Self-storage prices now move in large part because institutional money is in the market. I’d boil it down like this: more large buyers mean tighter cap rates on top assets, more focus on stabilized NOI, and more separation between sale-ready properties and weaker ones.

If you own a facility, here’s what matters most:

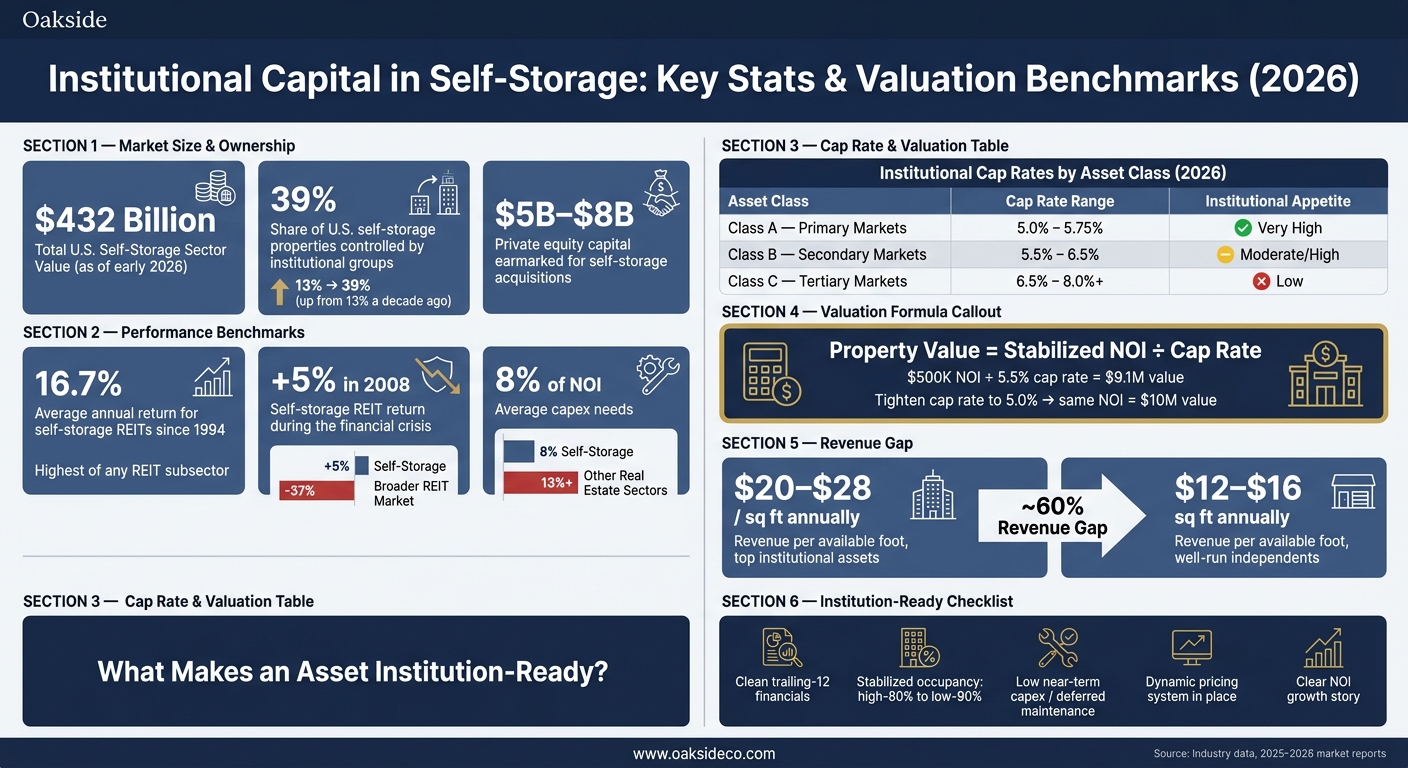

- Institutional groups now control about 39% of U.S. self-storage properties, up from 13% ten years ago.

- The sector is worth about $432 billion as of early 2026.

- Many buyers price deals with one formula: Value = Stabilized NOI ÷ Cap Rate.

