Interest rates directly impact the cost of financing storage assets like self-storage and boat/RV facilities. Loans are priced based on benchmarks such as SOFR, Prime Rate, or Treasury yields. Key takeaways:

- Lower Rates: Reduce borrowing costs, increase loan amounts, and improve cash flow.

- Higher Rates: Raise debt service costs, tighten cash flow, and increase equity requirements.

- Current Rates (May 2026): Fixed and floating rates have converged (~5.8%), offering stability for long-term loans.

- Loan Types: Bank loans (~5.5%), CMBS (5.75%-7%), life insurance loans (6.25%-7.5%), and bridge loans (9.25%-13%).

Key strategies include aligning loan structures with business plans, refinancing early, and using tools like rate caps and interest-only periods to manage risk. For stabilized assets, fixed-rate loans are attractive, while lease-up projects often require higher-cost bridge financing. Careful financial planning ensures resilience against rate fluctuations.

How Interest Rates Affect Financing Costs and Loan Structures

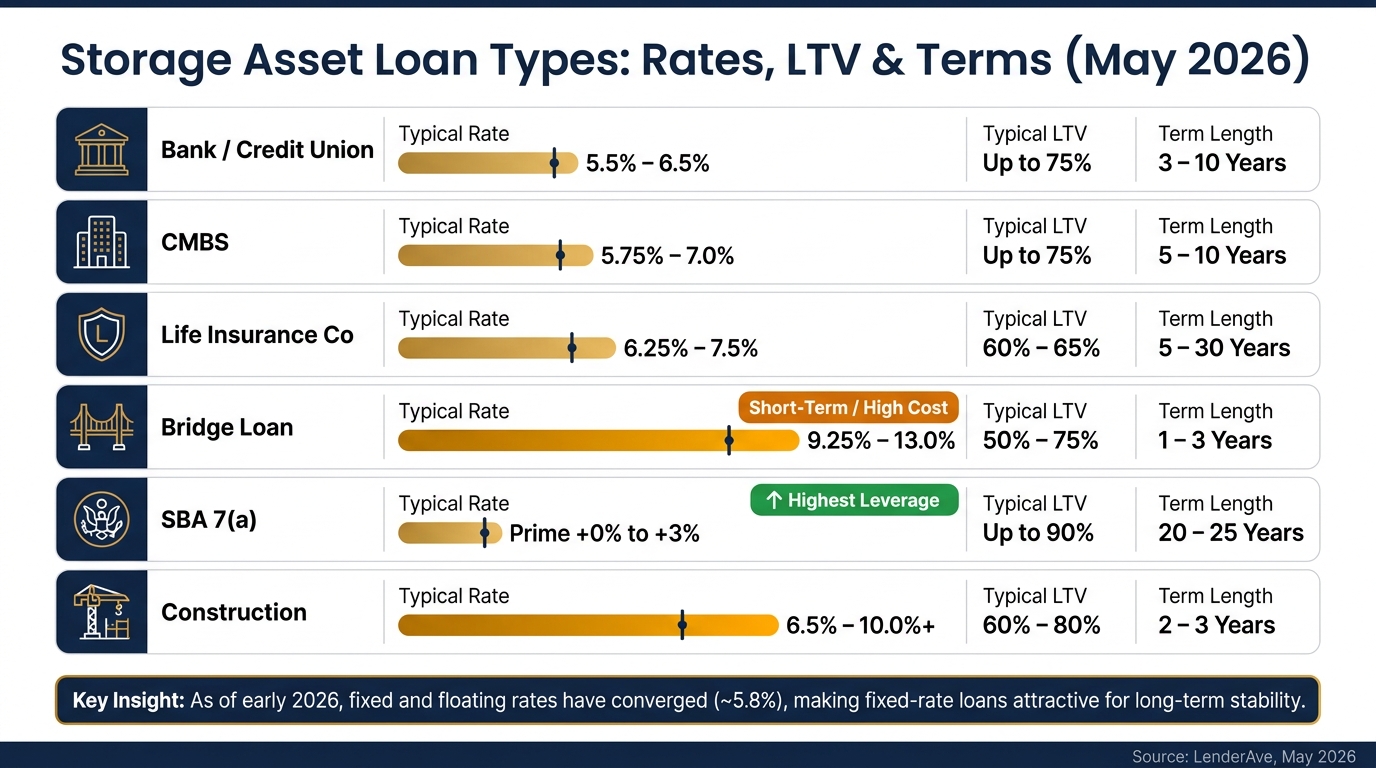

Storage Asset Loan Types Compared: Rates, LTV & Terms (2026)

Interest rates play a key role in shaping financing costs and the types of loans available. When rates rise, debt service costs increase, which can tighten cash flow. On the flip side, lower rates enhance borrowing capacity. The interest rate environment also determines the loan products offered and the terms attached to them.

