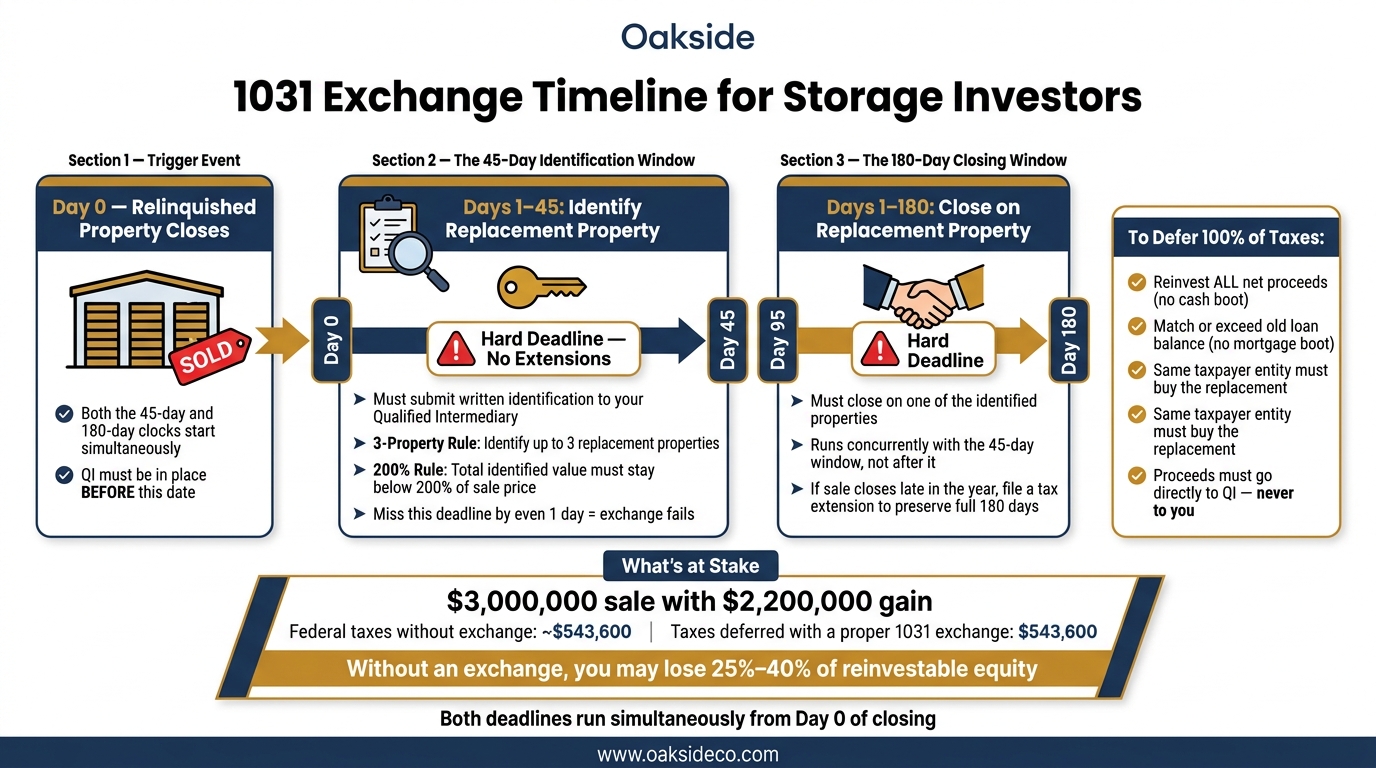

A 1031 exchange can keep a large part of your sale equity from going to taxes at closing. If you sell a self-storage, boat, or RV facility, you may cut your reinvestable cash by 25% to 40% if you do not exchange.

Here’s the short version:

- I can defer capital gains tax and depreciation recapture by moving sale proceeds into other qualifying U.S. investment real estate.

- I must follow two hard deadlines: 45 days to identify replacement property and 180 days to close.

- I cannot touch the sale proceeds. A Qualified Intermediary has to hold them.

- To defer the full tax bill, I need to replace all net equity and usually match or exceed the debt paid off on the sale.

- If I take cash out or reduce debt without adding cash, I may create boot, which can be taxable.

- The property types do not have to match. A storage site can be exchanged for apartments, retail, land, or a DST if the property is held for investment or business use.

- The same taxpayer that sells must buy the replacement property.

