If you sell a self-storage or boat/RV property, your first job is simple: figure out what you keep, what you owe in taxes, and whether a 1031 deadline applies. In many cases, taxes can take 35% to 45% of your gain, and a 1031 exchange gives you only 45 days to identify a replacement property and 180 days to close.

Here’s the short version:

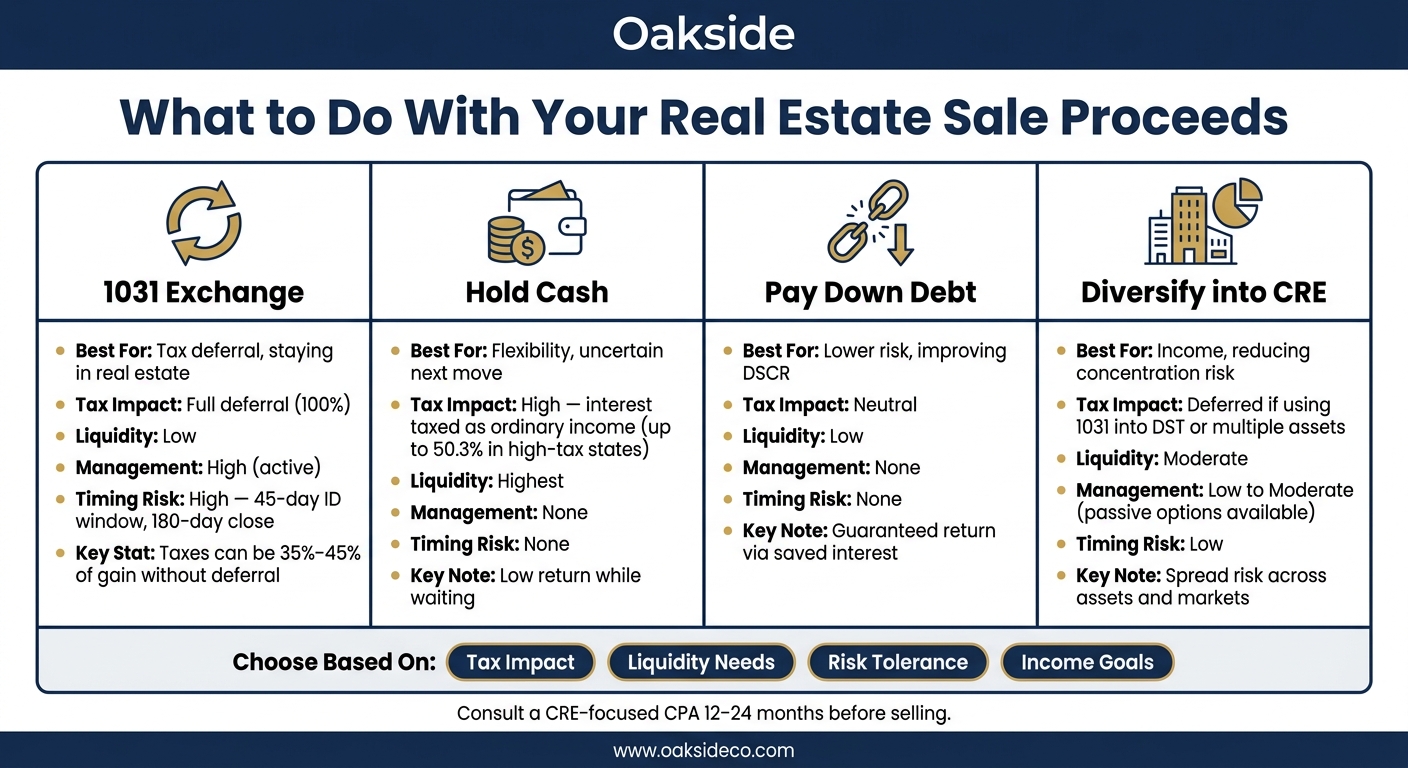

- Use a 1031 exchange if you want to defer taxes and stay in real estate.

- Hold cash if you need time and flexibility, but remember cash interest is taxable.

- Pay down debt if you want lower risk and a direct return from saved interest.

- Diversify into other CRE deals if you want income from real estate without keeping all your money in one asset.

Before you do anything, I’d focus on these three numbers:

- Net sale proceeds

- Estimated tax bill

- 1031 deadlines, if any

Quick comparison

| Option | Best for | Main upside | Main downside |

|---|---|---|---|

| 1031 exchange | Tax deferral | Keeps more equity invested | Tight timing and low flexibility |

| Hold cash | Flexibility | Easy access to funds | Low return and tax on interest |

| Pay down debt | Lower risk | Saves interest right away | Less liquidity |

| Diversify into CRE | Income and lower concentration | Spread risk across assets or markets | Less control in some setups |

The core idea is straightforward: don’t treat sale proceeds like idle cash. I’d make the next move based on tax impact, liquidity needs, risk tolerance, and income goals.

sbb-itb-09b4138

Understand your net proceeds, taxes, and timeline

Calculate what you actually keep after the sale

Before you pick a direction, figure out the actual dollars you’ll keep. The sale price alone doesn’t tell you much. What matters is your net proceeds: the amount left after the mortgage payoff, any prepayment penalty, deal costs like broker commissions, title, escrow, and legal fees, plus your estimated tax bill.

