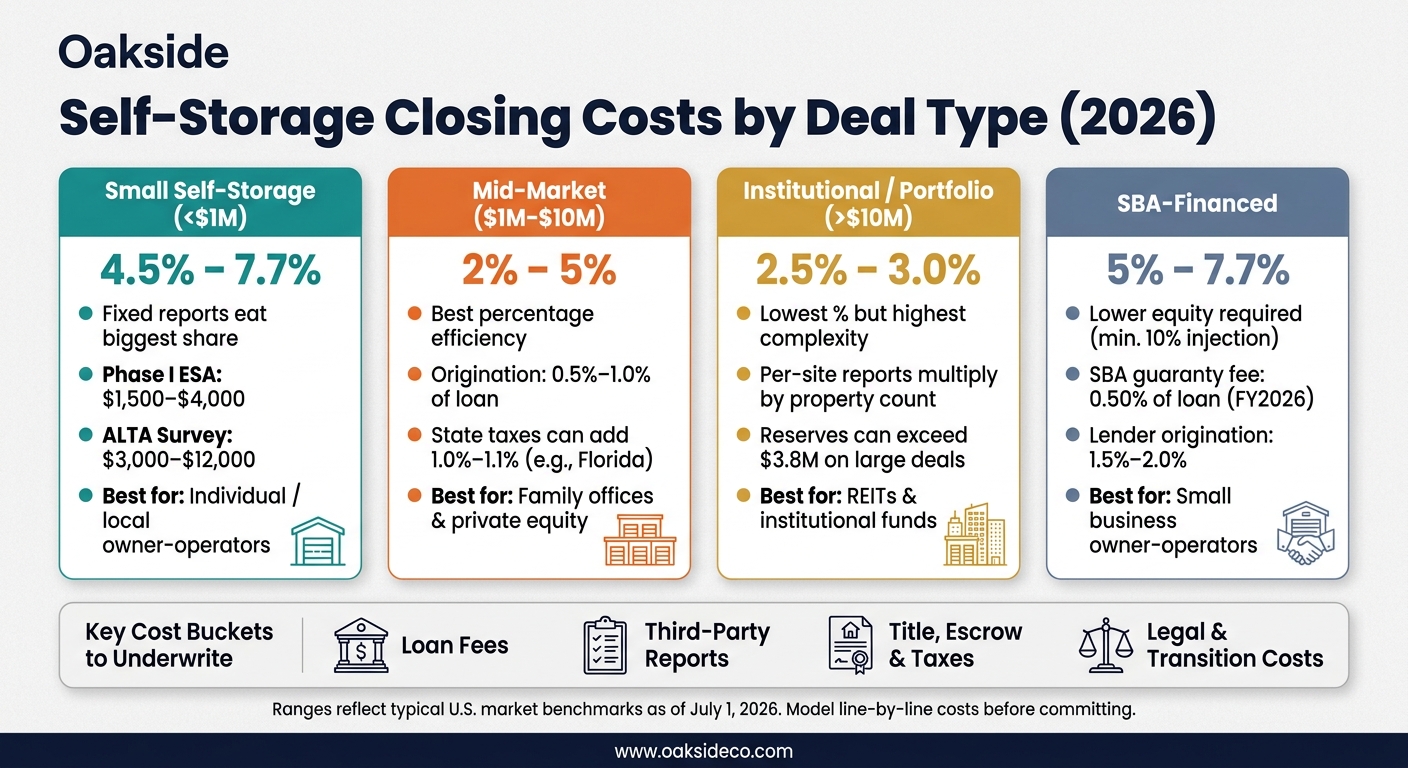

If I’m buying self-storage, I’d budget closing costs by deal type first, not by a flat rule of thumb. In this piece, the main ranges are clear: small deals often run 4.5%–7.7%, mid-market deals 2%–5%, portfolio deals 2.5%–3.0%, and SBA-financed deals 5%–7.7% as of July 1, 2026.

Here’s the short version:

- Small deals get hit hardest because fixed reports, title, escrow, and legal bills take up more of the price.

- Mid-market deals usually get better percentage math, even though the closing process is still not cheap.

