If you own self-storage or boat/RV property, one late move can turn a tax-saving gift into a taxable sale. As of July 2, 2026, the federal estate tax exemption is about $15 million per person and $30 million per married couple, with a 40% tax on the amount above that. For owners with high-value, low-cash real estate, that can create pressure fast.

Here’s the short version: I’d first map each facility, its debt, ownership entity, tax basis, and likely exit path. Then I’d match the gift tool to the goal:

- Direct bequest if I want to keep control for life and leave part of the estate to charity at death

- CRT if I want to transfer property before a sale, delay capital gains, and keep an income stream

- CLT if I want charity paid first and heirs to receive the asset later with lower transfer-tax cost

- DAF if I want an upfront income-tax deduction and grant money to charities over time

- Direct gift of real estate or LLC interests if I want to remove an appreciated asset from my estate and avoid capital gains on the donated piece

A few rules shape almost every decision:

- Timing matters: the gift usually needs to happen before a binding sale agreement is signed

- Debt matters: mortgages can trigger bargain-sale tax treatment

- Paperwork matters: non-cash gifts over $5,000 usually need a qualified appraisal and IRS Form 8283

- Basis matters: a step-up at death may beat a lifetime gift in some cases

- Entity structure matters: property held in an LLC or partnership is often easier to transfer than property held outright

Quick Comparison

| Option | Best use | Main tax angle | Main watchout |

|---|---|---|---|

| Direct bequest | Gift at death | Estate tax deduction | No lifetime income-tax deduction |

| CRT | Pre-sale planning + income | Delay capital gains; income stream | Must be set up before sale talks harden |

| CLT | Passing wealth to heirs | Gift/estate tax planning | Trust design can be complex |

| DAF | Deduction now, grants later | Income-tax deduction; capital gains avoided on donated asset | Sponsor approval for illiquid assets |

| Direct gift | Donate property or entity interest now | FMV deduction and estate reduction | Debt, appraisal, and filing rules |

Bottom line: I’d treat charitable planning as part of the exit plan, not an afterthought. The article shows how to line up the right vehicle, the right timing, and the right advisors so family goals, tax rules, and charitable goals don’t work against each other.

sbb-itb-09b4138

Estate Planning Basics to Establish Before Choosing a Charitable Strategy

Before you choose a CRT, DAF, or CLT, get a clear read on each asset’s ownership, debt, and tax basis. In plain English, that means building a clean inventory first.

Take Stock of Assets, Ownership Structures, and Liabilities

List every storage facility, land parcel, and equipment holding. Then note how each asset is owned: personally, inside an LLC, or through a family limited partnership (FLP). That detail matters because the structure affects control, how easy it is to gift interests, and whether valuation discounts may apply.

Debt needs a close look too. It can trigger bargain sale treatment, so review every mortgage, lien, and guarantee before making a gift. You should also document the original cost basis and current fair market value for each facility. That helps you estimate capital gains exposure and see how much a step-up in basis at death could matter. Review Section 1250 recapture before any gift.

This inventory shows which charitable tools are even on the table.

Decide Each Facility’s Exit: Family, Sale, or Recapitalization

Next, decide what happens to each facility. Will it stay in the family, be sold, or be recapitalized?

If heirs aren’t likely to operate the facility, a sale or recapitalization may make more sense. One example is a rollover into a Delaware Statutory Trust. That family-sale-recapitalization call shapes which charitable strategies fit and which ones don’t.

It also sets the tax rules and timing that come next.

Key Tax Rules That Shape the Plan

Three tax rules drive most charitable planning choices for storage owners.

Step-up in basis can erase built-in gain at death. Heirs inherit the facility at current fair market value, which can change whether a lifetime gift or a bequest makes more sense. Estate-tax exposure grows when you hold multiple appreciated facilities, because each one adds to the taxable estate above the exemption threshold. Current itemized charitable deductions face a 0.5% AGI floor and a 35% benefit cap for high-income taxpayers.

