Sell the wrong way, and taxes can take 35% to 45% of your gain. If I’m selling a self-storage, boat, or RV property, I need to plan before closing if I want to defer tax, spread it out, or cut it down.

Here’s the short version:

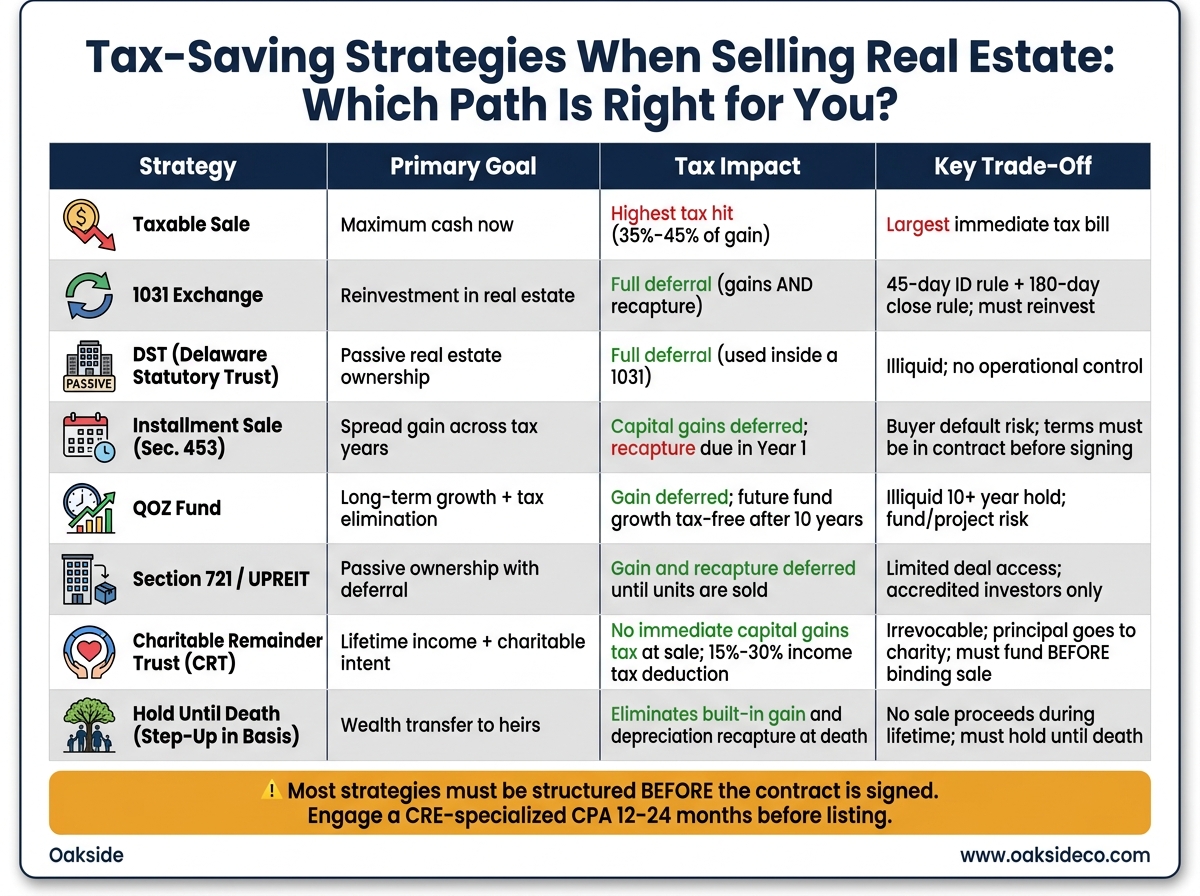

- 1031 exchange: I defer capital gains and depreciation recapture by buying other U.S. real estate.

- Installment sale: I spread capital gains over future tax years, but recapture is still due in Year 1.

- QOZ fund: I roll my gain only into a fund within 180 days and may avoid tax on future fund growth after 10 years.

- Section 721 / UPREIT: I swap property for partnership units and defer tax until I sell the units.