Fixed-Rate vs. Floating-Rate Loans

Fixed-rate loans – commonly offered by CMBS lenders and life insurance companies – lock in your interest rate for the entire loan term. These loans are typically priced as a spread over the 10-Year U.S. Treasury yield, which, as of April 2026, stands at about 4.27%. Fixed-rate loans provide predictable payments but come with steep prepayment penalties, making early repayment costly.

Floating-rate loans, on the other hand, adjust periodically based on an index like Term SOFR, which averaged 3.66% in the first quarter of 2026. These loans are more flexible for sales or refinancing, as they avoid heavy exit fees, making them a good fit for transitional or value-add projects. However, they carry the risk of rate increases. To mitigate this, lenders typically require borrowers to purchase an interest rate cap.

What’s unusual about the current market is that fixed and floating rates have converged. As of early 2026, SOFR-based floating rates average around 5.84%, nearly matching the 5.86% average for fixed-rate loans. This creates a rare opportunity for borrowers to lock in long-term payment stability without paying a premium, making fixed-rate loans particularly attractive for stabilized, long-term investments.

"If you can lock in a fixed rate at roughly the same cost as floating, the payment certainty comes essentially free." – LenderAve Editorial Team

Here’s a snapshot of current loan options and their typical terms (as of May 2026):

| Loan Type | Typical Rate (May 2026) | Typical LTV | Term Length |

|---|---|---|---|

| Bank / Credit Union | 5.5% – 6.5% | Up to 75% | 3 – 10 Years |

| CMBS | 5.75% – 7.0% | Up to 75% | 5 – 10 Years |

| Life Insurance Co | 6.25% – 7.5% | 60% – 65% | 5 – 30 Years |

| Bridge Loan | 9.25% – 13.0% | 50% – 75% | 1 – 3 Years |

| SBA 7(a) | Prime +0% to +3% | Up to 90% | 20 – 25 Years |

| Construction | 6.5% – 10.0%+ | 60% – 80% | 2 – 3 Years |

A key takeaway: align your loan structure with your business plan. For example, using a 10-year fixed-rate loan for a property you plan to sell in two years could hurt your returns due to prepayment penalties. Conversely, floating-rate loans on long-term stabilized assets expose you to unnecessary rate risks.

How Interest Rate Trends Affect Bridge Loans and Short-Term Financing

Bridge loans are often used for interim financing, helping to bridge the gap between acquisition or construction and stabilization. As of May 2026, these loans typically carry interest rates between 9.25% and 13%, are almost always interest-only, and have terms ranging from 12 to 36 months.

Since bridge loans are tied to SOFR, they are directly impacted by Federal Reserve policy changes. Rate hikes can significantly increase carrying costs, especially when a property is still in lease-up and generating below-stabilized income. To mitigate these risks, lenders now require higher reserves for interest and operating shortfalls upfront.

The exit strategy for bridge loans is another area where interest rate trends matter. Lenders focus on whether a borrower can refinance into permanent financing – such as CMBS, life insurance company, or bank loans – when the bridge loan matures. To secure a viable exit, lenders often require a minimum 9% debt yield based on "as-stabilized" metrics.

"Bridge lenders focus on the future and look for a clear path to permanent financing." – Adam Karnes, Senior Vice President, The BSC Group

Some borrowers are now turning to five-year CMBS loans as a longer-term alternative to bridge financing. These loans offer more flexible lending standards and feature six-month open prepayment windows, reducing the risk of being locked into unfavorable terms if market conditions change. However, for niche assets like boat and RV storage, bridge financing can be harder to secure. Lenders often view these assets as less liquid, leading to higher interest rates and stricter loan-to-cost ratios compared to traditional self-storage.