- In 2025–2026, national cap rates settled near 5.8% after moving up from the lows of 2021–2022.

- Today, most value growth comes from better NOI, not lower cap rates.

- Assets with clean financials, low near-term repair costs, strong occupancy, and better pricing systems tend to draw the most buyer interest.

Here’s the short answer: I see institutional capital changing value, liquidity, and timing. It can support pricing for stronger assets, but it also makes buyers more selective. That means your property does not just need income. It needs a clean story that a large buyer can underwrite fast.

A quick look at how this plays out:

| Topic | What I’d watch |

|---|---|

| Pricing | Cap rates, stabilized NOI, revenue per square foot |

| Buyer demand | Class A assets, supply-tight markets, assets with upside |

| Deal pressure | Higher borrowing costs, stricter debt tests, repair deductions |

| Sale prep | Trailing 12-month reports, occupancy, deferred maintenance, pricing tools |

So if I were planning a sale or refinance, I’d focus less on market hype and more on the basics that move price: income quality, property condition, and buyer fit.

Institutional Capital in Self-Storage: Key Stats & Valuation Benchmarks 2026

Institutional Capital in Self-Storage: What It Is and Why It Matters

What Institutional Capital Means in Self-Storage

Institutional capital refers to large, professional investors that care about scale, reporting, and strict underwriting. In self-storage, that usually means public REITs, private equity funds, pension funds, insurance companies, sovereign wealth funds, and large private investment groups.

These buyers play on a very different field than local owner-operators. They lean on centralized pricing, marketing, and customer service systems to run properties more efficiently. Public Storage now handles 85% of customer interactions digitally, which cuts down on on-site labor needs.

That edge shows up in the numbers. Institutional operators usually produce 10%–20% higher revenue per square foot than independent owners.

And that matters for more than just the properties they own. When large buyers can earn more from the same asset, they can often justify paying more for it. That can push pricing across the market, even for facilities they never touch.

How Large the Institutional Footprint Is in the U.S. Market

The institutional presence is already big, and it keeps growing. The top four REITs alone control about 30% of total U.S. inventory. Independent owners still hold about 70% of facilities, but that share is getting smaller.

There is also an estimated $5 billion to $8 billion in private equity capital now set aside just for self-storage acquisitions.

Once that much money starts chasing the same asset class, the effect spreads beyond a handful of deals. It shapes how buyers model value across the sector, from cap rates to income targets to final pricing. This often requires a detailed sensitivity analysis to account for shifting market variables.

Why Self-Storage Has Attracted Institutional Capital

Self-storage checks a lot of boxes for large investors. For one, capital expenditure needs are relatively low. They average just 8% of NOI, compared with 13% or more for most other real estate sectors. Put simply, more of the income can stay as income.

The sector has also shown unusual strength during rough periods. During the 2008 financial crisis, self-storage REITs were the only real estate sector to post positive returns, at +5%, while the broader REIT market fell -37%.

Long-term returns help tell the same story. Since 1994, self-storage REITs have posted an average annual return of 16.7%, the highest of any REIT subsector over that span.

Add in fragmented ownership and clear room for better operations, and it becomes easier to see why institutional money keeps flowing in. For owners, this helps explain who the buyers are, how they look at deals, and what they want to see in performance.

That mix of scale and operating discipline also helps explain why institutional capital has such a strong effect on cap rates, NOI expectations, and transaction pricing.

sbb-itb-09b4138

How Institutional Capital Shapes Valuations and Market Capitalization

How Cap Rates, NOI, and Value Connect in Self-Storage Underwriting

When institutional capital shows up in a deal, pricing usually comes down to one simple math problem: Value = Stabilized NOI ÷ Cap Rate.

Here’s what that looks like in plain English. If a facility produces $500,000 in stabilized NOI and trades at a 5.5% cap rate, its value lands at about $9.1 million. If the cap rate tightens to 5.0%, that same property is worth $10 million. Same income. Different pricing multiple.

That’s why cap rates matter so much.

Institutional buyers usually underwrite to stabilized NOI, not just the cash flow a property happens to show today. In other words, they focus on the income the asset should produce once it reaches steady occupancy and runs as expected. That approach tends to shape how they price deals in every part of the market cycle.