With those facts in place, the next move is matching the ownership setup to the charitable strategy.

Ownership structure affects control, gifting ease, valuation discounts, and liability:

| Ownership Structure | Control | Valuation Discount Potential | Ease of Gifting Interests | Liability Considerations |

|---|---|---|---|---|

| Personal Ownership | Full | None | Difficult (requires deeding) | High – personal assets exposed |

| LLC | High | Moderate | Easier (transfer of membership units) | Good – assets shielded by the corporate veil |

| Family Limited Partnership (FLP) | General partner retains control | High – potential lack of control/marketability discounts | Excellent for multi-generational gifting | Good – limited partners have protected liability |

| Revocable Living Trust | Full (as trustee) | None | Moderate | None – not a liability shield |

Charitable Giving Strategies That Work With Storage Estates

Once ownership and the exit path are clear, the next step is matching the charitable tool to the tax result you want. Each option comes with its own tax treatment, control tradeoffs, and paperwork. The best fit depends on whether the gift is part of a sale, a family transfer, or a legacy plan.

Direct Bequests and Beneficiary Designations

Leaving assets to charity through your will, revocable trust, or a beneficiary designation on a retirement account like an IRA or 401(k) can produce a 100% estate tax charitable deduction for the amount that goes to charity, with no lifetime deduction needed.

If control during your lifetime matters more than keeping things simple at death, trust-based tools may be a better fit.

CRTs, CLTs, and Donor-Advised Funds

A Charitable Remainder Trust (CRT) can work well for owners who want to sell a facility, swap operating income for passive income, and defer capital gains. The property needs to be transferred into the trust before any binding sale agreement or letter of intent (LOI) is signed. The trust then sells the asset, and the proceeds remain inside the trust for reinvestment. You receive income for life or for a set term, and whatever is left goes to charity.

A Charitable Lead Trust (CLT) flips that setup. The charity gets income for a set term, and the remaining assets pass to your heirs, often with a lower gift or estate tax cost. This can make sense for owners who want to move a high-growth facility to the next generation while still supporting a cause along the way.

A Donor-Advised Fund (DAF) can accept cash and, when the sponsor allows it, appreciated real estate or LLC interests. You get an immediate deduction at fair market value, then recommend grants to charities over time. DAFs can be a good middle ground if you want less admin than a private foundation. They can also take more complex assets, such as partnership interests, but it’s smart to confirm the sponsor’s due diligence rules before contributing illiquid property.

If the asset itself is ready to be transferred, a direct gift may make more sense.

Direct Gifts of Real Estate or Entity Interests

You can donate a storage facility – or an interest in the LLC or partnership that owns it – straight to a public charity. This tends to work best when the facility sits inside an LLC or partnership that can be transferred without a mess. If handled the right way, the gift avoids capital gains tax on the appreciation and gives you a deduction based on fair market value, not your original cost basis.

A few compliance rules are strict:

- Any non-cash gift over $5,000 needs a qualified appraisal dated no more than 60 days before the contribution date.

- You’ll also need to file IRS Form 8283.

Debt is the biggest wrinkle. If the property has a mortgage, the debt relief can trigger taxable gain under bargain-sale rules, even if no cash changes hands. That means debt and timing often drive the plan. They can decide whether the gift should happen before a sale, a recapitalization, or a transfer to heirs.

Coordinating Charitable Planning With Sales, Succession, and Execution

Charitable Estate Planning Roadmap for Storage Property Owners

Once you’ve picked the right charitable vehicle, the hard part shifts to timing and coordination.