One example shows why this matters: on a $3,000,000 sale with a $2,200,000 gain, federal taxes alone could reach about $543,600. A properly set-up exchange defers that bill, so more money stays available for the next deal.

If I want the exchange to work, I need to plan before listing, line up the QI early, and have backup replacement options ready.

What a 1031 Exchange Is and Why It Matters for Storage Owners

A 1031 exchange lets you sell investment real estate and roll the proceeds into another qualifying property without paying capital gains tax or depreciation recapture at closing. That doesn’t mean the tax disappears. It’s deferred. Your old basis carries over into the new property, and the deferred tax comes due if you later sell in a taxable sale.

For storage owners, that can make a big difference. More money stays in the deal, which gives you more room to move.

The Core Rule: Like-Kind Real Property Held for Investment or Business Use

Here’s the main rule: both the property you sell and the property you buy must be U.S. real estate used in a trade or business or held for investment.

This is where people often get tripped up. “Like-kind” does not mean the two properties have to match.

A self-storage facility can be exchanged for:

- An apartment complex

- A retail center

- Raw land

- A Delaware Statutory Trust (DST)

So yes, the asset type can change. What matters is investment intent.

Self-storage, boat storage, and RV storage facilities all meet this standard. A primary residence does not. A vacation home that you use personally does not either.

How Tax Deferral Affects Your Reinvestment Capacity

Tax deferral matters for one simple reason: it leaves more equity in your hands for the next purchase. And that can shape your next move in a big way.

Maybe you want to trade up into a larger facility. Maybe you want to combine a few smaller sites into one property. Or maybe you’re done with daily management and want to shift into a passive DST.

Some investors keep doing exchanges over and over, pushing the tax bill further down the road until death, when heirs may receive a stepped-up basis. Once a property meets the basic 1031 rules, the next thing to watch is timing and who controls the sale proceeds.

sbb-itb-09b4138

Eligibility, Exchange Rules, and the Deadlines That Control the Deal

1031 Exchange Timeline for Storage Investors: Key Steps & Deadlines

Before you list, nail down two things: whether the property qualifies and whether you can meet the deadlines. Once the property clears the eligibility test, the whole exchange comes down to timing and keeping the sale proceeds out of your hands.

What Counts as Relinquished and Replacement Property

Both the property you sell and the property you buy must be U.S. real estate held for investment or business use. Personal property no longer qualifies.

The same taxpayer that sells must also buy the replacement property. So if an LLC sells the property, that same LLC has to be the buyer on the replacement side.

| Property Type | Qualifies | Does Not Qualify |

|---|---|---|

| Residential | Single-family rentals, multifamily apartments | Primary residences, personal-use vacation homes |

| Commercial | Self-storage, retail centers, office buildings | Inventory held for resale |

| Land / Other | Raw land, farmland, parking lots, mineral rights | Partnership interests, stocks, bonds |

| Passive | Delaware Statutory Trusts (DSTs), Tenancy-in-Common (TIC) | REIT shares |

Once eligibility is clear, the next issue is timing. And this is where deals can go sideways fast.

The 45-Day Identification Rule and 180-Day Closing Rule

Both clocks start on Day 0 – the day your relinquished property closes. You get 45 days to identify replacement properties in writing to your Qualified Intermediary, and 180 days total to close on one of them. These windows run at the same time, not one after the other.

Miss either deadline by even one day and the exchange fails. The QI sends back the funds, and the gain becomes taxable. That wipes out the reinvestment capital the exchange is meant to keep in play.

If your sale closes late in the year, file an extension so you can keep the full 180-day window.

The 3-Property Rule lets you identify up to three replacement properties. That gives you a fallback option if your first pick falls apart during due diligence.

Those dates matter, but only if the proceeds never touch your account.

Why a Qualified Intermediary Must Hold the Sale Proceeds

A QI keeps the exchange intact by holding the proceeds until closing. If you receive the money, the IRS treats the exchange as failed.

A Qualified Intermediary (QI) takes the sale proceeds, holds them in a segregated account, and releases them at closing.

Your CPA, attorney, or recent agent can’t act as your QI. For a standard forward exchange, QI fees usually run from $750 to $1,500.

The QI must be in place, and the exchange agreement must be signed, before your storage facility closes – not after.

