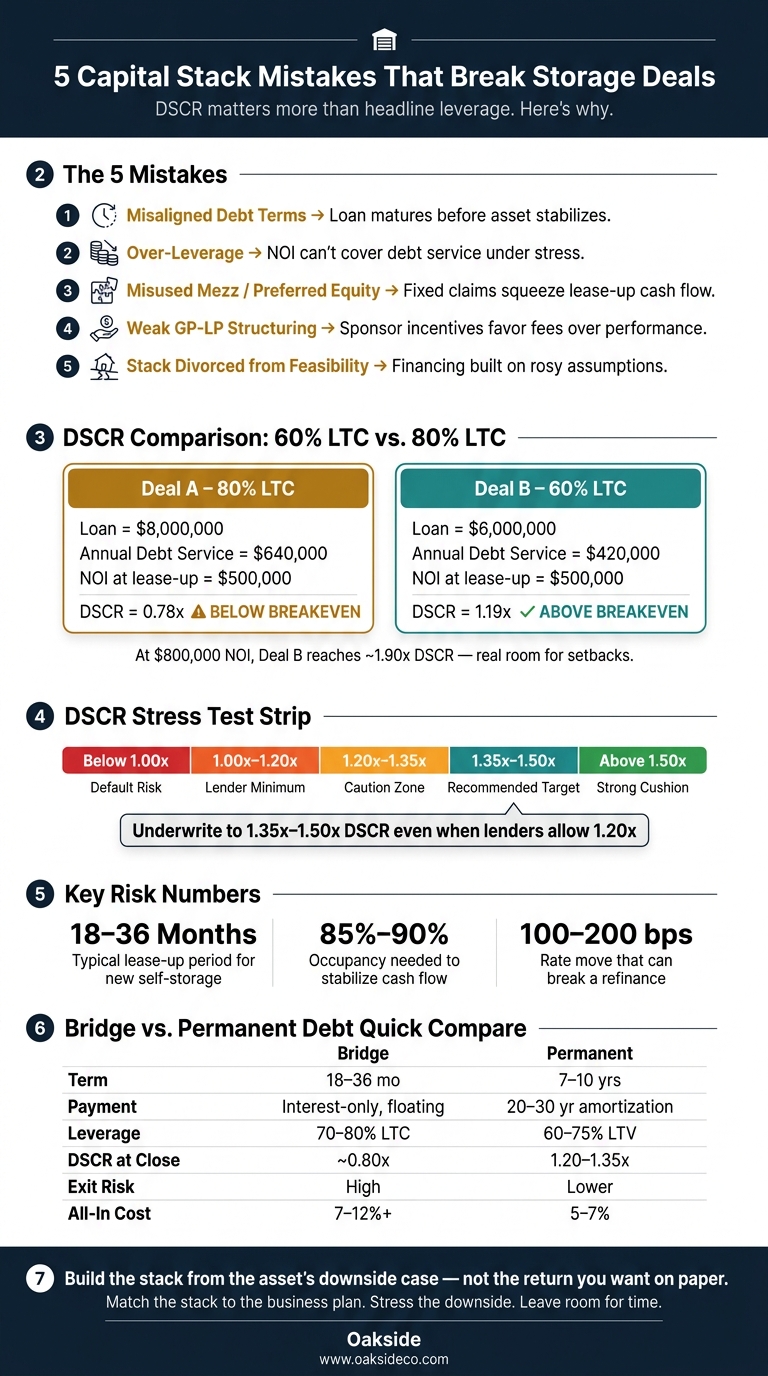

Most storage deals don’t break because of one bad assumption. They break because the capital stack leaves no room for delay, lower NOI, or higher debt cost.

If I were sizing a storage or boat/RV deal today, I’d focus on five pressure points first:

- Debt terms that expire too soon for lease-up or value-add work

- Leverage that looks fine on LTV but fails on DSCR

- Mezz debt or preferred equity added too early

- GP-LP terms that pay the sponsor before performance is proven

- A stack built to hit target returns instead of the asset’s downside case

The article’s core point is simple: in these deals, DSCR matters more than headline leverage. A project can appraise well and still not support more debt. That is even more true when lease-up takes 18 to 36 months, when occupancy needs to reach about 85% to 90%, or when seasonality squeezes cash flow.

