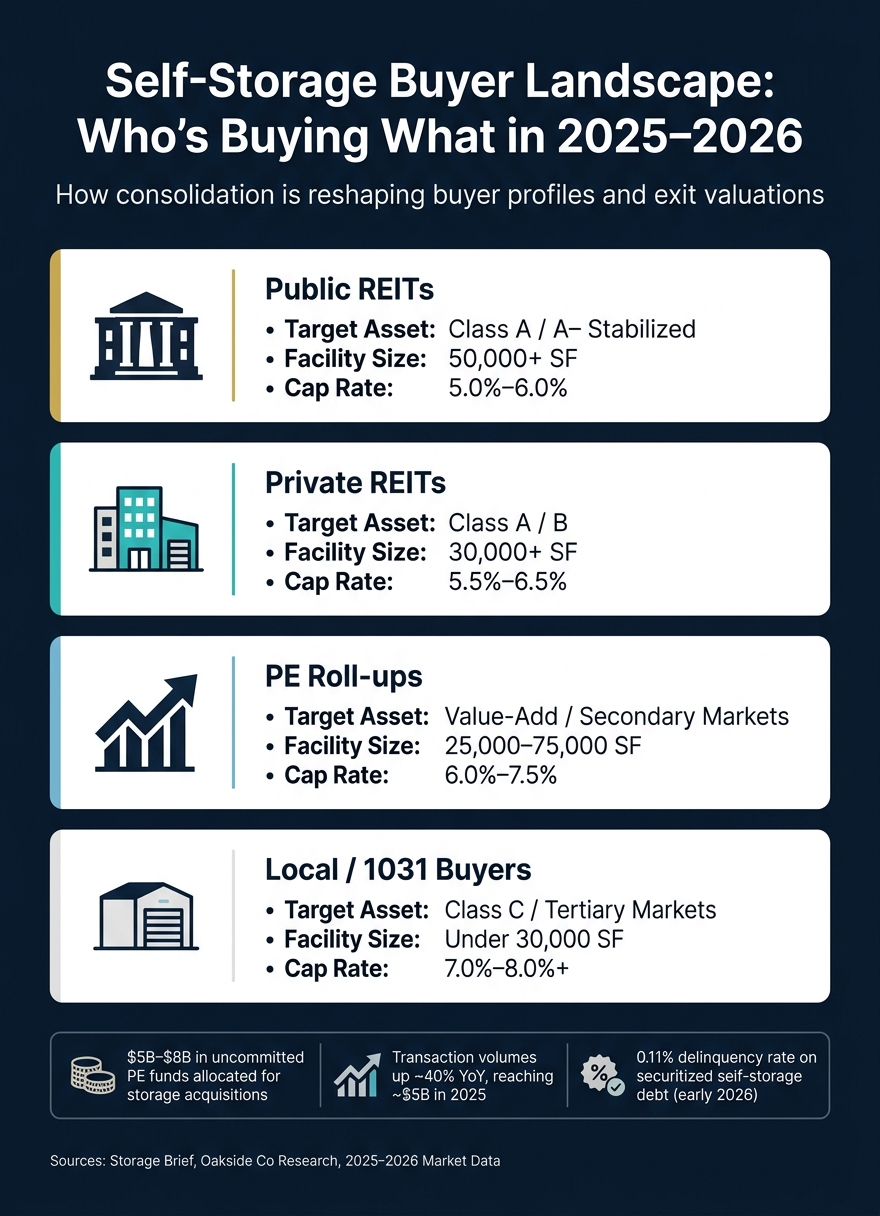

The availability of capital is a major force behind the acceleration of consolidation in the self-storage sector. Transaction volumes in the industry jumped nearly 40% year-over-year, reaching close to $5 billion in 2025. Meanwhile, private equity firms are sitting on an estimated $5 billion to $8 billion in uncommitted funds specifically allocated for storage acquisitions. This financial liquidity is creating significant acquisition momentum.

Self-storage’s appeal to institutional investors stems from its low credit risk. As of early 2026, securitized self-storage debt had an impressively low delinquency rate of just 0.11%. Additionally, real estate investment trusts (REITs) in the sector maintain conservative leverage ratios, averaging between 4.2x and 4.8x net debt to EBITDA.