Using Charitable Planning Before a Sale or Recapitalization

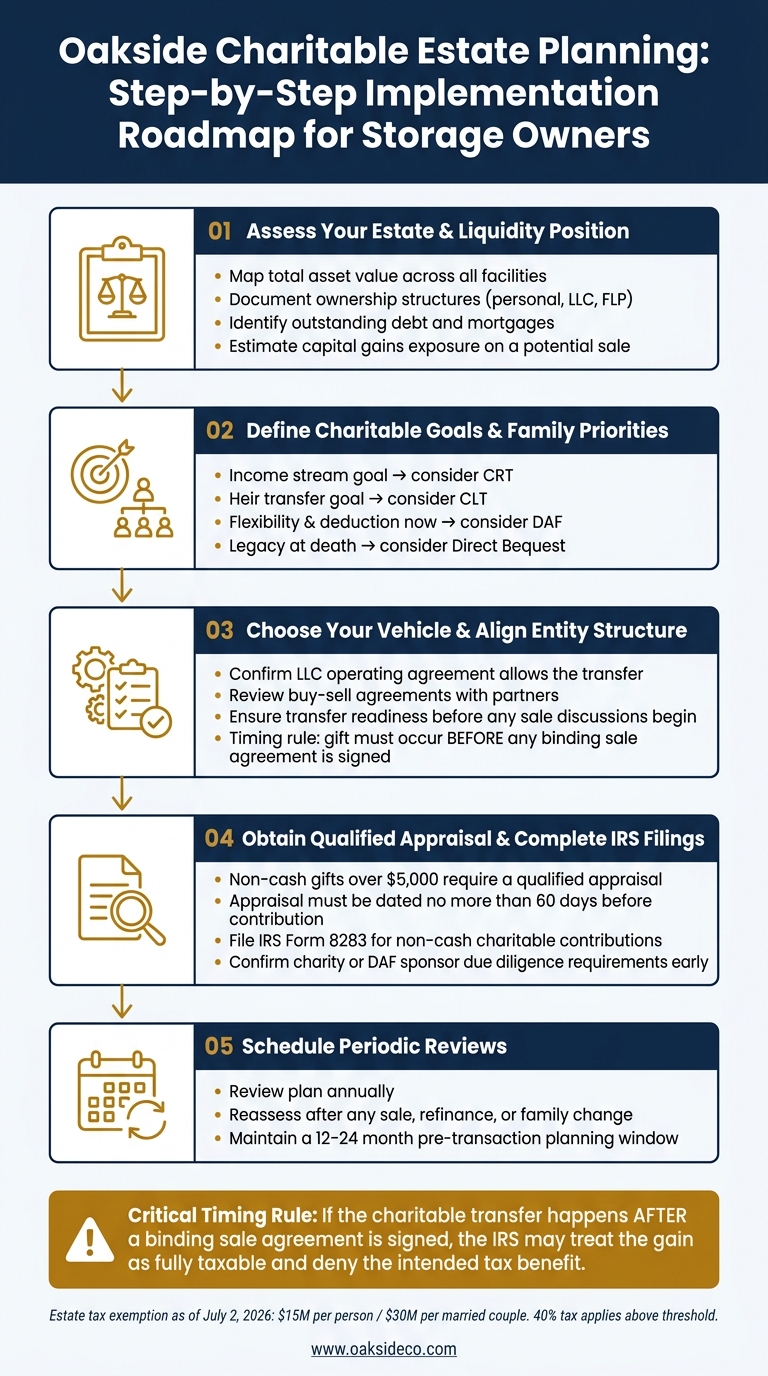

Timing drives tax treatment. The key rule is simple: transfers to a charitable vehicle must happen before any binding sale agreement is signed. If the transfer happens too late, the IRS may treat the gain as taxable. In a recapitalization or partial-interest sale, that means the transfer has to happen before the deal is signed, not after the structure is already in place.

That point matters more than it may seem. If the timing is off, you don’t just lose a deduction. You can also derail the charitable and family outcomes the plan was meant to support.

At that stage, the work moves from tax design to deal execution.

Building the Right Advisory Team and Governance Process

The next danger is execution. One missed signature, transfer, or filing can wipe out the tax result.

