Cap rates are a key metric for evaluating self-storage investments. They measure the relationship between a property’s income (NOI) and its market value, providing a snapshot of potential returns if purchased outright. Here’s why they matter:

- Buying Decisions: Lower cap rates (e.g., 5%) indicate stable, high-quality assets, while higher cap rates (e.g., 8%) may signal higher risk or value-add opportunities.

- Selling Impact: Cap rates directly affect property values. For instance, a $500,000 NOI property valued at $10M with a 5% cap rate would drop to $9.09M if the cap rate increases to 5.5%.

- Market Trends: In 2026, cap rates are higher than recent historic lows, influenced by borrowing costs and supply-demand shifts. Class A properties in prime areas see cap rates as low as 5.5%-6.5%, while rural Class C properties exceed 8%.

Cap rates depend on NOI, purchase price, location, asset quality, and market conditions. Small changes in cap rates can significantly impact values, making them essential for informed decision-making.

How Cap Rates Work

Let’s break down how cap rates operate, focusing on their calculation and the factors that influence them.

The Cap Rate Formula

The cap rate formula is designed to highlight a property’s performance by focusing solely on its operating income, leaving out financing considerations.

Net Operating Income (NOI) represents the income a property generates after subtracting operating expenses – like property taxes, payroll, insurance, and maintenance – but before deducting mortgage payments or financing costs. By excluding financing, cap rates provide a clear snapshot of how a property performs on its own.

To put it simply, the cap rate answers this question: If I bought this property outright with cash today, what kind of annual return would I see?

How Income and Pricing Affect Cap Rates

Cap rates are influenced by two key factors: NOI and the property’s price. Understanding how these elements interact is essential when evaluating potential investments.

When NOI changes: If the purchase price remains steady, an increase in NOI will push the cap rate higher, while a decrease in NOI – possibly due to rising operating expenses like property taxes or payroll – will lower it. For instance, take a property priced at $10 million with $500,000 in NOI. This setup yields a 5% cap rate. However, if operating expenses rise and NOI drops to $450,000, the cap rate falls to 4.5%, meaning you’re paying the same price for less income.

When price changes: On the other hand, if NOI stays constant, a higher purchase price reduces the cap rate, while a lower purchase price raises it. This is why sellers often aim to boost NOI before listing a property. Even a small increase in income can justify a higher price tag without necessarily impacting the market’s cap rate.

Here’s a quick look at how price changes affect cap rates when NOI is fixed at $500,000:

| Purchase Price | NOI | Cap Rate |

|---|---|---|

| $8,333,333 | $500,000 | 6.0% |

| $10,000,000 | $500,000 | 5.0% |

| $11,111,111 | $500,000 | 4.5% |

As the table shows, even small shifts in price can lead to noticeable differences in returns. This sensitivity becomes even more pronounced with higher NOI levels. A property’s price often reflects buyer confidence in its ability to maintain or grow income over time. The cap rate, in turn, serves as a visible indicator of that confidence.

Up next, we’ll dive into the latest trends shaping these dynamics in the self-storage market.

