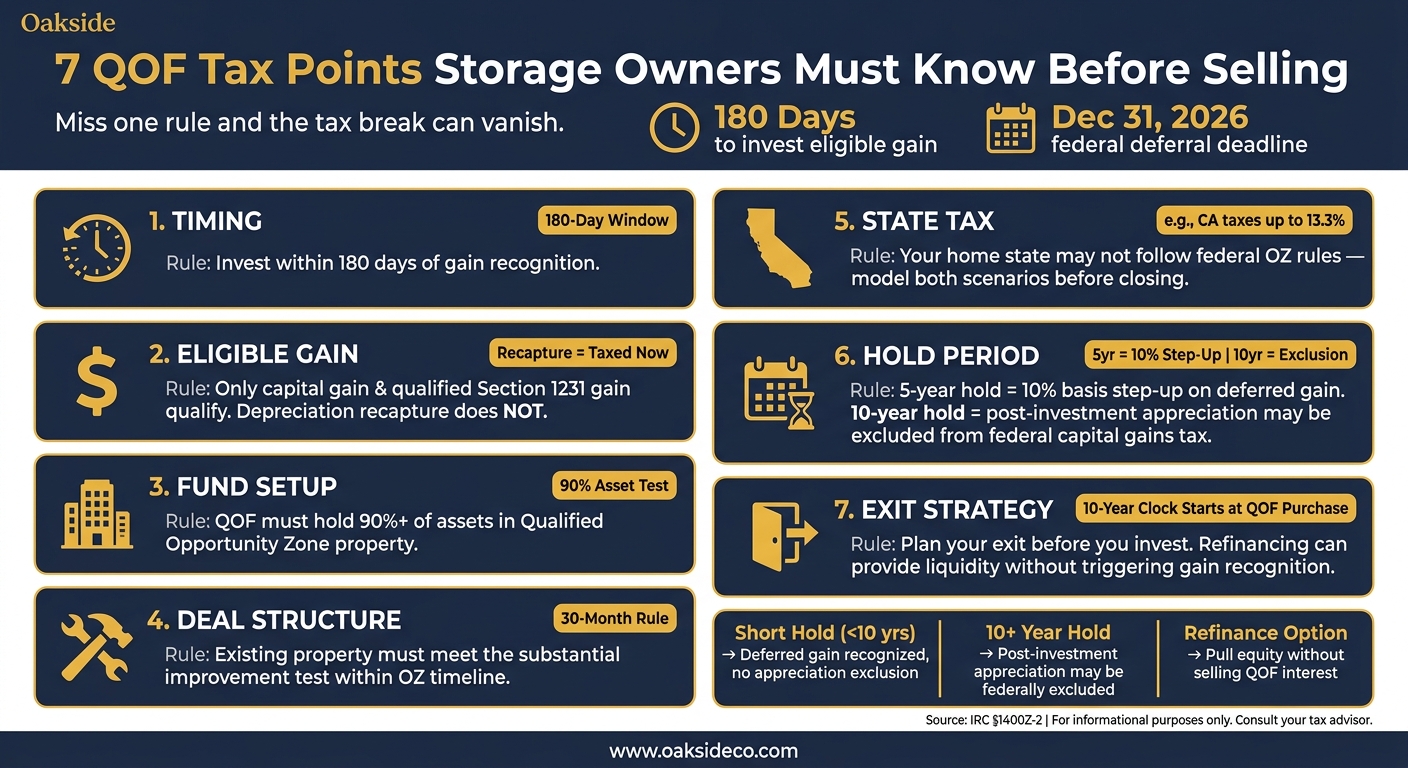

If I sell a storage, boat, or RV asset in 2026, the tax break only works if I get the timing, gain type, fund setup, state tax, hold period, and exit right. The biggest dates are simple: I usually have 180 days to invest eligible gain into a QOF, and deferred federal gain is generally taxed no later than December 31, 2026.

Here’s the short version:

- I can defer eligible capital gain, not all sale proceeds

- Depreciation recapture is taxed now

- The QOF investment must be equity

- A fund must meet its own tax tests, including the 90% rule

- State tax may still apply, even if federal tax is deferred

- A 5-year hold may cut deferred gain by 10%

- A 10-year hold may wipe out tax on post-investment growth

That means I need to answer seven questions before I invest:

- Did I meet the 180-day deadline?