New sources of capital are also emerging. For the first time, sovereign wealth funds from the Middle East and Asia-Pacific are taking an interest in U.S. self-storage investments. Joint ventures are becoming increasingly common, providing well-capitalized buyers with the flexibility to act quickly. For example, CubeSmart partnered with CBRE Investment Management in early 2026 to launch a $250 million joint venture targeting high-growth markets. Similarly, Centerbridge Partners and Reframe Holdings secured a $350 million debt facility from JPMorgan Chase to focus on acquiring Class A and high-quality Class B assets. These capital structures give institutional buyers a competitive edge, often allowing them to outpace smaller operators in acquisitions. The result? Faster deals, shifting valuations, and tighter timelines for sellers looking to exit.

sbb-itb-09b4138

How Consolidation Shapes Exit Strategies

Self-Storage Buyer Tiers: Cap Rates, Asset Types & Deal Sizes (2025–2026)

Changes in Buyer Profiles and Preferences

The landscape of storage asset buyers has shifted significantly, with institutional capital leading the charge. This group includes public REITs, private equity platforms, and sovereign wealth funds, each focusing on specific asset types and utilizing distinct underwriting strategies.

| Buyer Tier | Target Asset Type | Typical Facility Size | Cap Rate Range |

|---|---|---|---|

| Public REITs | Class A/A– Stabilized | 50,000+ SF | 5.0%–6.0% |

| Private REITs | Class A/B | 30,000+ SF | 5.5%–6.5% |

| PE Roll-ups | Value-Add / Secondary | 25,000–75,000 SF | 6.0%–7.5% |

| Local / 1031 Buyers | Class C / Tertiary | Under 30,000 SF | 7.0%–8.0%+ |

Institutional buyers are increasingly targeting properties with manual operations, leveraging the gap in technology to enhance efficiency and profitability.

There’s also a notable shift toward off-market transactions. Active buyers, such as private equity platforms and regional aggregators, are leaning into these deals to sidestep auction premiums and conduct more comprehensive due diligence.

"Buyers are no longer pricing assets solely on trailing performance. They are pricing execution risk, operational clarity, and certainty of close." – Matthew Horne, Storage Point Advisors

Portfolio Sales vs. Single-Asset Deals

This evolution in buyer profiles is influencing not just the types of assets being targeted but also the preferred deal structures.

Portfolio sales are particularly appealing to institutional buyers because they allow for cost efficiencies in rebranding and technology upgrades across multiple locations. On the other hand, single-asset deals – especially those under 30,000 SF – are more suited for local syndicators, small regional operators, and 1031 exchange investors. These buyers typically have smaller capital bases and lower risk tolerances, which often lead to wider cap rates and longer timelines for closing deals. However, private equity roll-up platforms sometimes acquire single assets as part of a strategy to consolidate them into larger portfolios, which can later be sold to institutional buyers at a premium.

"Buying a property without knowing how you’ll divest from it leaves profit on the table." – RK Kliebenstein, Founder, Self Storage LLC

These deal preferences underline the growing importance of key valuation metrics.

Key Metrics That Drive Valuation

The choice of deal structure amplifies the role of critical valuation metrics in shaping exit strategies. Consolidation has changed the way buyers evaluate property value, prioritizing factors like operational clarity, sustainable cash flow, and execution risk over historical revenue performance.

Scale and location are now more crucial than ever. For instance, climate-controlled units can command 25%–40% higher rents compared to standard drive-up units, making the unit mix a powerful driver of valuation. Similarly, Class A properties in top-10 metropolitan areas achieve tighter cap rates compared to Class C facilities in tertiary markets, reflecting the premium placed on location and quality.

Expense scrutiny has also intensified. Rising insurance costs – up by 30%–60% in many markets between 2022 and 2025 – and property tax resets triggered by sales are now significant factors in acquisition pricing. Institutional buyers often "mark to market" rent rolls, reassessing net operating income (NOI) to reflect sustainable market rates rather than inflated occupancy figures driven by concessions or below-market rents.

Firms like Oakside Co help sellers prepare clean, well-documented financials that can withstand rigorous buyer scrutiny. This ensures that a property’s true value is accurately reflected during negotiations. For sellers navigating a consolidating market, understanding these valuation metrics is essential for maximizing exit value.

Timing Your Exit in a Consolidating Market

This section dives into how to strategically time your exit in a consolidating market, building on the buyer profiles and deal structures discussed earlier.

Reading Market Cycles and Their Effect on Pricing

Market consolidation doesn’t follow a straight path – it moves in cycles. Your position in that cycle can significantly impact the price buyers are willing to pay. Right now, the self-storage market is transitioning from an oversupplied phase, marked by lower rents, to a stabilization period. By 2026, new self-storage supply is projected to peak at around 51.1 million net rentable square feet (NRSF), then drop by 25%–30% in 2027, thanks to rising construction costs and tighter lending conditions. As supply tightens, existing properties become more valuable, underwriting improves, and pricing firms up. This makes the mid-2026 through 2027 period a prime window for independent owners to sell while institutional demand is still robust.

Timing matters. For example, one owner delayed selling and saw occupancy fall from 88% to 71%, ultimately selling for 30% less than the 2020 valuation. In contrast, another owner timed the sale to align with buyer preferences and captured premiums by highlighting operational upside.