Your total tax bill may include a few parts:

| Tax Component | Rate | Notes |

|---|---|---|

| Federal Long-Term Capital Gains | 15%–20% | Typically applies to most sellers’ taxable gain |

| Depreciation Recapture | 25% (flat) | Applies to prior depreciation deductions |

| Net Investment Income Tax (NIIT) | 3.8% | May apply above $200,000 for single filers and $250,000 for joint filers |

| State Income Tax | Varies | Depends on your state |

That number becomes your starting point. Every option you’re weighing rests on it, so run those numbers first.

Know the 1031 exchange deadlines before closing

If a 1031 exchange is on your radar, set it up before closing. This is one of those areas where timing isn’t just important. It decides whether the exchange works at all.

To keep the exchange in place, a Qualified Intermediary (QI) must be hired to hold the proceeds. If the money goes to you directly, the exchange fails. In plain English: once closing happens the wrong way, there’s no easy do-over.

Set your decision criteria: preservation, income, or growth

Before you compare paths, get clear on the job you want this money to do.

Most sellers are aiming for one of three things:

- Preservation: keep capital intact and cut tax drag

- Income: improve cash flow with a better-performing asset

- Growth: move into a larger or higher-quality property

That lens helps you sort through the main choices, whether that means reinvesting, sitting in cash for a period, paying down debt, or spreading money across other assets.

Once your after-tax proceeds and timeline are clear, you can compare each path on the same basis.

Compare the main options for your money after a sale

What to Do With Real Estate Sale Proceeds: 4 Strategies Compared

Use your own priorities to sort these four paths: defer tax, cut risk, keep flexibility, or go after growth. Start with the option that lines up with what matters most right now, whether that’s tax deferral, risk reduction, or growth.

Reinvest through a 1031 exchange to defer taxes and stay in real estate

Choose a 1031 exchange when your top goal is tax deferral and you want to stay invested in real estate. A 1031 exchange lets you keep more capital in play by deferring the tax bill. But there’s a catch: you still have 45 days to identify a replacement property and 180 days to close. That clock limits what you can realistically buy, which is why it helps to have possible replacement assets lined up before your sale closes.

| Strategy | Tax Deferral | Liquidity | Management Burden | Timing Risk |

|---|---|---|---|---|

| Pay Tax & Keep Cash | None | Highest | None | None |

| 1031 Into One Property | Full (100%) | Low | High | High (45-day ID window) |

| 1031 Into Multiple Properties | Full (100%) | Low | Moderate | Low (professionally managed assets that are available quickly) |

If you don’t want all of your capital tied up, the next options give you more room to move, but usually at the cost of return.

Pay down debt or hold cash to reduce risk and keep options open

If preserving capital matters more than return, these are the two simplest moves. Paying down debt cuts leverage. Holding cash keeps your options open.

Paying down debt can make sense if you have high-interest loans on other properties or want to improve your Debt Service Coverage Ratio (DSCR). The upside is simple: you save interest right away, and there’s little to no market risk attached to that move.

Holding cash gives you the ability to act when the right deal shows up or when market conditions change. The downside is the drag on returns. Interest earned on cash reserves is taxed as ordinary income, potentially at rates as high as 50.3% combined in high-tax states, which can eat into what you earn while you wait.

| Pay Down Debt | Hold Cash | Reinvest Now | |

|---|---|---|---|

| Liquidity | Low | Highest | Moderate |

| Risk | Very Low | Low (inflation risk) | Market dependent |

| Tax Impact | Neutral | High (tax on interest) | Deferred (if 1031) |

| Expected Return | Guaranteed (saved interest) | Low | Variable |

Diversify or recapitalize into larger commercial real estate opportunities

If you want to stay in real estate without staying heavily concentrated in one asset, this is the middle path. Reinvesting proceeds from a self-storage or boat/RV sale into multiple assets, different U.S. markets, or a larger professionally managed acquisition can lower concentration risk and shift you into real estate with steadier income and less day-to-day work.