These shifts in interest rates and loan structures have a direct impact on how financing affects cash flow and overall asset valuation.

sbb-itb-09b4138

How Rising and Falling Rates Affect Acquisition and Development

Shifting interest rates influence more than just financing costs – they reshape the entire financial framework of acquisitions and developments. As rates climb, lenders tighten their requirements, reducing loan amounts and increasing equity demands. Deals that once seemed feasible might no longer qualify under these stricter conditions.

How Rates Affect Loan-to-Value Ratios and Debt-Service Coverage

When lenders determine loan amounts, they focus heavily on the Debt Service Coverage Ratio (DSCR) – the ratio of a property’s net operating income (NOI) to its annual debt service. For self-storage facilities, most commercial lenders in 2026 require a DSCR between 1.20x and 1.35x. Rising interest rates increase debt service costs, often forcing lenders to reduce loan amounts to maintain the required DSCR. This means buyers must contribute more equity.

Current leverage for self-storage acquisitions typically ranges from 55% to 65% LTV, with some higher-cost options reaching 75%. For new construction, financing is generally capped at 70% to 75% loan-to-cost (LTC). Underwriting standards vary by project type, as shown below:

| Metric | Stabilized Assets | Construction / Lease-Up |

|---|---|---|

| Typical LTV / LTC | 55% – 65% | 70% – 75% |

| Min. DSCR | 1.25x – 1.30x | 1.15x (stabilized projection) |

| Debt Yield Target | 8.5% – 9% | 9%+ |

| Occupancy Requirement | 82% – 92% | 0% – 80% (bridge phase) |

This cautious approach limits the loan amount and demands higher equity contributions, making underwriting a key factor in determining whether a deal is viable.

Lenders also use a "stress-test rate" – a rate higher than the actual note rate – to ensure the property can handle potential future rate increases. This conservative underwriting often results in lower loan amounts than borrowers might anticipate, even if their NOI appears strong. Here’s an example of how lender underwriting can differ from a borrower’s projections for a $1.6 million facility:

| Item | Borrower Pro Forma | Lender Underwritten |

|---|---|---|

| Effective Gross Income | $271,800 | $247,600 |

| Operating Expenses | $92,000 | $104,000 |

| Net Operating Income (NOI) | $179,800 | $143,600 |

| Annual Debt Service | $126,000 | $126,000 |

| DSCR | 1.43 | 1.14 |

Source: HonestCasa

In this scenario, the lender’s stricter underwriting reduces the DSCR to below the required 1.20x minimum, meaning the deal might not qualify for financing without a price reduction or a larger down payment. This challenge is even more pronounced for boat and RV storage assets, which face tighter underwriting and higher rates.

"The maximum leverage a lender will extend is a ceiling, not a target. Finance to a level that leaves room for the asset’s performance to soften before the capital structure becomes the problem." – AJ Osborne, CEO, Cedar Creek Capital

Rate Sensitivity in Stabilized vs. Lease-Up Projects

The stage of a project also plays a big role in how sensitive it is to interest rate changes. Stabilized properties, which operate at 82% to 92% occupancy with steady cash flow, are less affected by rate fluctuations. These properties qualify for lower-cost permanent financing options, such as CMBS loans (6.5%–8%) or life insurance company loans (6.25%–7.5%), with lenders actively competing for these deals.

Lease-up projects, on the other hand, face more challenges. Properties with less than 85%–90% occupancy typically require bridge financing, which comes with much higher rates (9.25% to 13%) and stricter underwriting due to the longer timeline for stabilization. As of 2026, lenders are increasingly requiring higher reserves for interest and operating costs to account for potential delays in reaching stabilization.

"Self-storage bridge closes fast and prices tight because the exit market (CMBS, life co, SBA 504) is deep and the operational model is among the cleanest in CRE." – Ed Freeman, Capital Advisor, PeerSense

A practical approach for lease-up projects is the bridge-to-permanent strategy. This involves using short-term bridge loans to cover the 18–36 month lease-up period, then refinancing into long-term debt like CMBS or SBA 504 once the property stabilizes. For owner-operators, SBA 504 loans remain one of the few high-leverage options, offering up to 90% LTV at rates around 5.80% as of May 2026.