- Is my gain actually eligible?

- Is the fund structure clean enough to support the tax treatment?

- Will the property meet the improvement rules?

- Does my home state follow the federal OZ rules?

- Can I hold long enough to keep the main tax break?

- What happens if I need cash before year 10?

7 QOF Tax Points for Storage Owners: Key Rules at a Glance

Quick Comparison

| Tax point | What I need to check | Why it matters |

|---|---|---|

| Timing | Invest within 180 days of gain recognition | Miss it, and deferral is gone |

| Eligible gain | Only capital gain and some Section 1231 gain count | Recapture does not qualify |

| Fund setup | QOF must meet OZ tests | Bad setup can sink the tax result |

| Deal setup | Rehab or new build must fit OZ rules | Property-level failure can spoil the deal |

| State tax | My state may not follow federal law | I may still owe state tax now |

| Hold period | 5 years and 10 years change tax result | Early sale can trigger tax |

| Exit | Sale, refinance, or early liquidity | The wrong exit can cost the main upside |

I read the article as a warning more than a pitch: the tax idea is simple, but the rules are not. If I’m looking at a sale, I’d want the tax math and the deal plan lined up before closing.

Why Opportunity Funds Matter for Storage Owners

Self-storage and boat/RV properties often gain a lot of value over a multi-year hold. So when an owner sells or recapitalizes one of these assets, the capital gain can be large. And that gain may set off federal capital gains tax, Net Investment Income Tax (NIIT), and, in some cases, state capital gains tax in the year of sale. That’s why timing is the first thing to look at.

For owners sitting on large, illiquid gains, the idea is pretty simple: with a big storage sale, the draw is the chance to defer tax on eligible gain while moving that capital into a qualifying long-term project.

For large self-storage or boat/RV dispositions, QOFs can leave more capital available for reinvestment and long-term growth.

If you’re facing a sale or recapitalization, Oakside Co can help model gain exposure, test timing, and line up the deal with QOF rules. Next comes the 180-day investment window.

1. Review the 180-Day Investment Window

The timeline usually starts when the gain is recognized for federal income tax purposes. In most direct sales, that means the closing date starts the clock. Under IRC §1400Z-2, you generally have 180 days from that recognition date to invest an eligible capital gain into a Qualified Opportunity Fund (QOF) and defer federal tax.

Things can get a little more nuanced with partnership or LLC gains. The start date may shift based on who makes the deferral election and which taxpayer reports the gain. That extra timing room can be helpful if you’re trying to line up your gain with a fund’s capital call schedule.

That said, the 180-day rule is just the front door. The QOF still has to pass its own compliance tests, including the rule that it must hold at least 90% of its assets in Qualified Opportunity Zone property. Before you put money in, check that the fund has a realistic plan to deploy capital within your deadline and stay on track with its own testing dates. After that, the next step is figuring out whether the gain itself qualifies.

2. Confirm Which Capital Gains Actually Qualify

Eligible gain can include capital gain and qualified Section 1231 gain from a storage sale, boat/RV asset sale, business interest sale, or another appreciated capital asset. Both short-term and long-term capital gains can qualify. And gross Section 1231 gains may qualify without netting them against Section 1231 losses.

One big carveout: depreciation recapture under Sections 1245 and 1250 does not qualify.

If you’re selling a storage facility with a lot of accumulated depreciation, the result is often split in two:

- The capital gain piece may be eligible for QOF deferral

- The recapture piece is taxed now at ordinary income rates

That split shows up a lot in storage sales where depreciation has piled up over time. So the amount you put into the QOF should match only the eligible gain, not the full cash proceeds from closing.

After you separate eligible gain from recapture, look at two more limits. Gains from a sale to a related buyer don’t qualify. And the QOF investment must be equity, not debt. There is no dollar cap on eligible gain.

Next, compare fund structures.

3. Compare Qualified Opportunity Fund Structures

QOF structure affects compliance, state reporting, and exit. For storage owners, the usual setups are single-asset, multi-asset, and sponsor-led QOFs. That last option rolls several deals into one sponsor-managed platform. Eligible gain only helps if the fund can hold it and put it to work without a mess. And the structure choice also sets up the next issue: whether the property can meet the substantial improvement rules.

