A self-storage lease can shape occupancy, pricing, collections, fees, and sale value all at once. In most U.S. facilities, the big choices come down to month-to-month, fixed-term, or hybrid leases, plus the fine print on pricing strategies, lien rights, default, abandonment, insurance, and vehicle storage rules.

If I were reviewing a facility today, I’d focus on these points first:

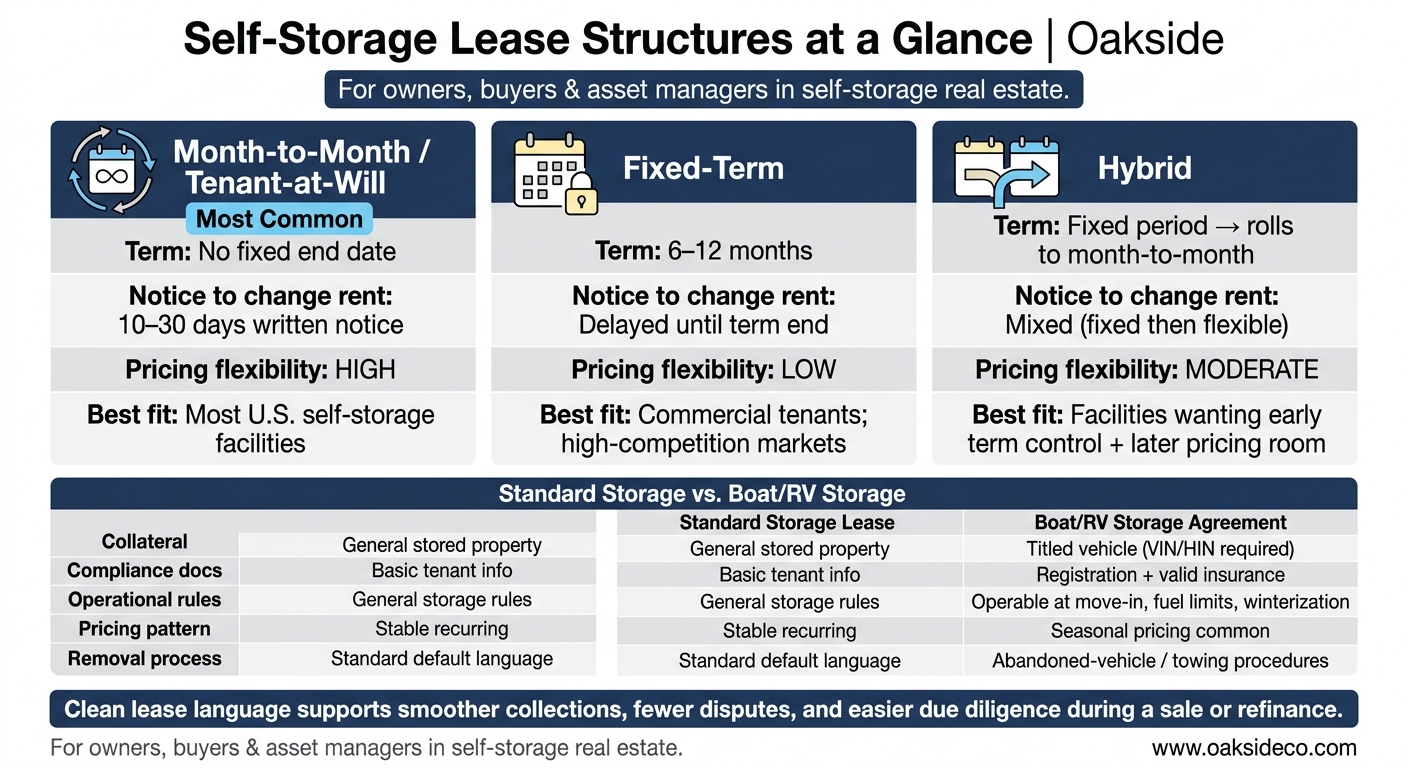

- Month-to-month leases give owners more room to change rent, often with 10 to 30 days’ notice

- Fixed-term leases usually run 6 to 12 months and can hold tenants longer, but pricing changes may have to wait

- Hybrid leases start with a set term, then switch to month-to-month

- Lien, default, and abandonment clauses affect how unpaid rent is handled

- Fees and insurance terms affect income and claim risk

- Boat and RV leases need extra terms for VIN/HIN, registration, insurance, towing, and seasonal use

For buyers, owners, and asset managers, the short version is simple: clean lease language can support smoother collections, fewer disputes, and a tighter review process during a sale or refinance. This is a critical step in self-storage exit planning to maximize property value.