Cedar Creek Capital provides a strong example of how to manage rate risk. By January 2026, the firm had maintained a portfolio-weighted average LTV of 56.8% across 21 properties. This deliberate buffer against rate volatility helped them avoid capital calls, even during the rapid rate hikes of 2022–2024.

How Interest Rates Affect Cash Flow, Asset Valuation, and Returns

Interest rate trends shape much more than loan structures – they ripple through every layer of a storage investment, influencing cash flow, asset valuation, and returns. As borrowing costs climb, the financial dynamics of these investments shift significantly.

How Higher Rates Impact Cash Flow and Debt Service

When interest rates rise, so do debt service costs, which directly squeeze cash flow. This can even lead to negative leverage – a situation where borrowing costs surpass cap rates, making returns lower than they would be with an all-cash purchase. Between 2024 and 2026, financing costs increased by 3%–5% compared to earlier periods, leaving thinner margins for investors. Once borrowing costs exceed the asset’s cap rate, debt becomes a drag on returns. For example, if interest rates jump from 4.5% to 8.5%, a property would need an unrealistic annual NOI growth of 13% for three straight years just to maintain loan proceeds.

"The dramatic speed and extent of recent interest-rate increases is likely the single greatest self-storage financing challenge since the Great Recession of 2007-09." – Neal Gussis, Executive Director of Capital Markets, Strat Property Management Inc.

This tightening of cash flow sets the stage for shifts in property valuation, particularly through adjustments in cap rates.

Cap Rate Adjustments and Property Valuation

Rising interest rates don’t just compress cash flow – they also push cap rates higher. As borrowing becomes more expensive, investors demand higher yields to offset the increased cost of capital. In the self-storage sector, cap rates have grown by 1% to 2% in response to these rising costs.

The effect on property valuation is striking. Even with steady NOI, a higher cap rate reduces the property’s value. For instance, a facility generating $200,000 in NOI would be worth approximately $3.64 million at a 5.5% cap rate. But if the cap rate increases to 6.5%, that same NOI drops the valuation to about $3.08 million – a reduction of roughly $560,000, despite no change in operational performance. However, this valuation reset isn’t uniform across all properties.

"Cap rate expansion reflects a reassessment of risk rather than a deterioration of fundamentals." – Matthew Horne, Storage Point Capital

Facilities with stable income streams tend to hold their value better, while those with uncertain income or lower occupancy face sharper value declines. In today’s environment, the durability of income has become the key factor in determining property valuations.

Financing Strategies for Managing Interest Rate Volatility

To handle fluctuating interest rates, it’s crucial to plan your financing strategy with foresight. By building flexibility into your capital structure early on, you can better navigate unpredictable market conditions.

When and How to Refinance Storage Assets

Start planning to refinance your loans 12–18 months before they mature to secure favorable terms.

Even if the new rate is higher, refinancing can still be a smart move. For instance, if you currently have a 4% loan and rates are climbing, locking in a fixed 6% rate now might save you from facing 8% or 9% rates later on. Acting sooner can help you avoid more significant financial strain in the future.

"Refinancing a 4% interest rate loan into a 6% one might feel counterintuitive… However, bypassing an impending rate hike or locking in long-term fixed financing amid volatility can be a smart, strategic move." – Adam Karnes, Senior Vice President, The BSC Group

For properties in the lease-up phase, transitioning from bridge financing to permanent debt is often the best path once economic occupancy reaches 85% to 90%. At this stage, lenders typically consider the income stable enough to offer competitive rates, such as those available through CMBS or life insurance company loans.

If you oversee a portfolio, it’s wise to stagger loan maturities across different years. This approach prevents multiple loans from coming due within the same year, reducing your exposure to unfavorable credit cycles.

Now, let’s look at additional tools to safeguard your financing against rate increases.

Using Rate Caps and Interest-Only Periods to Manage Rate Risk

Beyond refinancing strategies, certain loan features can help shield your cash flow and asset valuations from rate volatility.

For floating-rate loans, a rate cap is a must-have. It limits how high your interest rate can rise, protecting your debt-service coverage ratio (DSCR) during rate surges. When purchasing a cap, choose a strike rate that ensures your DSCR remains stable, and align the cap’s term with your loan duration.

It’s also helpful to stress-test your floating-rate loans. Simulate a 200-basis-point rate increase to see if your DSCR drops below 1.10x. If it does, your capital structure might be carrying too much risk.

