If I had to boil it down to one line, it’s this: lower-cost loans fit stabilized properties, while higher-cost capital fits deals that still need time, lease-up, or a fast close.

In 2026, self-storage, boat, and RV investors are often choosing between bank, SBA, CMBS, or life company debt on one side and bridge loans, private debt, mezzanine debt, preferred equity, or JV equity on the other. The split is simple: cost vs. flexibility.

Here’s the short version:

- Conventional loans often price in the mid-5% to 8.5% range

- Alternative capital often lands around 8.0% to 10.5%+ or SOFR + 395 bps

- Banks may want 25% to 35% equity

- Debt service tests often sit around 1.25x to 1.30x DSCR

- Proceeds often end up around 50% to 65% LTV on tighter deals

- Stabilized assets often need about 85% to 90% occupancy

- Conventional closings often take 60 to 90 days

- Bridge and private debt can close in about 21 to 45 days, and sometimes less

What I look at first is simple:

- Cost

- Leverage

- Time to close

- Recourse

- Prepayment limits

- Asset stage

- Exit plan

If a property has clean trailing income, permanent debt is often the better fit. If it’s in lease-up, conversion, renovation, or ground-up development, alternative capital may fit better even if the rate is higher. The cheapest loan is not always the best loan.

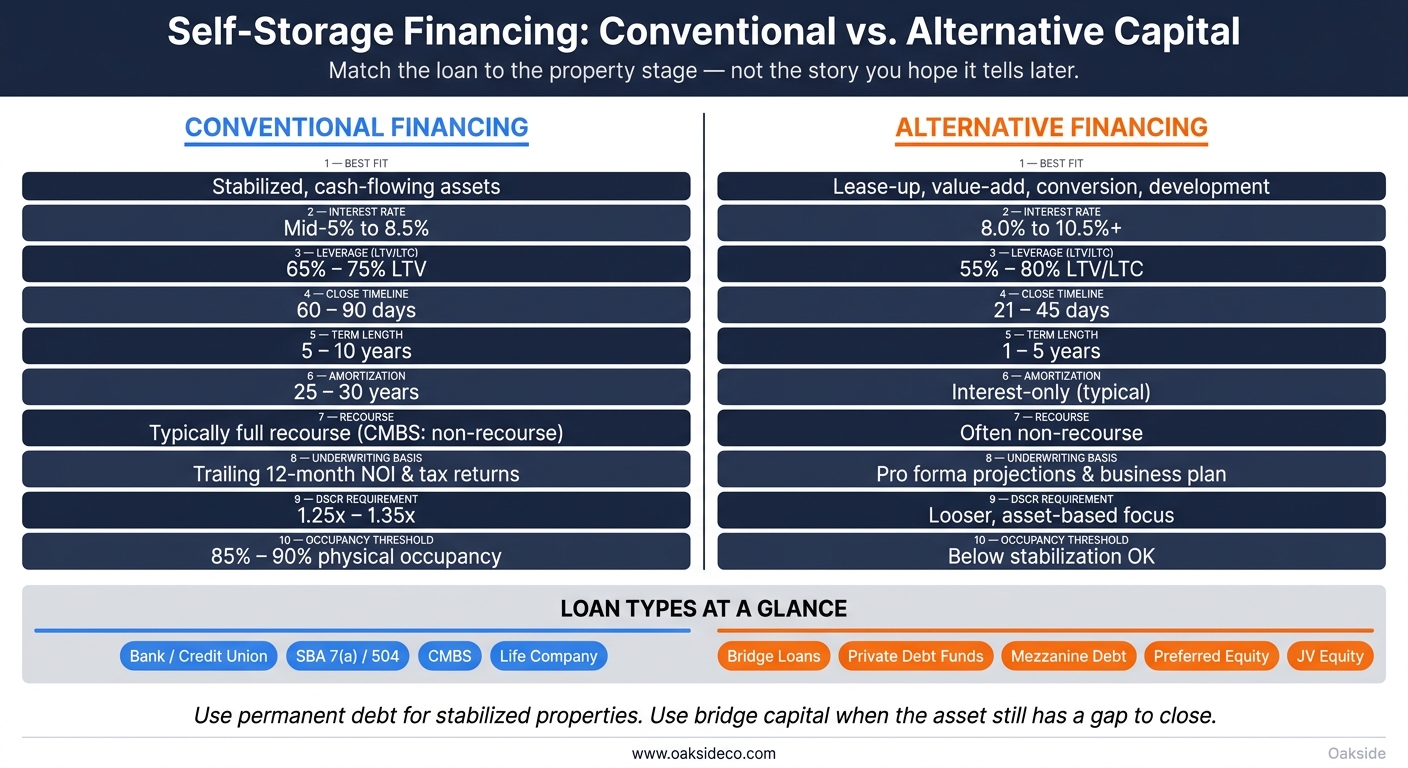

Self-Storage Financing: Conventional vs. Alternative Capital at a Glance

Quick Comparison

| Factor | Conventional Financing | Alternative Financing |

|---|---|---|

| Best fit | Stabilized, cash-flowing assets | Lease-up, value-add, conversion, development |

| Cost | Lower | Higher |

| Rate range | Mid-5% to 8.5% | 8.0% to 10.5%+ |

| Leverage | Often 65% to 75% LTV | Often 55% to 80% LTV/LTC |

| Close timeline | 60 to 90 days | 21 to 45 days |

| Underwriting | In-place income and trailing NOI | Pro forma and business plan |

| Recourse | Often full recourse, with some non-recourse options | Often non-recourse |

| Term | 5 to 10 years | 1 to 5 years |

| Best use | Long hold after stabilization | Short-term bridge to refinance or sale |

My takeaway: match the loan to the property’s current stage, not the story you hope it tells later.

sbb-itb-09b4138

Conventional financing: lower cost, tighter underwriting