- Step-up in basis: If I hold until death, my heirs may inherit at fair market value and avoid built-in gain tax.

- CRT: I move the property into a trust before any binding sale, the trust sells without immediate capital gains tax, and I can get income plus a charitable deduction.

The main point is simple: most of these options stop working once I sign the deal or receive the money.

A fast way to think about it:

| Option | What I get | Main limit |

|---|---|---|

| Taxable sale | Cash now | Highest tax hit |

| 1031 exchange | Tax deferral into new real estate | 45-day ID rule, 180-day close rule |

| DST in a 1031 | Passive real estate ownership | Illiquid, less control |

| Installment sale | Payments over time | Recapture due right away |

| QOZ fund | Deferral on gain, no tax on later fund growth if held 10+ years | Long hold, fund risk |

| 721 / UPREIT | Passive ownership with deferred tax | Limited deal access |

| CRT | Income stream and no immediate capital gains tax at sale | Irrevocable, charity gets remainder |

| Hold until death | Heirs may avoid built-in gain tax | No sale proceeds now |

If I want to keep more of the sale proceeds, I need to match the structure to my goal: cash now, reinvestment, passive income, or estate planning.

That’s the whole issue in one line: the tax outcome is often set before the property ever closes.

Tax Strategies for Real Estate Sellers: Compare Your Options

Tax-Deferral Strategies That Can Preserve More Sale Proceeds

If a sale will create a tax bill, it helps to look at your options before you list the property. Each path lines up with a different goal: putting money back into real estate, creating income over time, holding for years, or moving into a more passive role.

1031 Exchanges: Defer Tax by Reinvesting in Other Real Estate

A Section 1031 exchange lets you sell a self-storage, boat, or RV property and move the proceeds into another piece of U.S. real estate without triggering capital gains or depreciation recapture in the year of sale. The IRS applies like-kind rules broadly, so a self-storage sale can roll into apartments, retail, land, or industrial real estate.

Two deadlines run the whole process:

- You have 45 days after closing to identify replacement property in writing.

- You have 180 days to close on that property.

Miss either one, and the exchange is disqualified.

There’s another hard rule here: a Qualified Intermediary must hold the sale proceeds. The money cannot hit your bank account at any point. If it does, the exchange fails. To defer 100% of the tax, the replacement property needs to be equal or greater in value, and any debt paid off on the sold property has to be replaced with new debt or extra cash. Any leftover taxable cash from the exchange is taxed right away.

That’s why smart sellers start looking for replacement options early. Delaware Statutory Trusts (DSTs) can also work if you want a more passive route. And timing matters. The 45-day window goes by fast.

If you don’t want to reinvest, an installment sale may fit better.

Installment Sales: Spread the Gain Across Multiple Tax Years

An installment sale under Section 453 lets a self-storage, boat, or RV owner spread capital gain recognition across the years when payments are actually received, instead of stacking the full gain into one tax year. Each payment is divided into basis, gain, and interest.

That can help keep more income in lower tax brackets.

But there’s a catch, and it’s a big one: depreciation recapture is still due in full in the year of sale. The IRS requires all Section 1250 recapture to be recognized no matter how the payment schedule is set up. So if you go this route, the down payment needs to be large enough to cover that recapture bill.

| Feature | Installment Sale (Section 453) | 1031 Exchange |

|---|---|---|

| Liquidity | Periodic cash flow (principal + interest) | Low (capital tied in new property) |

| Tax Deferral Scope | Capital gains only (recapture due Year 1) | Full deferral (gains and recapture) |

| Management Burden | Passive (acting as the lender) | Active (unless using a DST) |

| Risk | Buyer default/credit risk | Market risk of replacement property |

One more thing: installment sale terms must be negotiated and written into the purchase contract before it is signed. You can’t tack them on after closing.

For many owners, 1031 exchanges and installment sales are the first two tools to review. The next pair is more specialized.

Qualified Opportunity Zones and Section 721 Structures

These two options are narrower, but for the right seller, they can work well.