- Portfolio deals can show lower percentage costs, but cash needed at close can still be high because of reserves, site-by-site reports, and more legal work.

- SBA deals can lower upfront equity, but lender fees, SBA fees, and escrows often push total closing costs up.

If I were underwriting a deal, I’d watch four buckets first:

- Loan fees

- Third-party reports

- Title, escrow, and taxes

- Legal and transition costs

Self-Storage Closing Costs by Deal Type (2026)

Quick Comparison

| Deal Type | Typical Buyer Closing Cost Range | Main Cost Pressure |

|---|---|---|

| Small self-storage | 4.5%–7.7% | Fixed reports and fees |

| Mid-market | 2%–5% | Loan terms and state taxes |

| Institutional/portfolio | 2.5%–3.0% | Multi-site reports, reserves, legal work |

| SBA-financed | 5%–7.7% | SBA fee stack and larger escrows |

Bottom line: I’d use the percentage ranges only as a starting point. The safer move is to build a line-by-line closing budget early, because lender structure, state taxes, and reserve demands can change the cash needed at close by a lot.

sbb-itb-09b4138

1. Small Self-Storage Acquisition

Small self-storage deals – often around $1 million – can get hit hard by closing costs. In this price range, buyers should plan for total closing costs of about 4.5% to 7.7% of the purchase price.

The big reason is simple: many due diligence and closing fees are fixed. They don’t shrink just because the property costs less. So on a smaller deal, they eat up a bigger piece of the budget.

For example:

- A Phase I Environmental Site Assessment usually costs about $1,500 to $4,000

- ALTA/NSPS surveys can add $3,000 to $12,000

- Appraisals often run $2,000 to $10,000

- Escrow fees can land around $1,000 to $3,500

On a $1 million purchase, those items alone can take up 1% to 2% of the price before lender fees even enter the picture.

Fixed Due Diligence Costs

These third-party costs are mostly non-negotiable. Lenders often require them, and the work itself doesn’t change much based on what the property is worth. A survey is still a survey. An environmental report still takes the same type of review.

One small way to cut costs: ask the title company for a simultaneous issue discount if the owner’s and lender’s title policies are issued at the same closing. That can lower title costs.

Financing & Legal Complexity

Your loan choice can change the cash you need in a big way. A conventional bank loan may keep total costs closer to the low end of the range. A DSCR loan, on the other hand, can push costs up because origination fees may reach 2%, and the lender may also require reserves for taxes and insurance.

Legal work can add another layer of expense. Buyer-paid lender legal fees often run $2,000 to $5,500+.

Buyer Cash Needed at Close

If you’re using financing, it’s smart to underwrite extra cash at close. Lender fees and reserve requirements can add up fast, while all-cash buyers avoid those line items.

Prorations can move the final number too. Prepaid rent and property tax adjustments may push cash needed at closing up or down depending on the closing date.

As the deal size gets larger, these fixed costs take up a smaller share of the purchase price.

2. Mid-Market Self-Storage Deal

At this size, fixed fees don’t hit as hard as they do in smaller deals. But lender terms and state taxes can still change the total in a big way.

Total Cost %

Mid-market self-storage deals – usually in the $1 million to $10 million range – tend to get better fee efficiency than smaller purchases. In most cases, buyers should plan on 2% to 5% of the purchase price for closing costs.

On a $5 million deal, buyer closing costs often come in around $60,000 to $80,000. So yes, the math gets a bit better. But the closing process itself isn’t much cheaper.

Fixed Third-Party Fees

This is where scale starts to help.

A Phase I Environmental Site Assessment still costs about $2,000 to $4,000, a Property Condition Assessment usually lands at $1,500 to $4,000, and a commercial appraisal often runs $3,000 to $10,000. On a $5 million deal, those same charges take up a smaller slice of the deal than they would on a $1 million buy.

Title insurance also gets more efficient at this level. Many policies use tiered pricing, which means the cost per $1,000 of value tends to drop as the deal size goes up.

Financing & Legal Complexity

Financing still has a big effect on total cost.

A standard commercial mortgage often comes with origination fees of 0.5% to 1% of the loan amount. Some lenders push that as high as 2%. That gap matters.