"The difference between selling at the right time and the wrong time can be hundreds of thousands of dollars on a single facility, and millions on a portfolio." – The Storage Brief

Using Cap Rate and NOI Trends to Time an Exit

Cap rates serve as a key indicator for sellers. National self-storage cap rates hit a low of 5.0% in Q4 2022 but have since stabilized around 5.8%–5.9% by early 2026. This rise – about 80–90 basis points – means buyers are paying less for the same net operating income (NOI). Exit cap rate expectations have shifted from 4.5%–5.0% during the pandemic to 5.5%–7.0% today.

Another critical signal is the shift in street rates. Positive growth in these rates indicates that buyers are ready to base valuations on sustainable market conditions. For instance, national street rates averaged $16.27 per square foot in early 2026, with year-over-year growth improving to +0.3% to +0.9%. Selling during this recovery phase, rather than waiting for it to fully stabilize, often results in better valuations.

However, sellers need to avoid the "cap rate trap." Offering steep rent concessions to boost occupancy before a sale can backfire, as institutional buyers will re-evaluate the rent roll based on sustainable market rates, not inflated figures. Loan terms also play a role. Prepayment penalties like yield maintenance or defeasance clauses can make a sale financially unfeasible if the timing doesn’t align with the loan’s lifecycle. On the flip side, having an assumable low-interest loan can be a strong selling point in a high-rate environment.

Local Market Factors That Affect Timing

While national trends set the stage, local market dynamics ultimately determine the best time to sell. Geography plays a big role. For example, supply-constrained markets like Boston and Los Angeles, where new development pipelines are just 0.7% of existing stock, are seeing rent growth of +11% to +15%. Meanwhile, oversupplied Sun Belt markets like Atlanta are experiencing rent declines of 8%–15%.

In oversupplied areas, it may be wise to wait until the projected 2027 supply drop for better local absorption. On the other hand, in high-barrier markets, the selling window may already be open. Additionally, more than 50 cities – including Atlanta, Chicago, and New York City – have enacted zoning restrictions or moratoriums on new storage development, increasing the scarcity of existing facilities and supporting tighter cap rates.

"The barrier to entry is one of the most important factors in self storage valuations, and regulatory barriers are increasingly supplementing the traditional barriers of land cost and construction expense." – The Storage Brief

Residential real estate trends also tie into storage demand. A rebound in local home sales often signals stronger demand for storage, creating a more favorable selling environment. Similarly, monitoring the 3-mile radius for adaptive reuse projects can help sellers anticipate new competition that could enter the market quickly and at lower costs.

| Local Factor | Impact on Exit Timing |

|---|---|

| Tight zoning / moratoriums | Positive – increases asset scarcity and supports higher exit multiples |

| High supply pipeline | Negative – increases concessions and lowers occupancy; delay until absorption improves |

| Recovering housing market | Positive – stronger demand environment supports buyer confidence |

| Oversupplied Sun Belt market | Caution – wait for the 2027 supply drop to stabilize local competition |

| Midwest / Northeast market | Stable – thinner development pipelines support steady cash-flow exits |

Combining national consolidation trends with local market insights is key to maximizing your exit value. Firms like Oakside Co can assist in mapping local dynamics against broader trends, helping you pinpoint the optimal window where market conditions, asset positioning, and buyer interest align for the best outcome.

How to Maximize Exit Value in a Consolidating Market

Improving Operations and Scale Before a Sale

REIT portfolios typically maintain occupancy rates between 84% and 93.5%, while private assets hover around 82%. Closing that gap before listing your property can directly enhance its value at sale.

One way to bridge this gap is by adopting AI-powered revenue management systems and smart access technologies. These tools help align your operations with institutional benchmarks, reducing execution risks. For example, smart access systems can cut on-site labor costs by up to 50%, directly improving your net operating income (NOI). Together, these upgrades show potential buyers that your property is already operating at a higher standard.

Another important step is cleaning up your financials. Removing personal or partnership expenses from your profit and loss statements (P&L) and clearly marking one-time capital expenditures provide buyers with a clearer view of your stabilized NOI. Addressing deferred maintenance – like fixing aging roofs or cracked paving – can also save you from dollar-for-dollar price reductions during due diligence.

"Your desired outcome should dictate every decision you make while holding the asset. Thinking about this financial goal forces you to reverse-engineer your entire operation." – RK Kliebenstein, Founder, Self Storage LLC

Start planning these changes 12–24 months before listing. Facilities that switch to third-party management during this time often see NOI improvements of 10%–25%. This not only increases your property’s value but also positions it as part of a broader portfolio strategy, which can be appealing to institutional buyers.

Designing a Portfolio With Exit in Mind

Operational improvements are just the first step. Structuring your portfolio for a sale can make it even more attractive to buyers, especially institutional ones like REITs. These buyers tend to favor acquisitions in markets where they already operate, as this creates operational efficiencies. A portfolio concentrated in a single metro area or region is generally more appealing than one spread across unrelated markets.