A few numbers make the risk plain:

- Many sponsors underwrite to 1.35x to 1.50x DSCR, even when lenders allow 1.20x

- A 10% to 20% NOI miss or 100 to 200 basis point rate move can make a refinance much harder

- Moving from 60% LTC to 80% LTC can strip away most of the margin for error during lease-up

My takeaway: I’d build the stack from the property’s weaker-case cash flow, not from the return I want on paper. That usually means slower lease-up assumptions, more reserves, cleaner equity terms, and debt that can last long enough for the plan to work.

Capital Stack Mistakes in Storage Deals: DSCR & Leverage at a Glance

Quick Comparison

| Mistake | What goes wrong | What I’d check first |

|---|---|---|

| Misaligned debt terms | Loan matures before the asset stabilizes | Term length, IO period, extension options |

| Over-leverage | NOI cannot support debt service under stress | DSCR under lower NOI and higher rates |

| Misused mezz/pref | Added fixed claims squeeze cash flow | Combined payment burden and control rights |

| Weak GP-LP structuring | Incentives favor fees or early exit | Pref, promote hurdles, GP co-invest |

| Stack divorced from feasibility | Financing is built on rosy assumptions | Downside NOI, reserves, local demand |

If you want the short version: match the stack to the business plan, stress the downside, and leave room for time.

Why Capital Structure Matters More in Storage and Boat/RV Deals

Storage and boat/RV assets are tougher to finance because most tenants pay month to month. That makes cash flow less steady. And when cash flow moves around, the capital stack has to match timing, not just leverage.

That issue hits hardest during lease-up. It’s the weakest stretch of the deal, and it can put pressure on the whole stack fast.

New self-storage facilities often need 18–36 months to reach 85%–90% economic occupancy, so debt has to leave room for a long ramp-up. If a deal doesn’t have enough interest reserves, workable covenants, and extension options, a sponsor can burn through cash before the property settles into normal performance.

Boat/RV storage brings a different problem: seasonality. Annual numbers can look fine while low-season DSCR gets squeezed. That matters more than it may seem. Thin operating reserves can push owners to cut back on marketing or maintenance at the wrong time, and that can hurt performance later. So even stabilized deals need more cushion than a lender’s bare-minimum test.

These properties also need a healthy DSCR buffer because taxes, insurance, and discounting can eat into margin in a hurry. A common underwriting target is 1.35x–1.50x DSCR, even when the loan minimum is 1.20x.

Expansion deals add another layer of risk. You’re not just running the current property. You’re also taking on construction and lease-up at the same time. If the financing isn’t split with dedicated reserves, draw schedules, and lease-up or construction milestones, cost overruns can hit the entire stack all at once. Put simply, the stack should fit the phase of the project, not force the project to fit the stack.

These risks usually show up in debt terms first.

1. Misaligned Debt Terms With the Business Plan

The biggest mistake is taking on debt that comes due before the project has time to settle. When that happens, leverage usually becomes the next headache.

For ground-up projects and heavy value-add deals, bridge debt only makes sense when a refinance or sale before maturity is a realistic path. If that path is shaky, the loan term can work against the deal fast. That’s why lease-up debt needs payment relief, not just more time. In many cases, the deal needs interest-only payments or some form of amortization relief until occupancy can carry the debt load.

Amortization matters just as much as maturity. A short-term loan can push an exit sooner than the business plan allows, forcing the sponsor to sell or refinance before the asset reaches full value.

A good gut check is to stress test the capital stack for:

- a 6- to 12-month lease-up delay

- a 10% to 20% NOI shortfall

When debt terms are too tight, coverage is usually the next thing to crack.

2. Over-Leveraging and Ignoring DSCR Cushion

Even when the loan term lines up with the business plan, too much leverage can wipe out your margin for error. DSCR tells you whether NOI can cover debt service. Push leverage too far, and that cushion gets thin fast. That’s when default risk starts to climb, especially during ramp-up.

A practical target is 1.35x–1.50x DSCR, even if the lender only asks for 1.20x. Why aim higher? Because it doesn’t take much to knock a deal off balance. A 10%–15% drop in NOI from slower lease-up, seasonal demand swings, or creeping tax and insurance costs can drag coverage down to the point where operations no longer cover debt service.

You can see it clearly in early lease-up. Take two ground-up storage developments, each with $10,000,000 in total development cost. Deal A uses 80% LTC and carries $640,000 in annual debt service. Deal B uses 60% LTC and carries $420,000. At $500,000 NOI, Deal A sits at 0.78x – below breakeven. Deal B comes in at 1.19x, which is still above breakeven. At $800,000 NOI, Deal B gets to about 1.90x, giving the project real room to handle setbacks. A lighter capital stack also helps keep refinance options open.