A Qualified Opportunity Zone (QOZ) investment lets you roll only the gain portion of your sale into a Qualified Opportunity Fund (QOF) within 180 days, while keeping your original basis liquid. If you hold the fund investment for at least 10 years, any new appreciation inside the fund is permanently excluded from capital gains tax. This tends to fit sellers with a long time horizon who want to wipe out tax on future growth, not just push off today’s gain.

A Section 721 contribution to an UPREIT works in a different way. Instead of selling, you contribute your self-storage, boat, or RV property to a REIT’s operating partnership in exchange for operating partnership units. Tax on the gain and depreciation recapture is deferred until you sell those units or the REIT sells the property. It can make sense for owners who want passive ownership with tax deferral.

There are limits, though. QOZ funds and many Section 721/DST setups are often limited to accredited investors, and they come with governance and timing restrictions.

If deferral alone won’t do the job, the next set of tools shifts from delaying tax to cutting it down or removing it.

sbb-itb-09b4138

Ways to Reduce or Eliminate Tax Rather Than Just Defer It

If deferral doesn’t match your goal, the next set of options aims to cut tax now or wipe it out later.

Step-Up in Basis: How Estate Planning Can Eliminate Built-In Gain

For owners who care more about heirs than current liquidity, a step-up in basis can be the cleanest way out. At death, heirs get a step-up in basis to fair market value. That can erase built-in capital gain and deferred depreciation recapture.

A lot of owners pair this with repeated 1031 exchanges during life, then keep the last asset until death. If heirs sell right away, they may owe little to no federal tax.

This path makes sense for owners who don’t need cash now and want to pass wealth to the next generation.

If you do need income during your lifetime, a CRT takes the conversation in a different direction.

Charitable Remainder Trusts: Generate Income and Cut the Tax Bill

A Charitable Remainder Trust works only if the property goes into an irrevocable trust before any sale becomes binding. The trust is tax-exempt, so it can sell the property without immediate capital gains tax. That means the full gross proceeds can stay invested, which may support a larger income stream than a direct sale.

You also get an immediate partial income tax deduction in the year you fund the trust, often between 15% and 30% of the gift’s value.

The catch is plain enough:

- The trust is irrevocable

- You give up access to the principal

- The remainder goes to charity, not your heirs

- The charitable remainder must be at least 10% of the contributed value

Timing matters here. If the IRS decides the sale was prearranged, the trust can be ignored and the full tax bill can come back.

For owners trying to balance growth with legacy planning, these tools don’t have to sit in separate boxes.

Combining Strategies for a Better After-Tax Result

Many owners don’t use just one approach. Some move through a series of 1031 exchanges, then hold the last property until death so the estate gets the step-up in basis. The best mix comes down to one thing: what matters most right now – cash today, income later, or wealth transfer.

| Strategy | Primary Goal | Tax Impact | Key Trade-off |

|---|---|---|---|

| Step-Up in Basis | Legacy / Wealth Transfer | Eliminates gain and recapture at death | Must hold asset until death |

| CRT | Charity / Lifetime Income | Eliminates immediate capital gains tax | Irrevocable; heirs lose principal |

| 1031 Exchange to Step-Up | Growth + Wealth Transfer | Deferral during life; elimination at death | Requires ongoing reinvestment in real estate |

Bring in a CPA with experience in CRE sales 12 to 24 months before a planned sale so you can compare structures before any contract is signed.

How to Pick the Right Structure Before You Go to Market

After you review the main tax options, the next move is simple: pick the structure that lines up with your exit plan.

Match Your Strategy to Your Goal: Cash, Reinvestment, Passive Ownership, or Legacy

Start with one question: what do you want from the sale – cash at closing, money to reinvest, passive income, or a legacy play?

If your top goal is cash now, a taxable sale is usually the most direct route. The downside is obvious: you may face a big federal tax bill, plus depreciation recapture and state taxes. If your goal is something else, a different setup may fit better.

| Primary Goal | Likely Best Fit | Key Tradeoff |

|---|---|---|

| Maximum cash now | Taxable sale | Highest immediate tax bill |

| Reinvestment in real estate | 1031 exchange | Strict timing |

| Passive income, no management | DST | Illiquid; no operational control |

| Spread gain across years | Installment sale | Recapture due in Year 1 |

| Long-term growth | QOZ fund | Illiquid; project risk |

| Lifetime income + charitable intent | CRT | Irrevocable; principal eventually goes to charity |

| Wealth transfer to heirs | Hold until death (step-up in basis) | Must hold until death |

Once the goal is clear, the next issue is control. How much complexity can you live with? And how much control do you want to keep?