sbb-itb-09b4138

Current Cap Rate Trends in Self-Storage

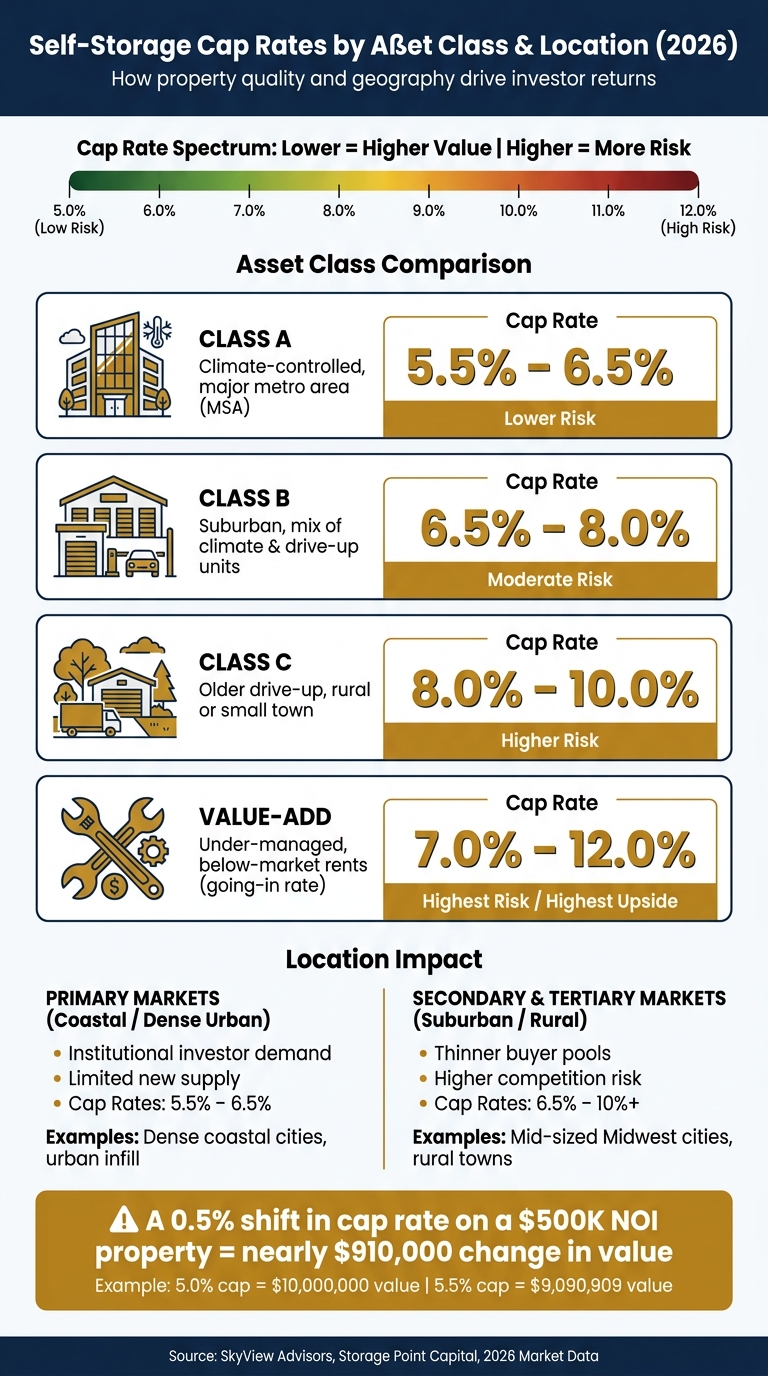

Self-Storage Cap Rates by Asset Class & Location (2026)

Cap rates in the self-storage sector have been influenced by rising borrowing costs and tighter credit conditions. While they remain higher than the historic lows seen in 2021 and 2022, investors are cautiously optimistic:

"2026 looks to be a year of continued resilience and selective growth. Fundamentals should strengthen as supply pipelines slow."

Typical Cap Rate Ranges for Self-Storage

The cap rate for a self-storage property depends largely on its quality and location. High-end Class A facilities – those multi-story, climate-controlled properties found in large metropolitan areas – tend to have the lowest cap rates. On the other hand, older properties with drive-up access in smaller towns trade at higher cap rates, reflecting the additional operational risks and lower demand.

| Asset Class | Property Description | Cap Rate Range |

|---|---|---|

| Class A | High-quality, climate-controlled, major MSA | 5.5% – 6.5% |

| Class B | Suburban, mix of climate and drive-up units | 6.5% – 8.0% |

| Class C | Older drive-up, rural or small town | 8.0% – 10.0% |

| Value-Add | Under-managed, below-market rents (going-in) | 7.0% – 12.0% |

These ranges provide a framework for investors to align their expectations with the risks and market conditions associated with different types of properties. Even small changes in cap rates can significantly impact property valuations, making it crucial to understand where an asset fits within this spectrum.

How Location and Asset Quality Affect Cap Rates

Two key factors – location and asset quality – play a major role in determining cap rates. Properties in primary markets, such as dense coastal cities or urban areas with limited new development, tend to attract institutional investors. These areas often see cap rates in the 5.5% to 6.5% range. In contrast, secondary and tertiary markets typically command higher cap rates. For example, a stabilized facility in a mid-sized Midwest city might trade at 6.5%–8.0%, while a rural Class C property could exceed 10%, reflecting thinner buyer pools, less pricing power, and heightened competition risks.