Refinance risk makes this even tougher. Loans that were originated at 1.30x–1.45x DSCR during the 2020–2022 low-rate period are now refinancing closer to 1.05x–1.00x. Higher rates and softer NOI can shrink refinance proceeds, change loan pricing, or stop the refinance altogether.

The fix isn’t adding more equity just to feel safe. It’s sizing debt with discipline. Underwrite to a stressed DSCR using:

- 10%–20% below pro forma NOI

- 100–200 bps above current rates

If DSCR drops below 1.25x under that stress case, the loan is too large.

3. Misusing Mezzanine Debt and Preferred Equity

Once senior debt is sized the right way, the next mistake is piling on extra capital that seems flexible but can weaken the deal. In lease-up and value-add storage deals, mezzanine debt and preferred equity are not the same thing. If you treat them like interchangeable funding sources, you can skew both cost and control.

Mezzanine debt is subordinated debt secured by a pledge of LLC interests. Preferred equity is equity with priority distributions, not a loan.

That difference matters when things go sideways. If a deal underperforms, a mezz lender can foreclose on pledged equity and take control. A preferred investor usually has to rely on contract rights in the deal documents, and that can make a workout slower and messier.

The bigger issue is the payment stack. When you layer on mezz payments or preferred distributions before the asset has stabilized, coverage gets squeezed. In a value-add or lease-up storage deal, occupancy is still ramping and NOI is still finding its level. So the cushion can get thin FAST. A slower lease-up, one surprise repair bill, or even one soft quarter can put pressure on the whole structure. At that point, GP-LP terms matter just as much as the stated price of the capital.

| Mezzanine Debt | Preferred Equity | |

|---|---|---|

| Legal form | Debt | Equity |

| Security | Pledge of LLC interests | Contractual rights in the entity |

| Default remedy | Foreclosure on pledged interests | Contractual remedies, not foreclosure |

| Typical pricing | 12%–18% | 13%–20% |

The best setup lines up each capital layer with the asset’s risk, timing, and control needs. Mezzanine debt also brings covenants like DSCR floors and loan-to-value tests, which can trigger a technical default even when payments are current. That can be a serious issue in self-storage and boat/RV deals, where seasonal demand swings may push NOI below covenant thresholds for a period. Preferred equity avoids that exact problem, but it can still pressure cash flow if the preferred return accrues faster than the property can produce income.

The practical test is simple: underwrite to combined debt service, not just senior debt service. If the project can’t carry the senior loan, mezzanine payments, and preferred distributions through lease-up with a real cushion, the structure is too aggressive for the business plan, no matter what the headline leverage ratio says. Once the debt and preferred layers are set, the next issue is how common equity gets split and who controls it.

4. Undisciplined GP-LP Equity Structuring

Even if the debt stack is sized the right way, the common equity split between the GP (sponsor) and LP (investors) can still chip away at the deal. A sponsor who gets paid well no matter how the asset performs isn’t lined up with investor outcomes. In storage and boat/RV deals, that gap can lead to bad calls on sales, refinances, or leverage at the exact moment the property needs patience.

The first thing to check is simple: do fees eat into returns before the property stabilizes? Front-loaded fees, like acquisition, asset management, and disposition fees, can drag down LP returns before the promote even starts, especially during lease-up.

Low hurdles and aggressive waterfalls create another problem. They push sponsors to chase speed instead of staying focused on long-term value. If a GP’s carried interest kicks in at a low net IRR to LPs, the sponsor has a reason to push for a fast sale or refinance instead of waiting for the asset to mature. And the waterfall matters just as much as the hurdle. An aggressive GP catch-up can trim LP upside and nudge the sponsor toward earlier exits or more leverage.

A more disciplined setup usually looks cleaner:

- LP capital gets returned first

- A clear preferred return comes next

- Profits are split in defined tiers

- Promotes start at higher, risk-adjusted targets, such as a 13% to 15% net IRR

That kind of structure pays the GP for holding up performance over time, not just for moving fast.

GP co-investment is the last big signal. The sponsor should have meaningful personal capital in the deal, not just fee income on the line. When the GP puts in money on the same terms as LP equity, it tends to change how they think about leverage, lease-up timing, and when to exit. That matters in storage and boat/RV assets, where seasonal demand and operating swings can move NOI in a material way from one quarter to the next.