Then look at how the QOF owns the property. In a direct structure, the QOF itself owns the storage property. In an indirect structure, the QOF owns an interest in a lower-tier Qualified Opportunity Zone Business, or QOZB, which owns and runs the facility. The QOZB works under a lower 70% tangible property test, plus extra operating rules, including limits on financial assets and intangible use. So while the indirect path can give you more room on the property test, it also adds another layer of rules to watch.

Structure also affects your sale after 10 years. With a single-asset fund and a set business plan, a 10-year hold can preserve the exclusion for post-investment gain. Multi-asset funds are less clean on timing because assets may sell at different points. That makes exit planning less certain and pushes more attention to the property-level rules in the next section.

Here’s the quick trade-off view.

| Structure | Control | Compliance Test | Exit Simplicity |

|---|---|---|---|

| Single-asset QOF (direct) | High | 90% QOZBP at fund level | More straightforward 10-year exit planning |

| Single-asset QOF (indirect/QOZB) | High | 70% tangible property at QOZB level | Clear, but with more entity layers |

| Multi-asset / sponsor-led QOF | Lower | Varies by asset; monitored by sponsor | Less predictable; sales at different times |

Next, test the deal against the substantial improvement rules.

4. Check the Deal Structure and Improvement Rules

If a QOF buys an existing storage property, it has to substantially improve the building within the Opportunity Zone timeline. That means the rehab budget and the closing date need to line up with that test before you put money in.

This is where timing can make or break the deal. The test turns on both the budget and the clock, so set the improvement budget before closing to help keep the deal eligible. If the work plan can’t meet the substantial improvement test, the deal can lose QOF treatment.

After the deal structure clears the improvement test, check state conformity before funding.

sbb-itb-09b4138

5. Review State Tax Conformity Before You Invest

Before you fund the QOF, check whether your home state follows the federal OZ rules. This step can make or break your after-tax return, so it belongs in your underwriting before you commit capital.

States usually fall into four buckets: full conformity, limited conformity, nonconformity, and no state income tax.

| State Treatment | What It Means for Storage Owners |

|---|---|

| Full conformity | State mirrors federal deferral and potential exclusion |

| Limited conformity | Benefits may apply only to in-state OZ investments or certain taxpayer types |

| Nonconformity | State taxes the deferred gain regardless of federal treatment |

| No state income tax | State conformity is largely irrelevant; focus stays on federal benefits |

Here’s the plain-English version:

- In a fully conforming state, you can usually defer both federal and state tax on the eligible gain.

- In a nonconforming state, you may still owe state tax in the year of the sale, even if the gain is deferred at the federal level.

California is a good example of why this matters. California has not adopted the federal OZ deferral or exclusion rules, and it generally taxes capital gains as ordinary income at rates up to 13.3%.

For most individual investors, the key issue is your home state, not the state where the project sits. So even if the QOF investment is in a conforming state, a nonconforming home state can still tax the gain.

Before closing, run both models:

- one with full federal and state benefits

- one with federal benefits only

That spread can change the deal’s IRR in a meaningful way, and it needs to be built into underwriting before closing.

6. Plan Around the Required Hold Period

After state tax treatment, the hold period is what decides how much of the federal tax break you keep. It affects when your original deferred gain becomes taxable and whether any growth after the investment can stay free from federal capital gains tax.

A 5-year hold gives you a 10% basis step-up on the deferred gain. A 10-year hold can let you exclude post-investment appreciation from federal capital gains tax. For a storage owner, that can cover gains tied to rent growth, better operations, and cap-rate compression over time.

An early exit can be costly. If you sell, gift, or otherwise dispose of your QOF interest before the 10-year mark, the deferred gain is recognized. And if you exit before year 10, you lose the appreciation exclusion. That shifts the focus to exit planning, because timing here can mean a big tax bill versus none on the added growth.

The 10-year hold is what protects post-investment appreciation. In a well-run storage facility, that’s often where the biggest tax-free upside sits.

7. Map the Exit Strategy Before Closing

The last test is the exit. Plan that exit before you invest, because QOF tax treatment depends on how long you hold the investment and when you need cash.

The 10-year clock starts when you buy the QOF interest. It does not start when the property is bought or when it’s placed in service. So if your plan includes a value-add stretch and then a stabilization period, your target sale date needs to land at or after the 10-year mark.