Charitable estate planning for storage assets isn’t a one-person assignment. It takes close coordination between:

- an estate planning attorney

- a CPA or tax advisor

- a commercial real estate advisor who knows the depreciation and valuation issues tied to self-storage and boat/RV properties

Each advisor has a different job. The attorney drafts trust documents and updates ownership structures. The CPA models tax outcomes and flags depreciation recapture exposure. The real estate advisor helps make sure transaction timing, asset valuation, and deal structure match the charitable plan before anything is listed or marketed.

A Step-by-Step Implementation Roadmap

Use this sequence to keep the gift lined up with the transaction. These steps move a chosen vehicle from plan to completed transfer.

- Assess your estate and liquidity position: Know your estate-tax exposure before choosing a tool. Map total asset value, ownership structures, outstanding debt, and estimated gain on a sale.

- Define your charitable goals and family priorities: Match the vehicle to the goal, whether that’s income, heir transfer, or deduction timing.

- Choose your vehicle, then align your entity structure: Once the vehicle is selected, confirm that your LLC operating agreement and any buy-sell agreements with partners don’t block the transfer. Keep this step centered on transfer readiness, not broad structuring.

- Obtain a qualified appraisal and complete IRS filings: This is a compliance checkpoint. Secure a qualified appraisal and file IRS Form 8283. If the charity or DAF sponsor is receiving real estate or a partnership interest, confirm their due diligence process early.

- Schedule periodic reviews: Review the plan each year and after any sale, refinance, or family change.

Conclusion: Choosing a Charitable Estate Plan That Protects Value and Defines Legacy

Start with the goal: a family transfer, a sale, or a mix of both. Then pick the charitable tool that matches that path. After you compare the main options, the next move is to line up the tool with your ownership structure and exit plan.

For storage owners with illiquid, appreciated operating real estate, the tax hit can be steep. Estate tax, capital gains, and depreciation recapture can wipe out a big chunk of value if you don’t plan ahead. That’s why early planning isn’t just nice to have. It’s expensive to put off.

Use a CRT when income is the main aim. Use a CLT when the focus is moving wealth to heirs. Use a DAF when you want flexibility and an immediate deduction. After the vehicle is set, timing becomes the thing that matters most. Put the gift in place before a sale agreement is signed. If the transfer happens too late, the IRS may treat it as part of a pre-arranged sale and deny the intended tax result.

That 12-to-24-month pre-transaction window matters. It’s the time to get appraisals, line up entity documents, and confirm the gift structure. When the plan is documented well and timed the right way, it can do more than cut taxes. It can shape what heirs receive and what charities can do with the gift.

For storage owners, a well-timed charitable plan can reduce taxes and make succession easier. It can protect value and define what you leave behind.

FAQs

When should I start charitable estate planning?

Start early and review your plan on a regular basis. If you wait too long, your options can shrink, and many tax moves won’t work as well.

For self-storage owners, this matters even more if a sale may be coming. Plan well before listing the property, because most charitable tax benefits are lost once the deal closes. Early coordination with tax and legal advisors helps line up your giving goals with your exit strategy.

How does debt affect a charitable real estate gift?

Debt can make a charitable real estate gift much more complicated. Under the bargain sale rules in IRC Section 1011(b), if a charity takes on a mortgage, the IRS treats that debt relief as an amount realized by the donor.

In plain English: even if no cash changes hands, the IRS may still treat part of the deal like a sale.

That means you have to split your basis between the gift portion and the sale portion. And that split can trigger a taxable capital gain, even when you don’t receive any money at closing.

As Nolen Masserman, Managing Director at Oakside, emphasizes, modeling these tax effects is a must.

Should I donate the property now or leave it at death?

It depends on your financial goals and your tax situation.

If you donate during your lifetime, you may avoid capital gains tax on appreciated assets. You may also be able to claim a deduction based on the asset’s fair market value. That can be a big help in high-income years, when tax planning matters most.

If you keep the asset until death, your heirs may receive a stepped-up cost basis. In plain English, that can wipe out deferred tax liabilities tied to the asset.

As Oakside notes, early planning can help align charitable goals with broader wealth-planning objectives.