State taxes can also shift the numbers fast. In Florida, for example, documentary stamp taxes and intangible taxes alone can add up to 1.0% to 1.1% of the purchase price on a financed deal. If you’re buying in a high-tax state, it’s smart to price that in early rather than get hit with it at the closing table.

Buyer Cash Needed at Close

The closing cost percentage isn’t the whole story.

Buyers also need to plan for lender reserve requirements. These are upfront reserve accounts for taxes, insurance, and replacements that lenders often want funded at closing. They increase the cash you need to bring, even if they aren’t all closing costs in the strict sense.

Prorations for prepaid rents and property taxes can also move the final number based on the closing date. They don’t create a net new cost, but they can change how much cash is due at close.

At the next size up, more parties and more paperwork start adding cost right alongside the property itself.

3. Institutional or Portfolio Self-Storage Transaction

Portfolio deals can trim percentage-based closing costs because fixed expenses get spread across a bigger deal size. But there’s a catch: the process gets more tangled, and buyers usually need more cash ready at closing.

Total Cost %

For portfolio deals, buyer-side closing costs often land around 2.5% to 3.0% of total transaction value. That’s lower than what you’d often see on smaller deals, but the tradeoff is a much more involved closing process.

Fixed Third-Party Fees

This is where things can stack up fast. In a portfolio deal, each asset often needs its own diligence package. So even though the deal is one transaction, many third-party costs repeat property by property.

A Phase I Environmental Site Assessment usually costs $2,000 to $6,000+ per site. An ALTA/NSPS Land Title Survey can cost $8,000 to $25,000+ per parcel. And a commercial appraisal often runs $10,000 or more for large or specialized properties. Buy five facilities, and in most cases, you’re ordering those reports five separate times.

It also makes sense to set aside money for data migration and system integration.

Financing & Legal Complexity

Financing can get expensive fast when the structure has a lot of moving parts. Mezzanine debt, multiple loan tranches, and CMBS loans can push lender legal fees well past the level of a simpler deal. Floating-rate bridge loans usually require an interest rate cap too, which adds one more item to the closing budget.

If there’s an existing CMBS loan and the buyer isn’t taking it on, defeasance or yield maintenance may add a material payoff cost. And if the seller is foreign, FIRPTA withholding can require a 15% holdback along with extra administration.

That’s why these deals can look cost-efficient on paper but still feel expensive when you’re in the middle of them.

Buyer Cash Needed at Close

Closing costs are only part of the story. Institutional lenders often require big reserve deposits at closing, including replacement reserves, tax and insurance escrows, and in some cases deferred maintenance reserves.

One modeled $131 million self-storage portfolio required a $3.865 million working capital reserve. That amount wouldn’t usually show up in a basic closing-cost estimate, but it can have a major effect on how much cash a buyer needs to bring to the table.

These costs usually fall into a few main buckets: financing, diligence, title, legal, and transition.

4. SBA-Financed Self-Storage Acquisition

SBA financing changes closing costs less because of deal size and more because of lender rules. It can cut the equity needed at closing, but that trade-off comes with added lender fees and larger escrow requirements. You’ll see that hit in both the fee stack and the cash you need to park at close.

Total Cost %

SBA-financed self-storage acquisitions usually land in the 5% to 7.7% range of the purchase price for closing costs.

Financing & Legal Complexity

SBA-backed financing adds SBA-specific charges on top of normal closing costs. For fiscal year 2026, from Oct. 1, 2025, to Sept. 30, 2026, the upfront guaranty fee is 0.50% of the loan amount. There’s also an annual service fee of about 0.21% of the outstanding balance.

On top of that, the lender charges its own origination fee. For SBA deals, that fee is usually 1.5% to 2.0%, versus 0.5% to 1.0% for conventional loans.

Lender legal fees also tend to be higher because SBA compliance adds more drafting and review work.

Fixed Third-Party Fees

SBA loans still call for the usual Phase I, PCA, survey, and appraisal. So even with SBA debt, fixed due diligence costs stay heavy, especially on smaller acquisitions.