Conventional debt is usually the pricing baseline for self-storage loans. It tends to offer lower cost and longer amortization, but underwriting is tighter. That’s why many self-storage borrowers start here. The catch is simple: lenders underwrite based on in-place income, not projections. If the asset hasn’t reached that point yet, many borrowers have to look at alternative capital.

Bank, credit union, SBA, CMBS, and life company loans

Not all conventional loans fit the same deal. Each one lines up with a different borrower type, leverage target, and asset stage.

| Loan Type | Best For | Typical LTV | Recourse | Prepayment |

|---|---|---|---|---|

| Bank / Credit Union | Local operators, stabilized assets | 65%–75% | Full recourse | Step-down (e.g., 5-4-3-2-1) |

| SBA 7(a) / 504 | First-time buyers, high leverage | Up to 85%–90% | Full recourse | Declining % over term |

| CMBS | Large portfolios, non-recourse needs | Up to 75% | Non-recourse | Yield maintenance or defeasance |

| Life Company | Institutional-quality, long-term hold | 50%–65% | Non-recourse | Flexible |

Community banks and credit unions are often relationship-based lenders. They’re a common fit for local operators buying or refinancing stabilized assets. Rates currently run from 7.0% to 8.5%, and most of these loans come with full recourse.

SBA 7(a) and 504 loans can push leverage much higher, up to 85% to 90% LTV, with 20- to 25-year amortization. The SBA 7(a) program caps at $5 million, which makes it a strong fit for smaller acquisitions and first-time buyers. Pricing is usually based on Prime plus a margin.

CMBS loans are fixed-rate, non-recourse loans with 30-year amortization schedules. Rates currently fall in the 6.25% to 7.75% range. These loans fit stabilized, institutional-quality assets, especially when the borrower wants long-term fixed debt without personal liability. But there’s a tradeoff: closing costs of about $25,000 to $35,000 can make CMBS a poor fit for smaller loan amounts.

Life insurance companies usually sit at the low end of the conventional pricing stack. Rates are currently in the low-6% to low-7% range. Still, they’re selective. They usually want newer-vintage, institutional-quality assets backed by experienced sponsors, and they keep leverage in the 50% to 65% LTV range. In return, borrowers can get long-term fixed rates and non-recourse terms that make sense for long holds.