Single-Asset Owners vs. Larger Investors: Different Needs, Different Fits

Size matters here.

A Mom-and-Pop owner selling one facility often has less room to maneuver than someone selling a portfolio. Larger or multi-asset sellers can look at more structures and may have more capacity to deal with added paperwork, planning, and moving parts.

So the best fit is not just about the strategy on paper. It also comes down to your time, your capital, and how much planning bandwidth you have.

Timing, Contract, and Advisory Steps You Should Take Before Listing

Some of these structures have to be set up before the contract is signed or the deal closes. Miss that window, and the option may be gone.

Use this checklist:

- Engage a CRE-specialized CPA 12–24 months before listing to model tax scenarios and review your ownership entity

- If you are considering a CRT, fund it before any binding sale agreement exists

- For a 1031 exchange, have a Qualified Intermediary and exchange documents in place before closing

- Negotiate installment sale terms and write them into the contract before signing

- If you want a passive exit, identify DST sponsors before the 45-day identification clock starts

- A January closing can defer tax into the next year

The big point is timing. Many of the best tax moves depend on what you put in place before you list the property.

Conclusion: Plan Before the Sale to Keep More of the Proceeds

After looking at deferral, elimination, and legacy paths, the choice comes down to timing.

Key Takeaways for Owners Getting Ready to Sell

The biggest tax hit often comes from waiting too long. That’s the part that catches people off guard. Start with your numbers, because your adjusted basis drives both your gain and your recapture exposure.

Then match the tool to the goal. If you want real estate exposure, use a 1031 exchange. If you want passive ownership, use a DST inside that exchange. If you want cash over time, use an installment sale. If legacy planning is the goal, look at step-up in basis or a CRT. The step-up in basis at death is the main elimination path, while a CRT can eliminate immediate capital gains tax.

From there, timing decides whether the plan works at all. Most of these structures need to be set up before the purchase contract is signed. A CRT must be funded before any binding sale agreement exists. A 1031 exchange needs a Qualified Intermediary before closing. An installment sale must be written into the contract terms. Miss those windows, and that option may be off the table.

Bring in a CRE-specialized CPA 12–24 months before you list. That kind of pre-sale planning can increase your after-tax proceeds from a self-storage, boat, or RV sale.

FAQs

Which tax strategy fits my sale goals?

The right strategy comes down to what you want most: liquidity, control, or legacy. That choice shapes what happens to your proceeds after the deal closes. And as Nolen Masserman, Managing Director at Oakside, points out, planning before closing is what helps protect those proceeds.

A few common paths stand out:

- 1031 exchange: lets you defer taxes if you plan to remain in real estate

- DST: offers passive ownership and can satisfy 1031 rules

- Installment sale, Opportunity Zone funds, or Charitable Remainder Trusts: may fit owners who want income, growth, or tax elimination

Can I still defer taxes after signing a contract?

Usually, yes – but timing matters a lot.

You need to plan ahead because many tax-deferral moves have to be in place before closing.

For example, a 1031 exchange requires a Qualified Intermediary before closing. If you receive the sale proceeds directly, the exchange is disqualified. Once the sale is fully closed and you have constructive receipt of the funds, your tax-deferral options become much more limited.

How do I estimate capital gains and recapture before selling?

Estimate three parts of your tax bill before selling: capital gains, depreciation recapture, and the 3.8% NIIT.

Capital gain is the difference between your sale price and your adjusted cost basis. Long-term federal rates are usually 15% or 20%.

Depreciation recapture is taxed at 25% on the total depreciation taken.

The Net Investment Income Tax (NIIT) may apply if your income is above $200,000 for single filers or $250,000 for married couples filing jointly.

Ask your CPA to include state taxes too.