Before you put money in, run at least two exit cases side by side. One should assume you hold the QOF interest for 10+ years and aim for the federal capital gains exclusion on post-investment gains. The other should assume you need liquidity sooner and have to exit early.

Use the three paths below to stress-test liquidity, tax timing, and downside risk before closing.

| Exit Scenario | Federal Tax Outcome | Key Risk |

|---|---|---|

| Hold 10+ years, sell QOF interest | Post-investment appreciation may be excluded from federal capital gains tax. | Requires patient capital |

| Exit before 10 years | Deferred gain is recognized, and appreciation is not excluded. | Loss of the main federal tax benefit |

| Refinance while holding | Cash can be raised without selling the QOF interest. | Must be structured carefully to avoid an inclusion event |

Think of refinancing as a liquidity tool, not a full exit. If there’s a chance you’ll need cash before year 10, a refinance after lease-up may let you pull out equity while keeping the QOF interest in place.

Opportunity Fund Structure at a Glance

Once you’ve looked at timing and exit planning, the next step is structure. And this part matters more than it may seem at first glance.

These four choices do a lot of the heavy lifting when it comes to tax treatment. Pick one path instead of another, and the compliance rules, holding period math, and state tax result can change in a big way.

| Structure Choice | Option A | Option B | Key Tax-Planning Implication |

|---|---|---|---|

| Ownership layer | Direct QOF ownership of property | QOF invests through a lower-tier QOZB | Direct ownership keeps the 90% fund test at the QOF level; a QOZB shifts compliance to the operating business. |

| Development path | Ground-up development (original use) | Substantial improvement of existing facility | Ground-up development avoids the improvement test; existing property must meet the 30-month substantial-improvement rule. |

| Hold period | Shorter hold (under 10 years) | 10-plus-year hold | A short hold defers gain; a 10-plus-year hold can exclude post-investment appreciation via a basis step-up at exit. |

| State tax exposure | State follows federal rules | State decouples from federal rules | States that follow federal treatment allow deferral and potential exclusion; states that decouple may tax the gain in the year of sale regardless of federal treatment. |

A simple way to think about it: one choice affects where compliance sits, another affects how the property qualifies, another affects when tax may hit, and the last one affects whether your state follows the same playbook as the IRS.

If you’re weighing direct ownership against a lower-tier QOZB, ground-up development against rehab, or a short hold against a 10-plus-year hold, you’re not just picking a deal shape. You’re picking the tax rules that come with it.

Conclusion

Opportunity Funds can defer tax on eligible storage and boat/RV sale gain, but only when the details line up: timing, eligibility, fund structure, state rules, and exit plans. Miss just one rule, and the tax break can vanish.

And even if the tax side works, the deal still needs to make sense as a plain business investment. The asset has to stand on its own. That means looking hard at location, demand, competition, day-to-day operations, and long-term value.

That’s why the tax plan and the transaction plan need to move in step. Bring in your tax advisor, legal counsel, and Oakside Co early so the QOF plan matches your deal timing and exit goals. These rules are technical and time-sensitive, so early guidance and steady monitoring matter.

FAQs

How do I calculate my eligible gain?

Start with the capital gain from selling your storage facility. That’s the difference between the sale price and your adjusted cost basis.

You’ll also want to account for depreciation recapture, which can push your taxable gain higher. And don’t lump every asset together. Separate the real property assets from non-qualifying business assets, because only the real property portion will usually qualify for tax-advantaged reinvestment strategies.

What counts as an inclusion event before year 10?

An inclusion event is any transaction or action that makes previously deferred capital gains from an Opportunity Fund investment taxable.

In plain English, it’s the moment the IRS says: you have to recognize those gains now.

This can happen if you sell your interest in the fund or if the fund sells the underlying asset before the 10-year holding period ends. As Nolen Masserman, Managing Director at Oakside, notes, early exit planning mistakes can reduce the intended tax benefits.

How do I know if my state follows OZ rules?

It depends on your state’s tax code. States don’t automatically follow federal Qualified Opportunity Zone (QOZ) tax treatment.

Talk with a tax advisor to see whether your state offers full, partial, or no conformity. If your state doesn’t conform, you may still owe state taxes on gains that are deferred for federal tax purposes.