Quick Comparison

| Lease Type | Term | Pricing Changes | Best Fit |

|---|---|---|---|

| Month-to-month | No fixed end date | Faster, based on notice rules | Most self-storage facilities |

| Fixed-term | 6–12 months | Often delayed until term end | Commercial users or tougher markets |

| Hybrid | Starts fixed, then rolls monthly | Mixed | Facilities that want both early term control and later pricing room |

There’s also a second split that matters: standard unit leases vs. boat/RV agreements. Standard leases deal with stored goods. Boat and RV agreements deal with titled vehicles, which means more rules, more paperwork, and more default steps.

That’s the core of the article: the lease type sets the basic structure, but the money and risk often come from the clauses behind it.

sbb-itb-09b4138

Core lease structures used in self-storage properties

Self-Storage Lease Types Compared: Month-to-Month vs Fixed-Term vs Hybrid

Month-to-month rental agreements and tenant-at-will occupancy

Month-to-month rental agreements are the standard setup in self-storage. They renew on their own and usually let either side end the agreement with 10 to 30 days’ notice. That makes them simple to run and easy for tenants to understand.

In self-storage, tenant-at-will language refers to occupancy rights, not residential tenancy. That distinction matters. It gives owners more room to adjust rates as demand shifts, instead of waiting months for a lease to expire.

Fixed-term and hybrid storage leases

Fixed-term leases, usually 6 to 12 months, show up most often with commercial users or in high-competition markets. They can help steady occupancy, but there’s a tradeoff: owners usually can’t reprice until the term ends.

Hybrid leases sit in the middle. They begin with a fixed term and then roll into a month-to-month arrangement. So you get some term stability up front, then more pricing and occupancy flexibility later.

Comparison of common lease structures

The table below shows how each structure balances occupancy control, pricing speed, and term length. Owners, buyers, and asset managers can use it as a quick reference when reviewing a facility’s leasing approach.

| Lease Type | Typical Duration | Flexibility | Typical use |

|---|---|---|---|

| Month-to-month / tenant-at-will | No fixed end date | High | Most common in U.S. self-storage |

| Fixed-term (6–12 mo.) | 6 to 12 months | Lower | Commercial tenants; high-competition markets |

| Hybrid | Initial fixed period | Moderate | Fixed term converting to month-to-month |

Lease type sets the baseline. But default, lien, and rate-change clauses are what shape how much revenue and risk the lease actually carries.

Key legal and financial provisions that drive risk and revenue

After the lease term, the next big drivers of performance are rent increases, fees, and liability allocation. The lease sets the rules for how income changes over time and who carries the risk when something goes wrong.

Rate-escalation clauses, fees, and notice mechanics

Use the rent-increase clause to spell out the notice period, delivery method, and effective date for any increase. A 30-day written notice is common, but the exact rule depends on the jurisdiction and the lease itself.

Pricing clauses shape revenue. Liability clauses help limit downside.

Liability limits, insurance requirements, and retail addenda

Liability and insurance clauses affect claim risk and NOI. Use non-bailee language to make clear that the operator does not take possession or control of stored goods. Add claim caps and waiver language to limit stored-property exposure. Match tenant insurance requirements with the tenant-protection options offered at the facility.

A retail addendum can govern any tenant-protection plan, accessory charges, or other non-rent items the facility offers. Those terms matter in day-to-day operations, and they also come up during buyer review.

How Boat and RV Storage Agreements Differ From Standard Storage Leases

When the collateral is a vehicle, the lease has to do more than assign a space. It needs to cover title, access, and removal.

That’s the big split between a standard storage lease and a boat or RV storage agreement. A standard lease mostly deals with stored goods inside a unit. A vehicle-storage lease has to deal with a titled asset. So the language needs to be more specific.

Boat and RV storage agreements should add terms that standard self-storage leases usually don’t, including title details, access rules, and removal steps. Those clauses matter because they shape default enforcement, liability exposure, and valuation. That’s why these agreements need a separate review, especially for identification, insurance, and abandonment terms.

Titled Vehicles, Insurance, and Vehicle-Specific Liability

Boat and RV agreements should identify the vehicle by make, model, year, and VIN, or Hull Identification Number (HIN) for boats. That ties the lease to the exact asset in storage. If the vehicle is later abandoned or has to be removed, that detail can save a lot of trouble.

The agreement should also require current registration and valid insurance as conditions of occupancy. It should clearly state who bears the risk for theft, damage, and towing. If a vehicle is abandoned, the lease should spell out the removal or towing process and any notice rules that apply before the vehicle is handled. That way, the lease supports lien enforcement and towing without gray areas.