How Institutional Inflows Affect Pricing Across Market Cycles

Institutional demand pushed self-storage cap rates lower in 2021 and 2022. After that, higher interest rates changed the tone. Buyers became more selective, and cap rates widened by about 80 to 100 basis points from those lows before leveling off at roughly 5.8% nationally in 2025–2026.

Pricing per square foot moved the same way. Average values fell 12%, sliding from a peak of $174 in Q1 2023 to about $159 by Q2 2025.

One of the biggest pressure points today is leverage. Borrowing costs of 5.0% to 6.5% often meet or beat day-one cap rates. That can make deals harder to pencil for private buyers. Institutional groups still have an edge because many use corporate-level debt instead of property-level financing. Public Storage, for example, carries debt at about 3.2%, which sits far below many private-market borrowing costs.

The table below shows how institutions are pricing each asset type in 2026:

| Asset Profile | Typical Cap Rate Range | Institutional Appetite |

|---|---|---|

| Class A (Primary Market) | 5.0% – 5.75% | Very High |

| Class B (Secondary Market) | 5.5% – 6.5% | Moderate/High |

| Class C (Tertiary Market) | 6.5% – 8.0%+ | Low |

For owners thinking about a sale right now, that matters. In 2026, most value growth comes from improving NOI, not from cap rates falling further.

Single-Asset Values vs. Sector Market Capitalization: Key Differences

A single facility sale and the sector’s total market capitalization are related, but they are not the same thing.

An individual sale price depends on local conditions: supply, the property’s NOI, and what a buyer thinks they can improve after closing. Sector market capitalization works at a much bigger scale. It reflects the estimated value of all U.S. self-storage assets, which reached about $432 billion by February 2026.

That sector-wide figure is shaped by public REIT pricing, portfolio trades, and forward NOI expectations across the industry. Big portfolio deals can also reset the market’s view of pricing for scale and institution-grade assets. One example is Public Storage’s March 2026 acquisition of National Storage Affiliates, which helped reset pricing expectations for larger, institution-quality portfolios.

For owners, the message is pretty direct: institutional capital tends to support stronger pricing for assets that fit institutional standards, while properties that fall short can see discounts happen much faster.

How Institutional Capital Changes Investment Strategy and Deal Structure

Institutional capital does more than push prices up. It also shrinks the pool of assets and deal setups that can pass underwriting.

What Asset Types Institutional Buyers Are Targeting Today

Institutional buyers are zeroed in on asset profiles that fit their return targets and risk limits. Stabilized Class A facilities in high-barrier markets like Boston, New York City, and Los Angeles are still at the top of the list. These markets have limited new supply and strong pricing power, which helps support steady cash flow.

They also look for assets with clear operational upside that can justify a higher basis. But there’s a catch: buyers only pay up for that upside when it has a direct, believable path to higher NOI.

Self-storage vs. RV storage assets are getting more attention too, especially in markets with active housing turnover and strong recreational demand. If you own one of these assets, that shift in buyer demand matters.

That same focus on operations shapes how buyers think about leverage, hold period, and value-creation assumptions.

How Underwriting Standards and Hold Strategies Have Evolved

Institutional buyers are taking a harder look at supply pipelines, occupancy staying power, and rent growth assumptions than they did a few years ago. That discipline helps protect basis at a time when cap rates do not have much room left to compress. With new deliveries projected at just 2.4% of total stock in 2026 and dropping below 2% by 2027, supply-constrained markets are drawing the most attention.

Underwriting is tighter across the board. Many institutional buyers are still modeling at least 1.3x DSCR and projecting 9%–14% revenue gains from dynamic pricing.

Expense control matters just as much as top-line growth. Buyers are underwriting deferred maintenance into the deal from day one, so issues with roofs, paving, or HVAC will drag on price because those costs get baked in upfront.

How Owners Can Align Transaction Strategy With Institutional Requirements

Once an asset clears the buyer’s screen, presentation becomes the next lever on price.

The first thing buyers want is clean trailing-12 financials. Institutional groups expect trailing 12-month reports that are consistent and backed by industry-standard software, not manual spreadsheets. Clear NOI support is the backbone of a sale process buyers can trust.