Margo Masserman of Oakside Companies explains:

"Cap rate expansion reflects a reassessment of risk rather than a deterioration of fundamentals. Higher borrowing costs, tighter credit conditions, and longer hold assumptions have materially changed how investors price cash flow."

In 2026, investors are moving away from oversupplied Sunbelt cities like Phoenix and Austin – areas that experienced heavy development between 2017 and 2019 – and focusing on coastal and infill locations where building new supply is more challenging. For those targeting tertiary markets, keeping an eye on local supply is critical. Even one new competitor in a smaller market can significantly affect occupancy rates and exit cap valuations.

Next, we’ll dive into the main factors driving these changes in self-storage cap rates.

What Drives Self-Storage Cap Rates

Cap rates don’t just shift randomly – they’re influenced by a distinct set of factors. Some stem directly from the property itself, while others are tied to broader market forces. By understanding these drivers, you can make more accurate assessments and avoid overpaying. Let’s break it down, starting with property-specific factors.

Property-Level Factors

Net Operating Income (NOI) is a key driver of cap rates. Even with a facility showing 92% physical occupancy, the actual revenue collected (economic occupancy) can lag behind by 3–8% due to concessions or unpaid rent. This shortfall directly impacts NOI.

Efficiently run facilities typically maintain an expense ratio of 35–45% of Effective Gross Income (EGI), which includes a 5–6% management fee for owner-managed properties. Smaller facilities often skip accounting for this fee when owners handle management themselves, making their cap rates appear artificially lower.

Nolen Masserman of Oakside Companies explains it well:

"The final number depends on the buyer’s confidence that a property will continue to achieve its current income level or NOI will increase. The cap rate is simply a reflection of that confidence."

A property’s lease-up status also matters. Facilities still filling vacant units are valued based on projected income (pro forma) rather than past performance. Stabilized facilities, by contrast, aim for physical occupancy levels between 85% and 92%.

Market-Level Factors

The local market plays a big role in how buyers assess risk and price properties. Below is a summary of common market-level factors and how they influence cap rates:

| Factor | Impact on Cap Rate | Reason |

|---|---|---|

| High Population Growth | Downward (Compression) | Boosts demand and NOI growth potential |

| Rising Interest Rates | Upward (Expansion) | Increases borrowing costs, narrowing the profit margin |

| New Market Supply | Upward (Expansion) | Adds competition, potentially triggering price wars |

| Institutional Capital Influx | Downward (Compression) | Higher competition among buyers drives up property prices |

| Rising Property Taxes | Upward (Expansion) | Cuts into NOI unless offset by higher rents |

Self-storage operates as a hyper-local business, meaning even small changes in the nearby market can have a big impact. For instance, a new competitor offering steep discounts within a few miles can lower occupancy and push cap rates higher. This effect is especially pronounced in smaller markets where the pool of buyers is already limited.

Specialized Asset Types

Different types of self-storage facilities require different approaches to valuation. For example, climate-controlled (CC) facilities are considered Class A assets and typically command the lowest cap rates – around 5.0% to 6.0% in primary markets by 2026. These units rent for a 30% to 50% premium over standard drive-up units and now make up over 40% of new national supply.

However, CC facilities come with higher operating costs. Utilities alone can eat up 3% to 8% of EGI. When analyzing mixed-use facilities, it’s essential to separate climate-controlled and non-climate-controlled units, as they have distinct cost structures and rental dynamics.

On the other end of the spectrum, older drive-up facilities in tertiary markets trade at higher cap rates – often 7.0% to 7.5% or more. While these properties carry more risk, they also offer opportunities for repositioning. Upgrading a Class C property to Class A or B – by adding climate control, enhancing curb appeal, or modernizing revenue management – can reduce the exit cap rate and increase resale value.

How to Value a Self-Storage Investment

Once you grasp the factors influencing cap rates, the next step is figuring out how to value a property. This process builds on the relationship between income, pricing, and cap rates. The method you use will depend on whether the property is fully operational, in transition, or undergoing improvements. Accurate valuation is crucial, as Nolen Masserman at Oakside Companies explains: "A swing of just half a percentage point can add or subtract millions of dollars."