Buyer Cash Needed at Close

The biggest shift is the cash needed at closing. SBA lenders often require 12 to 18 months of tax and insurance escrows, plus a minimum 10% equity injection based on total project cost. At least 5% of that must come from the buyer’s own cash.

Here’s the side-by-side view:

| Fee Category | Conventional Small-Balance | SBA Financing |

|---|---|---|

| Origination Fee | 0.5% – 1.0% | 1.5% – 2.0% + SBA fees |

| SBA Guaranty Fee | N/A | 0.50% (FY 2026) |

| Third-Party Reports | $10,000 – $25,000+ | $15,000 – $30,000+ |

| Tax/Insurance Reserves | ~6 months | 12 – 18 months |

| Total Buyer Cost % | ~2% – 4.5% | ~5% – 7.7% |

Typical ranges above reflect lender fee benchmarks, SBA guaranty fees, third-party report pricing, and reserve requirements.

How Closing Costs Break Down by Category

Across deal types, closing costs usually land in four main buckets: lender and financing charges, third-party reports, title and escrow, and legal and transition costs. The mix shifts with deal size, but these same buckets show up in every closing. Here’s how they change across the four deal profiles.

Lender and Financing Charges

Origination fees tend to move the most with deal size. As the deal gets larger, those fees usually drop as a share of the loan. SBA financing adds a separate upfront guaranty fee of 0.50% of the loan amount for FY 2026, plus more lender work. That’s why SBA deals often end up with higher total financing charges than conventional loans of a similar size.

Third-Party Reports and Inspections

Phase I environmental assessments, ALTA surveys, property condition assessments, and appraisals are mostly fixed-cost items. That’s the key point. The same base spend takes up a much bigger chunk of a $1 million purchase than a $10 million one.

Portfolio deals add another layer. These costs usually multiply by site count, so a five-property acquisition will often require five separate rounds of reports.

Title, Escrow, Recording, and Transfer Taxes

Once lender and diligence costs are on the table, taxes and title often decide how much the final closing bill changes from one state to another. Transfer taxes swing the most. Texas and Arizona are 0%, Pennsylvania is 2%, and some jurisdictions push total transfer taxes above 5%.

Florida is a good example of how financing can change the math. There, documentary stamps and intangible tax can total about 1.0% to 1.1% of transaction value on a financed deal.

Legal, Advisory, and Transition Costs

These are often the costs people notice last, even though they can create the biggest headaches in larger transactions. For institutional buyers, entity formation usually runs about $15,000, with monthly legal and accounting retainers of $3,000 to $7,000 during the acquisition phase.

That’s part of what makes larger deals harder to execute. It’s not just that the numbers are bigger. The work gets messier too. Platform migration and tenant-data transfers can add $500 to $5,000+, depending on the system.

The table below shows where the biggest cost differences tend to come from across the four deal profiles.

| Cost Category | Small Deal (<$1M) | Mid-Market ($1M–$20M) | Institutional/Portfolio | SBA-Financed |

|---|---|---|---|---|

| Lender Origination | 1.0% – 2.0% | 0.5% – 1.0% | 0.5% – 1.0% | 0.5% – 1.5% + 0.50% SBA fee |

| Title Insurance | ~0.5% – 1.0% | Tiered (lower %) | Tiered (lowest %) | ~0.5% – 1.0% |

| Legal/Entity | $1,500 – $3,000 | $5,000 – $15,000 | $50,000+ (Platform/Entity) | $3,500 – $7,500 |

| Software/Data Migration | $500 – $5,000 | $500 – $5,000 | $500 – $5,000+ | $500 – $5,000 |

Ranges reflect typical U.S. market benchmarks across deal profiles.

Pros and Cons by Deal Profile

The same cost buckets can feel very different depending on deal size. That’s the core tradeoff here: small deals get hit harder by fixed fees, mid-market deals tend to look better on a percentage basis, institutional deals spread costs across more value, and SBA loans cut the cash needed at closing but add loan-related fees.

Small Deals: Fewer Dollars, Higher Percentage Cost from Fixed Fees

The big draw of a small acquisition is simple: you’re putting fewer dollars at risk. But there’s a catch. Fixed diligence costs don’t shrink just because the purchase price is lower, so routine third-party reports can take up a big chunk of the deal.