Even strong GP-LP terms can fall apart if the stack ignores the asset’s actual lease-up and operating risk. Once equity incentives are lined up, the next step is to check whether the full capital stack still fits the business plan.

5. Treating the Capital Stack Separately From Asset Feasibility

A common mistake is building the capital stack around a target IRR instead of the property’s actual lease-up and cash flow. It usually starts when the stack gets underwritten before the asset does. That’s backwards.

Start with what the property is likely to do in plain terms: its lease-up pace, the rents it can get, the expense load it will carry, and where it stands in the local market. Then build debt, equity, and waterfalls around that picture.

When people skip that step, the problem shows up fast in coverage and timing. Debt gets sized off rosy NOI, and fixed payments may hit before the asset is stable. In storage, even small forecast misses can turn into financing issues. Boat/RV assets are even more exposed because they often take longer to stabilize, so lenders may ask for 60% to 65% LTV and 1.20x to 1.25x DSCR at stabilization. Put simply, the stack should be sized from the asset’s downside case, not the sponsor’s upside case.

The fix isn’t fancy. Build the stack from the bottom up.

- Start with a conservative NOI forecast

- Stress-test it for slower lease-up and higher expenses

- Size debt to keep a real DSCR cushion, often 1.20x to 1.35x for self-storage

If that conservative case can’t support the target IRR, change the structure instead of massaging the assumptions. That may mean less leverage, more equity, or capital that’s willing to wait longer.

That same idea also shapes whether a deal calls for bridge debt or permanent debt.

sbb-itb-09b4138

Bridge Debt vs. Permanent Debt: A Quick Comparison

Bridge debt fits lease-up. Permanent debt fits stabilization.

In storage and boat/RV deals, the main issue is simple: does the loan still hold up if stabilization takes longer than planned? That’s where things can get tight.

| Factor | Bridge Debt | Permanent Debt |

|---|---|---|

| Term Length | 18–36 months, often with one or two 6–12 month extension options | 7–10 years or longer |

| Payment Structure | Interest-only for the full term; floating rate, often SOFR + spread | 20–30 year amortization, sometimes after an initial IO period of 2–5 years |

| Closing DSCR | Lower – some lenders fund with no minimum DSCR or around 0.80x | Higher – typically around 1.20x–1.35x on in-place or trailing NOI |

| Exit Risk | High – the balloon arrives before NOI may be fully stabilized | Lower over the hold period, though maturity still creates some refinance risk |

| Leverage Range | 70%–80% LTC / 65%–80% LTV | 60%–75% of stabilized value |

| All-In Cost | Roughly 7%–12%+ all-in, plus 1%–3% in origination fees | Roughly 5%–7% all-in, generally with lower fees |

Bridge debt gives you room to lease up and execute the plan. Permanent debt gives you a longer runway and more predictable payments. One leans toward flexibility; the other leans toward stability.

The catch with bridge debt is the exit. If NOI hasn’t reached the level needed for a refinance by the time the balloon hits, the deal can turn into a DSCR issue fast. That risk gets sharper when leverage is high.

Use the table as a quick stress test. Look at what happens if lease-up slips, rates stay high, or cash flow comes in below plan before maturity.

DSCR Example: How Over-Leverage Shrinks Margin for Error

A simple stress test shows how fast DSCR can tighten. Start with a hypothetical stabilized self-storage asset with a total project cost of $8,500,000. That includes a purchase price of about $8,000,000 plus roughly $500,000 in closing costs, reserves, and light capex. Assume a base NOI of $900,000, a 25-year amortization schedule, and a fixed rate of 6.00%.

At 65% loan-to-cost (LTC), the loan amount is $5,525,000. Annual debt service comes in at about $440,000, which puts DSCR at roughly 2.05x. On paper, that leaves a decent buffer.

Now turn the leverage up. At 80% LTC, the loan rises to $6,800,000. Annual debt service increases to around $550,000, and DSCR falls to about 1.64x. If the rate moves to 7.5%, debt service jumps again to roughly $650,000, which pulls DSCR down to about 1.38x. That is barely above a 1.35x threshold, with almost no room left for mistakes.

And that’s where the risk gets very real. A 5-point occupancy miss – for example, physical occupancy slipping from 90% to 85% – could reduce NOI from $900,000 to about $840,000. DSCR would then fall to roughly 1.29x. A 10-point miss could cut NOI to $780,000 and bring DSCR down to about 1.20x.