Trailing, Pro Forma, and Stabilized Cap Rates

Each type of cap rate reflects a different income scenario, and knowing when to use the right one is key.

| Cap Rate Type | Based On | Best Used For |

|---|---|---|

| Trailing | Actual NOI from the past 12 months | Established, fully operational facilities |

| Pro Forma | Projected NOI based on future improvements | Properties expecting occupancy or rent growth |

| Stabilized | Normalized NOI for steady-state operation | New developments or transitioning facilities |

The trailing cap rate focuses on historical performance, showing what the property has earned in the past year. However, it might not reflect recent changes, like a major tenant leaving or a recent expansion. On the other hand, the pro forma cap rate is forward-looking, based on projected income. While this can highlight potential, it often includes optimistic assumptions about rent or occupancy increases, especially in competitive markets with rising supply. Lastly, the stabilized cap rate accounts for normalized income once the property reaches full operation, making it a better fit for facilities still ramping up. Solely relying on trailing income for such properties could lead to undervaluation; stabilized NOI provides a clearer picture of future earnings.

To ground your valuation, you’ll need to turn to real-world market data.

Using Comparable Sales and Market Data

When comparing properties, consistency is critical. For example, a high-end, climate-controlled facility in a busy suburb isn’t directly comparable to an older drive-up facility in a rural area – even if they’re in the same state. Use market-derived cap rates from similar self-storage sales to evaluate whether a deal is fairly priced. This data helps refine your valuation, but only when applied thoughtfully to the specific property in question. As Margo Masserman points out:

"Context matters. A strong facility in a secondary market may outperform a weak one in a primary market, regardless of what the stated cap rate suggests."

Be sure to verify the reported NOI. Smaller facilities, especially those run by "mom-and-pop" operators, may underreport expenses like management fees if the owners self-manage. This can make the cap rate appear higher than it actually is. While cap rates provide a solid starting point, they work best when combined with discounted cash-flow analysis and sensitivity testing. These tools help account for financing costs and future capital expenses, giving you a more complete picture.

How Cap Rates Affect Property Value

Cap rates and property values share an inverse relationship – when cap rates rise, property values drop. Conversely, when cap rates fall, property values climb.

How Sensitive Property Value Is to Cap Rate Shifts

For self-storage investors, grasping how even minor cap rate changes can influence property values is key to planning both purchases and exits. Property value is determined by dividing the net operating income (NOI) by the cap rate. This means even a slight adjustment in the cap rate can lead to a noticeable shift in value. For example, a self-storage property with a $500,000 NOI is valued at $10,000,000 at a 5.0% cap rate. If the cap rate rises to 5.5%, the value drops to roughly $9,090,909 – a decrease of nearly $910,000:

| NOI | Cap Rate | Property Value | Value Change vs. 5.0% |

|---|---|---|---|

| $500,000 | 5.0% | $10,000,000 | – |

| $500,000 | 5.5% | $9,090,909 | −$909,091 |

| $500,000 | 6.0% | $8,333,333 | −$1,666,667 |

"The cap rate is simply a reflection of [the] confidence a buyer has that a self-storage property will continue to perform well and grow NOI over time." – Nolen Masserman, Oakside

This highlights the importance of ensuring that NOI projections are accurate. Any miscalculation can significantly alter a property’s valuation, making it critical to understand these dynamics when planning your investment’s exit strategy.

Planning Your Exit Around Cap Rates

Timing the sale of your property to align with favorable cap rate conditions is just as important as negotiating the right purchase price. For instance, in late 2025 and early 2026, the market saw a shift where sellers’ price expectations began to better align with current market conditions. This encouraged buyers to scrutinize properties more closely, focusing on their ability to maintain or grow NOI.

Sellers can enhance their outcomes by optimizing operations before listing. Steps like improving revenue management and cutting unnecessary costs can lead to a higher valuation. Collaborating with advisors to identify active buyers and effectively showcase the property’s stability can also shorten the time on the market and secure a stronger sale price.

Ways to Improve Cap Rates and Returns

Improving your cap rate boils down to enhancing the property’s income and reliability, which makes it more appealing to buyers and increases its overall value. Below, we’ll explore operational changes and physical upgrades that can help achieve these goals.