Space Type, Access Rules, and Seasonal Pricing and Occupancy Patterns

Boat and RV storage leases also need operating rules that match the space and the vehicle. Common terms cover:

- Must be operable at move-in

- Fuel limits

- Battery disconnection

- Winterization

- Snow-removal duties

Boat and RV storage also often calls for seasonal pricing and access terms. That makes sense. Demand can shift with the time of year, and move-in and move-out patterns don’t always look like standard self-storage occupancy.

Comparison of Standard Storage and Boat/RV Agreements

The table below shows where vehicle-storage terms split from standard storage leases.

| Factor | Standard Storage Lease | Boat/RV Storage Agreement |

|---|---|---|

| Collateral type | General stored property | Titled vehicle |

| Asset identification | Unit number or space assignment | Make, model, year, VIN/HIN |

| Compliance documents | Basic tenant information | Current registration and valid insurance |

| Operational rules | General storage rules | Must be operable at move-in, fuel limits, battery disconnection, winterization |

| Removal/disposition | Standard default language | Specific abandoned-vehicle or towing procedures |

| Pricing pattern | More stable, recurring unit demand | Often uses seasonal pricing or billing terms |

Buyers and asset managers should review boat and RV lease language separately from standard unit leases. The underwriting, liability, and day-to-day issues are different enough that rolling them together can create avoidable risk. These terms can shape recoverability, downtime, and underwriting, often requiring sensitivity testing to account for seasonal occupancy shifts.

How to Evaluate and Improve a Facility’s Lease Package

A lease package has a direct impact on rent collection, default enforcement, and buyer due diligence. A solid lease review turns those terms into a practical checklist that owners, buyers, and asset managers can actually use.

Lease Review Checklist for Owners, Buyers, and Asset Managers

Start with the clauses that have the biggest effect on cash flow and enforcement.

- Base rental agreement: Make sure the lease structure fits the facility’s current occupancy model and matches the language used in the current template.

- Lien and default language: Check that default timing and lien rights line up with state law, plus the facility’s actual notice and default process.

- Rate-escalation clauses: Look for clear notice mechanics and automatic pricing authority. If the language is vague, rate changes can turn into a headache fast.

- Insurance requirements: Make sure the lease clearly covers tenant insurance and liability allocation.

- Boat/RV lease terms: If the facility stores boats or RVs, review those agreements on their own. Titled property, vehicle-specific liability, insurance, access rules, and seasonal rate management need separate attention.

How Cleaner Lease Language Can Support Value

When the lease is clean and enforceable, underwriting cash flow gets much easier. It also helps protect value during a sale or refinance. Weak lease language can increase collection risk, dispute risk, and due diligence friction. Stronger leases help tighten the rent roll and make underwriting more dependable.

The good news: improving lease language usually doesn’t mean pushing out current tenants. Most facilities can update the standard lease template for new agreements and phase in stronger terms as units turn over.

Key Takeaways

Rate-escalation clauses and lien rights are the lease terms that most directly affect property performance and revenue management. Boat and RV storage agreements also need a separate review. Titled property, insurance, access rules, and seasonal rate management are different enough that folding them into a standard lease audit can create avoidable risk.

FAQs

Which lease structure gives owners the most pricing flexibility?

Month-to-month lease structures usually give owners the most room to change pricing. Because the terms are short, rates can be adjusted more often based on market conditions, occupancy, and demand.

As Nolen Masserman, Managing Director at Oakside, notes, tenants in high-occupancy facilities generally have less bargaining power, making month-to-month leases a practical starting point for rate increases.

What lease clauses matter most when reviewing a self-storage facility?

The lease clauses that matter most are the ones tied to steady revenue and day-to-day control.

Pay close attention to month-to-month agreements, existing customer rate increase (ECRI) clauses, and delinquency and default provisions.

These terms give owners room to adjust pricing as market demand shifts, move in-place rents closer to market rates, and keep collections on track. When lease terms are standardized, it also becomes easier to support steady rent growth, property value, and the occupancy levels lenders expect.

Why do boat and RV storage agreements need separate lease terms?

Boat and RV storage agreements need their own lease terms because they don’t work like standard self-storage.

The setup is different from the start. These properties need to deal with parking layout rules, including 50–60-foot drive aisles for 90-degree parking, plus the ups and downs of seasonal demand.

There’s also a different risk mix. Local HOA rules can limit how vehicles are stored, and today’s larger rigs take up more room than many older sites were built for. Specific lease terms help protect the asset and make day-to-day expectations clear for both owners and tenants.