Expenses can squeeze things even more. If costs come in 10%–15% above budget – because of property tax reassessments, insurance hikes, or payroll pressure – expenses could move from 37% of revenue to roughly 41%–43%. That would trim about $70,000–$110,000 from annual NOI and push DSCR from 1.38x to around 1.25x or lower, even before any drop in revenue.

That’s the point of DSCR. It shows how much the deal can bend before it starts to crack. When leverage gets too high, the cushion gets thin fast, and each part of the capital stack has less room to absorb bad news.

The Capital Stack Layers: Priority, Returns, and Control

Building on the mezzanine-vs.-preferred equity distinction above, the main point here is priority and control. Put simply: who gets paid first, who can step in when things go sideways, and who gets the upside if the deal goes well.

| Layer | Payment Priority | Security Position | Typical Return | Control Rights |

|---|---|---|---|---|

| Senior Debt | First | First-position mortgage or deed of trust, often with assignment of leases and rents | Lowest | Covenants, cash sweeps, foreclosure rights on default |

| Mezzanine Debt | After senior debt, before equity | Pledge of equity interests in the property-owning entity | Low-mid | Step-in rights and UCC foreclosure rights on the ownership entity, limited by senior lender rights |

| Preferred Equity | Ahead of common equity | Contractual priority in the operating agreement; no direct lien | Fixed preferred return | Approval rights over major decisions such as sales, refinances, budgets, and GP replacement |

| Common Equity (GP/LP Split) | Residual | Ownership interest only | Highest upside | GP handles day-to-day control; LPs usually have limited major decision rights |

The sharpest difference between mezzanine debt and preferred equity comes down to rights and remedies. Mezzanine debt is still a loan, secured by a pledge of equity interests. That means the lender may be able to take control of the ownership entity through UCC foreclosure, often in as little as 30 to 60 days.

Preferred equity works differently. It has no direct lien, but it may still give the investor teeth. For example, the deal documents can allow sponsor replacement or even a forced sale if certain performance marks are missed. That may sound similar on the surface, but it isn’t. One tool is based on a secured loan structure. The other comes from contract rights in the operating agreement. That difference affects who moves first, how the process unfolds, and what it may cost.

There’s also a plain economic point here. Every layer above common equity adds a fixed claim that must be paid before the sponsor sees any upside. In storage and boat/RV deals, that matters a lot during lease-up and seasonal swings. More fixed claims mean less breathing room if occupancy comes in slower than planned, expenses climb, or off-season cash flow gets thin.

That’s why the debt type matters next.

Aligned vs. Misaligned GP-LP Equity Structures

GP-LP economics can help a deal just as much as debt terms can hurt it. The big issue is simple: if the sponsor gets paid too early, the structure can reward speed over stabilization. And if the sponsor can still make money when the deal falls short, execution tends to slip. In storage and boat/RV deals, that alignment needs to support lease-up, not just nice-looking return targets.

| Structural Element | Aligned | Misaligned |

|---|---|---|

| Preferred Return Design | Cumulative 6%–8% preferred return paid before any promote | A low or non-cumulative pref that can be deferred without much downside for the sponsor |

| Promote Hurdles | Tiered hurdles tied to IRR or equity multiple | A single, easy-to-clear hurdle or promote that can trigger before LP capital is fully returned |

| Fee Load | Clear fees, no double-counting against promote | A high fee load that rewards the GP even when equity returns are mediocre |

| GP Co-Invest | Meaningful co-investment at risk alongside LPs, so the sponsor shares real downside if the deal underperforms | Minimal co-invest, with the GP earning mainly through fees and promote |

| Distribution Waterfall | Return of capital first, then pref, then promote | Early sponsor catch-up or promote participation that allows the sponsor to share in profits before LPs are made whole |

| Hold-Period Alignment | Loan maturity, hold period, and promote should match the same exit timeline | A short loan term or near-term IRR hurdle that pushes toward an early exit before the asset stabilizes |

The biggest pressure points are fee load, exit timing, and whether the sponsor is paid to wait or paid to sell.

Fee load is where things often get buried. Acquisition fees, asset management fees, financing fees, and disposition fees can add up fast. When you stack them together, total sponsor pay can look very different from what the headline waterfall seems to show. That’s why investors should model total GP economics before putting money in.

Hold-period alignment is the other issue that matters a lot in storage and boat/RV deals. If the loan comes due before the property is stabilized, you get a mismatch. That can lead to a forced refinance or a sale close to maturity, which may push the sponsor toward an early exit before the asset’s full upside is realized.