Where conventional debt works best

The main issue is whether the asset is mature enough to qualify. Conventional debt works best when occupancy and collections are stable. Put plainly, it tends to fit after the asset has stabilized and the business plan has already been proven.

Lenders usually want 85% to 90% physical occupancy and a DSCR of 1.25x to 1.35x. But physical occupancy alone doesn’t tell the whole story. Lenders underwrite to economic occupancy, not just how many units are filled. They care about rent actually collected.

That distinction matters. A facility can look full on paper but still miss the mark if it relies too much on discounts or promotions. In that case, unit count may look fine while income does not. Clean collections matter more than a full rent roll.

If the deal has a tight timeline, or the asset hasn’t fully stabilized yet, alternative capital can be a better match. That’s usually where the comparison starts to shift.

Alternative financing: more flexibility, higher cost

When a self-storage deal falls outside a bank’s rules, alternative capital steps in. It moves faster, gives borrowers more room to work, and costs more. In most cases, alternative lenders charge 150 to 250 basis points more than banks and other standard lenders.

That tradeoff is simple: more speed and more flexibility, at a higher price. This is where standard underwriting stops and transitional capital starts.

Bridge loans, private debt, mezzanine debt, preferred equity, and JV equity

These options mainly differ in two ways: where they sit in the capital stack and how much control the sponsor keeps. These structures directly impact self-storage cap rates and overall property valuation.

Bridge loans and private debt funds are usually the first stop in alternative financing. Bridge loans are short-term, usually 1 to 5 years, and are often interest-only and non-recourse. They’re built to carry a property through a transition until it can qualify for permanent financing. Leverage can go up to 70% to 80% LTV, and funding may happen in as little as 3 to 6 weeks.

Private debt funds play a similar role, but they can move even faster. In some cases, they can fund in less than a week.

Mezzanine debt and preferred equity help fill the gap above a senior loan when the sponsor wants more leverage without putting in more common equity. Both sit above senior debt and below common equity in the stack. Preferred equity usually comes with a preferred return of 6% to 10%, which must be paid before common equity holders get distributions.

That extra layer can make a shaky deal pencil out. But it also adds cost and structure to manage.

Joint venture (JV) equity works differently. Instead of making a loan, the partner takes an ownership stake. One common setup is a 90/10 split, with the equity partner putting in most of the capital in exchange for a preferred return, while the sponsor keeps day-to-day control of the asset.

When alternative capital is the better fit

Alternative capital tends to work best when the property needs time or when the closing window is tight. Lease-up, conversion, and renovation deals often have the same problem: they are not stable enough yet for permanent debt. If occupancy is still below what a bank wants to see, bridge capital can buy the time needed to get there.

Still, this money is a bridge, not a long-term answer. Every alternative structure needs a clear way out, usually through a sale or a refinance into permanent debt once the asset is stable. Without that exit, maturity risk can climb fast.

A smart move is to negotiate extension options at the start. That can give the borrower a bit more breathing room if the business plan takes longer than expected. The contrast with standard financing shows up even more clearly in the side-by-side comparison below.

Conventional vs. alternative: side-by-side comparison

This choice usually comes down to one simple tradeoff: lower cost with tighter underwriting versus higher cost with more room to maneuver. The table below makes that tradeoff easy to see.

Comparison table: terms, structure, and execution tradeoffs

| Metric | Conventional (Bank / Life Co / CMBS) | Alternative (Bridge / Private Debt / Mezzanine / Equity) |

|---|---|---|

| Interest Rate | Mid-5% range; roughly 1.85%–2.85% over the 10-year Treasury | 8.0%–10.5%+ |

| Leverage (LTV / LTC) | 65%–75% | 55%–80% |

| Term Length | 5–10 years | 1–5 years |

| Amortization | 25–30 years | Interest-only, typically |

| Recourse | Typically recourse; CMBS is the main exception | Often nonrecourse |

| Speed to Close | 60–90 days | 21–45 days |

| Underwriting Basis | Trailing 12-month NOI, tax returns, and borrower-level cash flow | Pro forma projections, unit-level rent ramps, and market absorption |

| Prepayment Flexibility | Moderate; CMBS can include strict yield maintenance | Highly flexible |

| Covenants | Strict; DSCR minimums of 1.25x–1.35x | Looser, with a more asset-based focus |

| Best-Fit Use Case | Stabilized, cash-flowing assets | Value-add, lease-up, and conversion projects |