Put simply, instead of betting on one property, you spread exposure across several assets, markets, or a larger managed deal. That can reduce dependence on the performance of any single property.

| Single Replacement Asset | Multi-Asset Diversification | Larger, Professionally Managed Acquisition | |

|---|---|---|---|

| Scale | 1:1 | Portfolio | Institutional |

| Concentration Risk | High | Low | Low |

| Management Intensity | High (active) | Moderate (passive/DST) | Low (professional) |

| Income Stability | Moderate | High | Highest |

Match each strategy to your goals, risk tolerance, and time horizon

Pick the move that lines up with your goal, risk tolerance, and hold period. Once your sale proceeds, tax exposure, and deadlines are clear, you can match each strategy to the outcome you want from the money.

Which path fits income-focused, tax-sensitive, and growth-oriented owners

Use the profiles below to narrow the choice fast.

| Owner Profile | Primary Goal | Best-Fit Strategy | Time Horizon | Management |

|---|---|---|---|---|

| Near retirement, income-focused | Reliable income, lower stress | DST or diversified 1031 into passive real estate | Medium to long (5–15 years) | Passive |

| Tax-sensitive, wants to stay in real estate | Defer taxes, preserve equity | 1031 exchange (direct or DST) | Long (7+ years) | Active or passive |

| Growth-oriented, high risk tolerance | Scale portfolio, compound wealth | Direct 1031 exchange or recapitalization into a larger acquisition | Long (7+ years) | Active |

| Needs flexibility, uncertain next move | Liquidity, optionality | Hold cash, short-term Treasuries, or money market funds | Short (<1 year) | Passive |

| Recapitalize or diversify | Reduce concentration, improve income stability | Diversify into multiple assets or a larger professionally managed acquisition | Long (7+ years) | Passive |

If passive ownership is your top priority, take a closer look at the DST row. For owners who want a hands-off setup, a Delaware Statutory Trust (DST) can offer 1031 eligibility and distributions without day-to-day management.

Why tax planning should be part of the decision from day one

After you know which strategy fits, tax planning shapes how much capital you can actually put to work. Start before closing, not after. Capital gains, depreciation recapture, NIIT, and state tax can cut into your net proceeds more than many owners expect.

Bring in a CRE-focused CPA 12–24 months before you sell, not when you’re already under contract. Put simply: tax planning done early gives you more room to act.

Conclusion: Choose your next move with a clear post-sale plan

Selling a self-storage or boat/RV property puts real money in motion. What you do next shapes how much of that capital stays in play. It starts with the math.

Begin with your true net proceeds: sale price minus debt payoff, commissions, closing costs, and estimated taxes.

Once those numbers are on the table, the next step is pretty simple. Decide what you want the money to do. Then line up your choice with your goal, risk tolerance, and time horizon. The best path depends on what matters most to you: tax deferral, liquidity, or growth.

Key takeaways for sellers after closing

After you choose a path, execution is all about timing and discipline.

- Calculate true net proceeds first.

- Respect 1031 deadlines if you use them – the 45-day identification and 180-day closing windows are non-negotiable.

- Choose liquidity, tax deferral, or reinvestment based on your goal.

Bring in a CRE-specialized CPA, tax attorney, and fiduciary wealth advisor before you need them – ideally 12–24 months before listing.

For owners getting ready to sell or handling proceeds after closing, Oakside helps evaluate the next move with transaction-focused analysis. A clear plan before and after closing helps protect your tax position and keep your options open. The right post-sale plan turns a closing into the next step.

FAQs

How do I estimate my after-tax sale proceeds?

Estimate your after-tax proceeds by factoring in federal capital gains, depreciation recapture, and any state taxes. Start with your adjusted cost basis. That’s your sale price minus your original investment, then adjusted for the depreciation claimed over the years.

You may owe 25% on recaptured depreciation, along with federal capital gains tax and, in some cases, the 3.8% Net Investment Income Tax. The details can shift if your deal includes an asset sale, seller financing, or an earn-out, so it’s smart to review the numbers with your CPA before you lock in your plan.

When does a 1031 exchange make more sense than holding cash?

A 1031 exchange often makes more sense when you want to roll your proceeds into a larger property or one in a better location. The big draw is tax deferral: it can postpone capital gains tax and depreciation recapture, which can leave more money available for your next deal. That matters even more if you live in a high-tax state, where the tax hit can sting.

Holding cash may be the better move if your goals have changed. Maybe you’re ready to retire, want more liquidity, or simply don’t want the hassle of managing property anymore. It can also be the safer path if you don’t want to deal with the strict deadlines that come with identifying and closing on a replacement property in a 1031 exchange.

How should I choose between paying down debt and reinvesting?

Choose based on your own priorities and the trade-offs you can live with.

If keeping cash on hand and cutting monthly obligations matter most, paying down debt can lower risk and free up cash flow. On the other hand, if your main goal is growth or income and you’re fine staying invested, reinvesting may be the better fit.

Before you decide, look at the full picture: your timeline, other income sources, state taxes, and your tax plan, including capital gains and depreciation recapture.