The cleanest structures are usually the easiest to follow:

- A cumulative preferred return in the 6%–8% range

- A promote that starts only after LPs get back capital plus pref

- A GP co-invest large enough that the sponsor feels the downside in a real way

Use these alignment tests before sizing the full stack from the asset up.

How to Build the Capital Stack From the Asset Up

Build the stack from the asset up.

Start with a market and competition analysis. Look at local demand, occupancy, rents, new supply, and concessions. For boat/RV assets, go a step further and check outdoor parking demand, household income, zoning, and access limits. If demand looks soft, the stack needs to be more conservative. That should shape the financing plan from the start. Put simply: the operating picture sets the ceiling for leverage.

Next, build a conservative operating pro forma for base, downside, and upside cases, and track DSCR in each one. Storage and boat/RV deals often come with material capital needs, including gate systems, paving, roofing, security upgrades, software, and unit-turn costs. Those items aren’t side notes. Underwrite reserves as part of the capital stack.

Only after that should you size the debt. Size debt to a stressed DSCR, not just the lender’s minimum. The structure also needs to hold up if rates move higher or lease-up takes longer than planned. Equity should follow that same line of thinking.

Once debt is sized and covenants are reviewed, including DSCR triggers, interest-only periods, extension options, and cash management provisions, the equity structure is the last piece to design, not the first. The waterfall, promote hurdles, and preferred return should match the deal’s actual risk profile. A heavy value-add with a 6- to 12-month lease-up calls for different GP economics than a stabilized, cash-flowing asset. That’s the difference between a disciplined stack and one built backward.

Oakside Co can help stress-test whether the stack matches the asset’s operating path.

Where Specialized Advisory Can Add Value

Once debt, DSCR, and equity terms are mapped, advisory helps confirm that the stack still holds up when the deal moves from a model to an actual closing. The goal is simple: line up underwriting, capital structure, and execution before financing terms are set.

Oakside Co advises self-storage and boat/RV investors with data-driven underwriting, capital-stack design, and transaction management. A stack can look fine in a spreadsheet and still fall apart in practice. That’s where this kind of support matters.

Oakside adds value in three main areas:

- underwriting downside cases

- coordinating lenders and equity partners through closing

- sourcing investors who understand self-storage and boat/RV risk

That work speaks directly to the five mistakes covered above: misaligned debt terms, too much leverage, poor use of mezzanine and preferred equity, weak GP-LP structuring, and stacks built without a clear view of how the property will operate.

Use advisory before financing terms are locked.

Conclusion

These five mistakes usually come from the same issue: the capital stack gets built before the asset is fully underwritten.

That’s where things start to go sideways. When the stack is shaped around return targets instead of what the property can actually support, problems pile up fast. Each mistake cuts into flexibility. Put them together, and a deal that looked workable on paper can become fragile in practice.

Build the stack to hold up in a downside case, not just to get to closing. A sound structure leaves room for slower lease-up, higher costs, and a tougher refinance market. If the deal falls apart under downside pressure, the structure is too aggressive.

For sponsors who want a more resilient structure, Oakside Co can help pressure-test the capital stack against the asset itself.

FAQs

How much DSCR cushion is enough?

It comes down to your risk tolerance and how much the asset’s cash flow can move around. A lender might underwrite based on stabilized performance, but a solid DSCR cushion gives your equity some breathing room if revenue dips or expenses climb out of nowhere.

The best way to figure out how much cushion you need is with sensitivity analysis. Once you know your equity-wipeout boundary – the point where cap rate expansion and slower rent growth would wipe out your initial investment – you can choose a DSCR target that leaves more room for error.

When should mezz debt or preferred equity be avoided?

Avoid mezzanine debt and preferred equity when a property doesn’t have steady cash flow to carry the added debt service or return demands. These layers cost more and add payment pressure, which can eat into profit fast if the asset falls short.

As Nolen Masserman, Managing Director at Oakside, notes, over-leveraging with expensive capital in a tightening market can push a deal toward an equity-wipeout boundary, leaving little room to recover the initial investment.

How do I know if my loan term fits the lease-up timeline?

Start by lining up your loan term with the time it should take the property to stabilize. In most cases, that means reaching 85% to 90% occupancy, and right now that process is taking about 36 months.

If the loan term is too short, even a modest delay can eat into projected yields and push carry costs higher. As Nolen Masserman, Managing Director at Oakside, notes, misaligning debt terms with the lease-up lifecycle is a common mistake.