Which option fits each stage of the asset lifecycle

The right fit shifts as the asset moves from one stage to the next.

For a stabilized refinance, CMBS or life company debt is often the best match once a facility is near 90% occupied and showing clean trailing income. At that point, the property looks more like what permanent lenders want: steady cash flow, fewer loose ends, and less guesswork.

For ground-up development, things look different. Regional banks have pulled back on construction lending and often ask for larger deposit relationships or personal guarantees. That has pushed more borrowers toward debt funds and private credit, especially for deals that fall outside strict bank rules.

For lease-up or conversion, bridge capital is often the better tool. It can be set up with interest reserves when in-place cash flow still isn’t enough to support permanent debt. Then, once occupancy gets to roughly 90%, owners often refinance into CMBS or life company debt.

That stage-by-stage fit is what shapes the final capital stack decision.

Conclusion: Choosing the right capital stack for self-storage investments

When you line up the options side by side, the answer comes down to fit. This isn’t about picking conventional or alternative financing in the abstract. It’s about choosing the structure that matches the asset’s stage.

Conventional debt usually costs less. Alternative capital gives you more room to shape the loan around the deal. And that matters. A slightly higher-cost loan can beat a cheaper one if it fits the business plan better.

Stabilized assets tend to work best with permanent debt. Transitional assets usually need capital that can carry the deal through a lease-up or value-add period. Put simply: use permanent debt for stabilized properties, and use bridge capital when the asset still has a gap to close.

Here’s a simple rule of thumb:

- Conventional financing fits stabilized, cash-flowing assets where the goal is to keep borrowing costs low and lock in long-term stability.

- Alternative financing fits transitional or value-add deals where speed, higher leverage, or a nonstandard borrower profile is part of the picture.

- Structure matters as much as rate: a loan with more flexible amortization and prepayment terms can outperform a cheaper loan with rigid constraints over the life of a deal.

- Match prepayment flexibility to your hold period: shorter holds need room to exit cleanly, while longer holds can gain from locked-in fixed rates.

In self-storage finance, the best structure is the one that supports the plan from acquisition to exit.

FAQs

How do I know if my property is stabilized enough for a conventional loan?

Lenders usually treat a self-storage property as stabilized when the numbers show steady performance and dependable income.

The usual markers are 85% to 90% occupancy with a positive or improving 12-month trend, a DSCR of 1.25x to 1.30x, and an operating expense ratio of 30% to 40%. Just as important, the property needs clear, verifiable financial records to back up those figures.

When does a higher-cost bridge loan make more sense than cheaper permanent debt?

A higher-cost bridge loan can make sense when a project doesn’t yet qualify for lower-rate permanent debt. That often happens with a value-add acquisition, a conversion, or a facility still in lease-up.

Yes, the rate is higher. But the tradeoff is flexibility. A bridge loan gives the borrower time to finish improvements, stabilize the property, and then refinance into lower-cost permanent debt once the property hits the required performance metrics.

What exit plan do lenders expect for lease-up or value-add self-storage deals?

Lenders usually want to see a clear exit plan: refinance into a permanent, long-term loan once the property is stabilized.

That’s the whole point of a short-term bridge loan. It helps fund the deal until occupancy or revenue improves enough for the property to qualify for longer-term financing.

As Nolen Masserman, Managing Director at Oakside, notes, a defined path to stabilization matters. And Cameron Vale, President at Oakside, stresses the same idea from the business-plan side: you need to clearly show how the plan will improve performance.