Another key factor is the inclusion of climate-controlled units, which are increasingly in demand. New developments now consist of 50%–60% climate-controlled space, and these units can command 25%–40% higher rents than standard drive-up units. A portfolio with a strong focus on climate-controlled units aligns with what institutional buyers are actively looking for.

A great example of strategic portfolio building is the February 2026 merger between BlueGate and Go Store It, which created a 189-property portfolio spanning 27 states. Private equity groups often assemble smaller properties into larger portfolios for this exact reason: to meet the scale requirements of REITs or large operators, who need a certain portfolio size to justify transaction costs.

"If your goal is to sell to a real estate investment trust (REIT), you must build something that meets institutional criteria. This means incorporating their standards to ensure you’re an attractive acquisition candidate." – RK Kliebenstein, Founder, Self Storage LLC

Working With a Specialized Advisory Firm

In a market dominated by consolidation, expert advisory services can make a significant difference in your sale outcome. Specialized brokers create competitive bidding environments by marketing your property to a wide pool of qualified buyers – something independent sellers often can’t achieve on their own.

"A facility that is quietly offered to just one or two buyers will likely sell for a lower price than one that is widely marketed to a larger pool of qualified buyers." – Zachary Urow and Sean Ruhlman, Urow Real Estate

Take the 2022 example of Carl, who owned a 45,000 SF facility. By working with a specialized broker, Carl participated in a structured Call-for-Offers process. The winning bid came in at a 5.2% cap rate, based on the buyer’s projected NOI after operational improvements – not Carl’s current performance. This highlights the value of advisors who understand institutional underwriting and can present your property’s potential rather than just its historical performance.

Firms like Oakside Co bring a unique mix of sector expertise and a national network of investors. Their ability to combine in-depth knowledge of self-storage and boat/RV markets with broad buyer reach is particularly valuable in today’s consolidating market. Engaging an advisor 6–12 months before your planned sale allows time to implement any value-add improvements they recommend, ensuring your property is well-prepared to hit the market.

Conclusion: What Consolidation Means for Your Exit Strategy

The storage industry is experiencing a steady transformation. Independent ownership is on track to decline further, potentially reaching just 60%–65% by 2030. This trend significantly narrows the window for sellers to achieve peak exit value.

Timing plays a major role in maximizing exit value. Institutional buyers are aggressively pursuing properties with untapped NOI potential. For instance, Public Storage invested $946 million in acquisitions in 2025, while the $10.5 billion purchase of National Storage Affiliates Trust in April 2026 underscores the vast capital driving this consolidation . As the market consolidates, the number of under-optimized properties diminishes, which in turn reduces buyer urgency.

"The next 12–24 months represent a strategic window for sellers who want to capitalize on strong buyer demand before market dynamics shift." – The Storage Brief

The sellers who achieve the best outcomes are those who plan ahead. This includes organizing financial records, addressing occupancy issues, and targeting the right type of buyer. On the other hand, neglecting these steps – such as allowing deferred maintenance to pile up – can lead to discounts of up to 30% below peak valuations. Proactive planning and strategic upgrades are essential for presenting a property’s full potential.

In this evolving market, thorough preparation is key to aligning your property with institutional standards. Companies like Oakside Co specialize in readying storage assets to meet these standards and connect with the broadest pool of qualified buyers. Preparation isn’t optional – it’s the foundation for a successful exit.

FAQs

Should I sell now or wait another year?

Selling now or waiting depends on your personal goals and the current market landscape. With strong institutional demand and attractive financing options keeping valuations high, it could be a smart time to sell if your priority is cashing out. On the other hand, if you’re aiming for long-term ownership, prepare for a period of market adjustments that could span several years.

To get the best value, focus on keeping your financial records organized and your operating data accurate. Buyers tend to value transparency and preparedness more than lofty projections, so make sure your documentation is clear and reliable.

What upgrades move my sale price the most?

To increase your sale price, focus on upgrades that enhance net operating income (NOI) and attract institutional buyers. Consider integrating modern technology like dynamic pricing tools, AI-driven revenue management systems, and cloud-based platforms. Physical improvements also play a big role – think climate-controlled units, advanced security measures like smart locks and updated CCTV systems, and boosting curb appeal. Oakside Co provides data-driven solutions to help pinpoint and implement these impactful changes.

How do buyers decide what my storage is worth?

Buyers determine the worth of your facility by calculating its Net Operating Income (NOI) – which is your total income minus operating expenses – and then dividing that figure by the market cap rate. Beyond this, they also evaluate aspects such as potential for revenue growth, how efficiently the facility operates, and the specific dynamics of the local market. Oakside Co provides customized, data-driven insights to help you grasp these elements and fine-tune your exit plan.