The story around the asset matters too. Buyers want to see room for growth, proof that revenue management is already in place, and a property that does not come with immediate capex needs. Even putting dynamic pricing in place before a sale can lift revenue per available foot by 5%–15%, and that increase flows straight into value at a 5.5% cap rate.

Risks, Benefits, and Practical Positioning for Institutional Capital

What Owners Gain and What Can Become More Challenging

As institutional buyers take up more of the buyer pool, operational readiness starts to show up in pricing in a very direct way.

For sellers with strong assets, that can be a good thing. Institutional demand can help support pricing and keep deals moving, especially for quality properties. But there’s another side to it. The same scale that helps support prices also pushes up expectations for operations, reporting, and tech.

Institutional operators often run with AI-driven pricing, stronger marketing, and tighter systems than many smaller owners can match. AI pricing can increase revenue by 5%–10%, while scale can cut costs for insurance, taxes, and vendors. That edge doesn’t just improve day-to-day performance. It also creates a bigger valuation gap between assets that are ready for institutional buyers and those that aren’t.

| Category | Advantages | Tradeoffs |

|---|---|---|

| Pricing | Premiums for assets with clear upside | Wider valuation spread between stronger and weaker assets |

| Liquidity | Institutional demand can support pricing and transaction volume | Sellers need cleaner financials and a clearer operating story |

| Operating | Scale and AI pricing improve performance | Smaller owners face a growing technology gap and tougher competition |

What Makes a Self-Storage Asset Institution-Ready

That gap helps explain why buyers look first at occupancy, reporting, and near-term capex.

Institutional buyers tend to favor stabilized occupancy in the high-80% to low-90% range. In late 2025, REIT portfolios were sitting in the low-90% range, about 8 to 12 points above smaller private operators. Buyers also want clean, steady reporting with clear NOI support. If the numbers are messy, the story gets harder to sell.

Physical condition matters just as much as the operating story. Assets with limited near-term capex needs and rent levels that hold up under review are easier to underwrite. Revenue per available foot is another big marker. Top institutional assets bring in about $20 to $28 annually, while well-run independents tend to land around $12 to $16. If an owner can narrow that gap before going to market, pricing can improve.

Conclusion: What Institutional Capital Means for Pricing, Liquidity, and Timing

Institutional capital is making the spread wider between institution-ready assets and the rest of the market. That puts more weight on preparation and timing when an owner is thinking about an exit. Owners who deal with deferred maintenance, tighten up reporting, and update pricing systems are in a better spot to attract institutional demand and hold the line on price when buyers get more selective.

For owners, the practical question is not whether institutional capital matters. It’s whether the asset is set up to benefit from it.

FAQs

How do institutions affect self-storage values?

Institutional capital is pushing self-storage values up. The main reason is simple: more competition for properties tends to lift prices. And that shift has been meaningful. Institutions now control about 30% of inventory, up from 17% two decades ago.

They also have room to pay more and still make the numbers work. Why? Their operating scale often leads to 10%–20% higher revenue per square foot. That extra income can change the math in a big way.

Add in favorable financing and steady consolidation, and you get a market where property values, occupancy, and rent growth all have support.

What makes a facility institution-ready?

An institution-ready self-storage facility blends modern tech with disciplined day-to-day execution. The core pieces usually include dynamic pricing, AI-powered revenue management, smart access, and online rentals. Together, those features can improve revenue, tighten efficiency, and make the customer experience much smoother.

Scale matters too. Larger operators often benefit from lower operating costs and stronger lead conversion, which can have a direct effect on performance. Facilities in supply-constrained markets tend to stand out even more when they pair that location advantage with modern amenities and well-run operations.

For institutional investors, that mix can be hard to ignore: a facility that looks modern, runs cleanly, and turns interest into signed rentals without a lot of friction.

Should owners sell now or improve NOI first?

Owners need to make a clear choice.

They can sell now and take advantage of strong buyer demand and favorable market conditions. Or they can hold the property longer and put money into NOI improvements through modernization and operational changes.

That second path can pay off, but timing matters. Wait too long, and the property’s future value may slip.