On deals around $1 million, buyer closing costs usually land between 4.5% and 7.7% of the purchase price.

Mid-Market Deals: Lower Percentage Costs

Mid-market deals often hit a sweet spot. You still get a fairly straightforward closing process, but fixed costs start to look much smaller as a share of the purchase price. That’s why this part of the market often gives buyers the best mix of scale and deal simplicity.

For deals in the $1 million to $10 million range, buyer closing costs usually fall between 2% and 5% of the purchase price.

Institutional or Portfolio Deals: Scale With Added Complexity

At larger deal sizes, the issue usually shifts. It’s less about the raw cost and more about how much coordination the deal demands. Buyers can benefit from tiered title insurance and from spreading legal costs across multiple assets, which helps keep closing costs in a fairly tight range of 2.5% to 3.0% of transaction value.

That said, bigger deals come with more moving parts: layered financing, heavier legal work, and site-level diligence that grows with each property in the portfolio.

SBA-Financed Deals: Lower Equity Required at Close, More Loan Fees

SBA financing changes the math again. The main upside is lower cash needed at closing. A minimum 10% equity injection can keep the upfront cash need lower. But that lower entry point comes with a thicker fee stack.

For FY 2026, the SBA upfront guaranty fee adds 0.50% of the loan amount, on top of standard origination and compliance costs. As a result, SBA-financed deals usually end up in the 5% to 7.7% total closing cost range.

The table below sums up the main buyer tradeoffs by deal profile.

| Small Deals (<$1M) | Mid-Market ($1M–$10M) | Institutional/Portfolio (>$10M) | SBA-Financed | |

|---|---|---|---|---|

| Est. Buyer Closing Costs | 4.5%–7.7% | 2%–5% | 2.5%–3.0% | 5%–7.7% |

| Key Strength | Lower absolute capital required | Best blend of scale and simplicity | Scale reduces per-asset costs | Lower equity required at close |

| Key Weakness | Fixed costs create higher percentage cost | More fixed costs than institutional scale | High legal complexity and coordination | Heavy compliance; SBA-specific fees |

| Best-Fit Investor | Individual/local owner-operators | Family offices and private equity | REITs, institutional funds, and large portfolios | Small business owner-operators |

Conclusion

Closing costs usually have less to do with the property itself and more to do with deal size, financing, and how complex the process gets. These factors also directly influence self-storage cap rates and overall property valuation.

Across all four deal types, the mistake shows up in the same place: people often underestimate fixed costs and financing costs. The smart move is to model closing costs line by line as early as the LOI stage.

On smaller deals, fixed costs can eat into the numbers fast. Get third-party quotes early, and put lender quotes side by side before you move ahead.

As deal size grows, the main problem often shifts from the dollar amount to coordination. That’s where Oakside Co can help keep execution organized.

Percentage ranges are a starting point, not the answer. Underwrite a full line-item budget before you commit. That’s the real closing-cost test: accuracy before commitment.

FAQs

What’s included in closing costs?

Closing costs are the fees and expenses you pay to finish a self-storage real estate deal.

For buyers, that usually means loan fees, the appraisal, environmental and property inspections, the survey, title insurance, and recording charges. Sellers usually cover brokerage commissions, attorney fees, and any transfer taxes. Closing costs can also include prorated property taxes and prepaid tenant rents.

How much cash should I bring to closing?

Buyers should usually plan for closing costs equal to 2% to 5% of the purchase price. The exact amount depends on the property’s location, how complex the deal is, and how the loan is set up.

These costs often include lender fees, due diligence costs, title insurance, attorney fees, and recording costs or transfer taxes. On top of that, buyers also need to bring their down payment to closing, which is often 30% to 40% for conventional loans.

Which closing costs are negotiable?

Many closing costs are negotiable in the purchase agreement, even though buyers or sellers often pay them by custom.

Common examples include title insurance, survey costs, and certain transfer taxes. In some deals, a motivated seller may also agree to pay part of the buyer’s closing costs to help get the deal across the finish line.