How Storage Investors Structure a Full-Deferral Exchange

With eligibility and deadlines out of the way, the next step is protecting every dollar of deferred gain. For full deferral, investors need to replace all net proceeds and all debt tied to the sale.

How Boot Is Created and How to Reduce It

Boot is any value received in the exchange that is not like-kind real estate. Cash boot means sale proceeds were not fully reinvested. Mortgage boot happens when the debt on the replacement property is lower than the debt paid off when the old property sold. Either one can trigger taxable gain.

To avoid mortgage boot, the new loan should match or exceed the old loan balance. If it doesn’t, the gap can be covered with extra cash brought in from outside the exchange.

There’s another trap here. Exchange funds can only go toward buying the replacement property. They can’t be used for repairs after closing unless the exchange was set up as an improvement exchange from the start.

Once boot is under control, the next move is picking a replacement asset that fits the portfolio. This selection is a critical part of any self-storage investment strategy.

Replacement Property Options for Self-Storage, Boat, and RV Portfolios

Storage investors can shift equity into other like-kind real estate, including single-tenant industrial, multifamily, or land.

One common play is to sell older Class C facilities and roll that equity into a larger Class B asset (where self-storage cap rates are often lower) in a stronger submarket. For investors who want a more hands-off route, Delaware Statutory Trusts (DSTs) offer fractional ownership. DST sponsors often charge upfront fees ranging from 10% to 15% of invested capital.

The 200% Rule gives investors room to name as many replacement properties as they want, as long as the total identified value stays below 200% of the sale price.

Even a solid replacement property won’t save the exchange if the paperwork or ownership setup is off.

Mistakes That Make the Exchange Taxable

The 45-day identification window is absolute, so the search for replacement property should start before closing. Another common problem is breaking the same taxpayer rule. The entity that sells the relinquished property must also buy the replacement property.

And one mistake can kill the whole deal fast: if the investor receives or controls the sale proceeds at any point, the exchange is disqualified.

Planning Your Exchange With the Right Advisory Support

Once boot, deadlines, and eligibility are clear, success comes down to preparation. The listing, debt plan, identification, and closing all need to line up before the sale moves forward.

When to Bring Oakside Co Into the Process

Bring in Oakside Co before you list the property, ideally a few months in advance. Oakside works with self-storage and boat and RV owners to model tax exposure, set replacement criteria around debt replacement and boot avoidance, and coordinate the qualified intermediary, lender, and tax advisor through closing.

This kind of support matters most at each step of the exchange timeline:

| Exchange Phase | Timing | Advisory Focus |

|---|---|---|

| Pre-Listing | Months before sale | Tax modeling, disposition strategy, QI selection |

| Pre-Closing | Before the contract is signed | 1031 cooperation language, QI engagement |

| Day 0–45 | Identification window | Data-driven analysis of replacement self-storage, boat, or RV assets |

| Day 45–180 | Closing window | Transaction management, financing, closing execution |

| Post-Closing | Tax filing year | IRS Form 8824 filing |

Key Points to Remember Before You Start

A 1031 exchange defers tax. It does not erase it. In most cases, the replacement property value should match or exceed both the equity and debt being replaced. Proceeds need to go to the qualified intermediary, the 45-day deadline must be met, and replacement options should be lined up before listing.

FAQs

Can I do a 1031 exchange into multiple properties?

Yes. A 1031 exchange can be used to buy more than one replacement property, not just a single asset.

There’s a catch, though: timing and IRS rules matter a lot.

You need to:

- identify the replacement properties within 45 days of selling your relinquished property

- close on them within 180 days

- follow one of the IRS identification rules: the 3-property rule, the 200% rule, or the 95% rule

Think of it like giving yourself a short runway. You can split one sale into several purchases, but you still have to stay inside the IRS time limits and identification rules.

What happens if one identified property falls through?

If one of your identified replacement properties falls through, you can still complete the exchange – but ONLY if you named other options by the 45-day deadline.

After Day 45, you can’t add new properties. That’s why it makes sense to identify more than one option from the start, such as under the three-property rule.

As Nolen Masserman, Managing Director at Oakside, notes, starting your search before the sale of your current facility is final can help you avoid feeling rushed.

How long should I hold a replacement property?

There is no required minimum hold period for a replacement property under Section 1031.

That said, the IRS expects you to buy it with a clear intent to hold it for investment or business use, not flip it right away. If you sell after only a short time, that can lead the IRS to question what your intent was from the start.