Improving Day-to-Day Operations

A great way to boost Net Operating Income (NOI) is through smarter revenue strategies. For instance, you can adjust street rates based on occupancy levels: increase rates when physical occupancy is above 90% and offer promotions when it drops below 85%. This tactic ensures revenue stays optimized, especially during the busy moving season from May to September.

Additional revenue streams, like tenant insurance, retail sales, and truck rental commissions, also contribute significantly to NOI. Many facilities now require tenants to carry insurance, providing a steady income with minimal overhead. On top of that, reducing payroll expenses by incorporating remote management systems and automated kiosks can further improve profitability.

Well-managed facilities often aim for an expense ratio between 35% and 45% of Effective Gross Income (EGI). Margo Masserman, VP of Oakside Companies, emphasizes:

"Improving operational efficiency can substantially enhance your sales price."

While operational changes directly impact NOI, property upgrades can significantly change how buyers perceive an asset, potentially lowering its cap rate.

Property-Level Upgrades and Repositioning

Physical enhancements can make a big difference in how buyers evaluate a property, often leading to lower cap rates. For example, retrofitting older drive-up facilities with HVAC systems can increase their appeal, as climate-controlled units now make up over 40% of new supply nationwide. This upgrade can turn outdated facilities into high-demand assets that attract more buyers.

If your property has unused land, consider building a multi-story, climate-controlled structure. This can elevate a Class C property to Class A status, drawing interest from institutional buyers who typically have access to cheaper capital and are willing to pay more per square foot for premium assets:

"By improving the quality of the asset, this opens up to a buyer pool with more access to capital and likely lower cost of capital, who will pay more per SF for higher quality of the asset."

Even smaller renovations, like replacing roofs, repainting exteriors, or reconfiguring unit layouts, can reduce the property’s risk profile. The goal is to make the asset’s income stream appear more stable and reliable, which compresses cap rates and boosts its market value. These upgrades not only strengthen current cash flows but also enhance the property’s appeal when it’s time to sell.

Key Takeaways for Self-Storage Investors

Here’s what stands out for investors based on the analysis:

Cap rates are powerful tools – when you understand the context.

"Ultimately, it’s the confidence a buyer has that a self-storage property will continue to perform well and grow NOI over time that determines asset price. The cap rate is simply a reflection of that confidence."

Even a small shift, like a half-point change in cap rates, can significantly impact property values. For this reason, both buyers and sellers must carefully evaluate every assumption tied to the NOI.

Cap rates depend on market and asset quality. Urban Class A facilities often see rates as low as 5%, while rural Class C properties might trade above 8%. Factors such as location, asset condition, and local market trends all influence what buyers are willing to accept.

While cap rates offer a great starting point, they’re just one piece of the puzzle. Pair them with cash-flow and sensitivity analyses to get a more complete picture – one that considers potential operational improvements, cost savings, and repositioning opportunities over time.

FAQs

What’s a “good” cap rate for self-storage today?

A "good" cap rate for self-storage properties generally ranges from 5.0% to 8%+. Properties in prime locations with steady performance often hover around 5.5%, reflecting lower risk. On the other hand, cap rates closer to 8.0% might signal higher risk or less appealing assets. These figures serve as useful guidelines for investors to weigh potential returns against associated risks when considering self-storage investments.

How do I verify NOI before trusting a cap rate?

Before relying on a cap rate, it’s crucial to ensure the Net Operating Income (NOI) is accurate and reflects realistic numbers. Start by reviewing income statements to confirm that all revenue sources are included. At the same time, make sure expenses – like real estate taxes – are adjusted to reflect current market levels.

It’s also helpful to compare the trailing NOI (based on past income) with the forecasted or stabilized NOI (projected future income). This comparison can reveal inconsistencies and give you a clearer picture of how reliable the cap rate might be.

When should I use trailing vs. pro forma vs. stabilized cap rates?

When deciding which cap rate to use, it all comes down to your analysis goals:

- Trailing cap rates focus on recent, actual income and are best for evaluating current performance.

- Pro forma cap rates project future income, making them ideal for analyzing potential returns after improvements or changes.

- Stabilized cap rates represent steady, long-term income once a property reaches full occupancy or completes upgrades.

In short, use trailing cap rates for understanding current trends, pro forma for forecasting, and stabilized for assessing long-term value.