Interest-only (IO) periods are another effective tool. These periods delay principal payments, providing much-needed cash flow relief during lease-up or construction phases. For stabilized properties, CMBS loans often offer full-term IO options, while bridge loans typically include an initial three-year IO period. For new developments, combining IO payments with an interest-carry reserve can cover debt service during construction and lease-up.

Lastly, consider a rate buydown. In CMBS financing, borrowers can pay an upfront fee – usually up to 1% of the loan amount – to lower their interest rate. This can save approximately 0.25% on a five-year loan or 0.15% on a ten-year loan, improving both DSCR and borrowing capacity.

"A great deal in a bad capital structure is still a bad deal. Structure the debt for the worst plausible scenario and let the upside take care of itself." – AJ Osborne, CEO, Cedar Creek Capital

Key Takeaways for Storage Asset Owners

Interest rates influence every aspect of financing, from borrowing limits and DSCR to property valuations. Rather than attempting to predict market cycles, successful storage asset owners focus on building financing structures that can withstand fluctuations.

Here are some refined strategies for creating a solid financial foundation:

- Keep Loan-to-Value (LTV) in check: Aim for an LTV between 55% and 65%, instead of pushing to the lender’s maximum limit.

- Set a strong DSCR baseline: Target a Debt-Service Coverage Ratio (DSCR) of 1.30x or higher at origination, offering a buffer above the usual 1.20x–1.25x minimum.

"The maximum leverage a lender will extend is a ceiling, not a target. Finance to a level that leaves room for the asset’s performance to soften before the capital structure becomes the problem." – AJ Osborne, CEO, Cedar Creek Capital

Cedar Creek Capital exemplifies this disciplined approach. As of January 2026, the firm maintained a portfolio-weighted average LTV of 56.8% across 21 properties and avoided issuing a capital call for over two decades. This track record highlights the importance of maintaining financial flexibility.

To complement these principles, align your financing choices with your asset strategy:

- Use short-term bridge loans (8%–12%) for value-add and lease-up projects.

- Opt for long-term, fixed-rate loans for stabilized assets, such as CMBS loans (6.5%–8%) or life insurance loans (5.0%–6.0%).

Additionally, stress-test your floating-rate exposure by modeling a 200-basis-point rate increase. This ensures your DSCR remains above 1.10x, providing an extra layer of security.

Avoid waiting for the "perfect" rate environment. As Adam Karnes, Senior Vice President at The BSC Group, advises: "If a deal makes sense at current rates, carefully consider how to manage the risk. Additionally, if you’ve hesitated to refinance, you may find the lending landscape more appealing in the near future."

Ultimately, the goal is to create a capital structure that can weather challenges. By focusing on the asset’s performance rather than solely on financing terms, you set the stage for long-term success.

FAQs

Should I choose a fixed or floating rate for my storage loan?

Choosing between a fixed-rate or floating-rate loan hinges on your financial goals and the type of investment. Fixed-rate loans are ideal if you’re looking for predictable payments, making them a good fit for long-term investments with consistent cash flow. On the other hand, floating-rate loans offer more flexibility, which can be advantageous for short-term projects or value-add opportunities.

Although recent rate cuts have brought down floating-rate benchmarks like SOFR, it’s important to weigh the potential savings against the possibility of future rate hikes.

How do higher rates change my LTV and DSCR approval?

Higher interest rates mean higher debt service costs, which often prompt lenders to tighten their underwriting standards. To meet the required debt-service coverage ratio (DSCR) – commonly between 1.25x and 1.30x – lenders might reduce the maximum loan amount they’re willing to offer. This often leads to loan-to-value (LTV) ratios being capped at 50% to 65%, a noticeable drop from the higher ratios seen during periods of lower rates. The result? Borrowers may qualify for significantly lower loan proceeds.

When should I refinance a storage facility loan?

Refinancing a storage facility loan hinges on factors like your financial goals, the current loan status, and prevailing market conditions. A common time to refinance is when your loan is approaching maturity, helping you avoid the risk of default or the need to sell the property. Other motivations might include obtaining improved loan terms, tapping into your equity through cash-out refinancing, or securing a fixed interest rate to safeguard against rate fluctuations. Just make sure your debt service coverage ratio (DSCR) aligns with lender expectations, which usually fall between 1.25x and 1.35x.