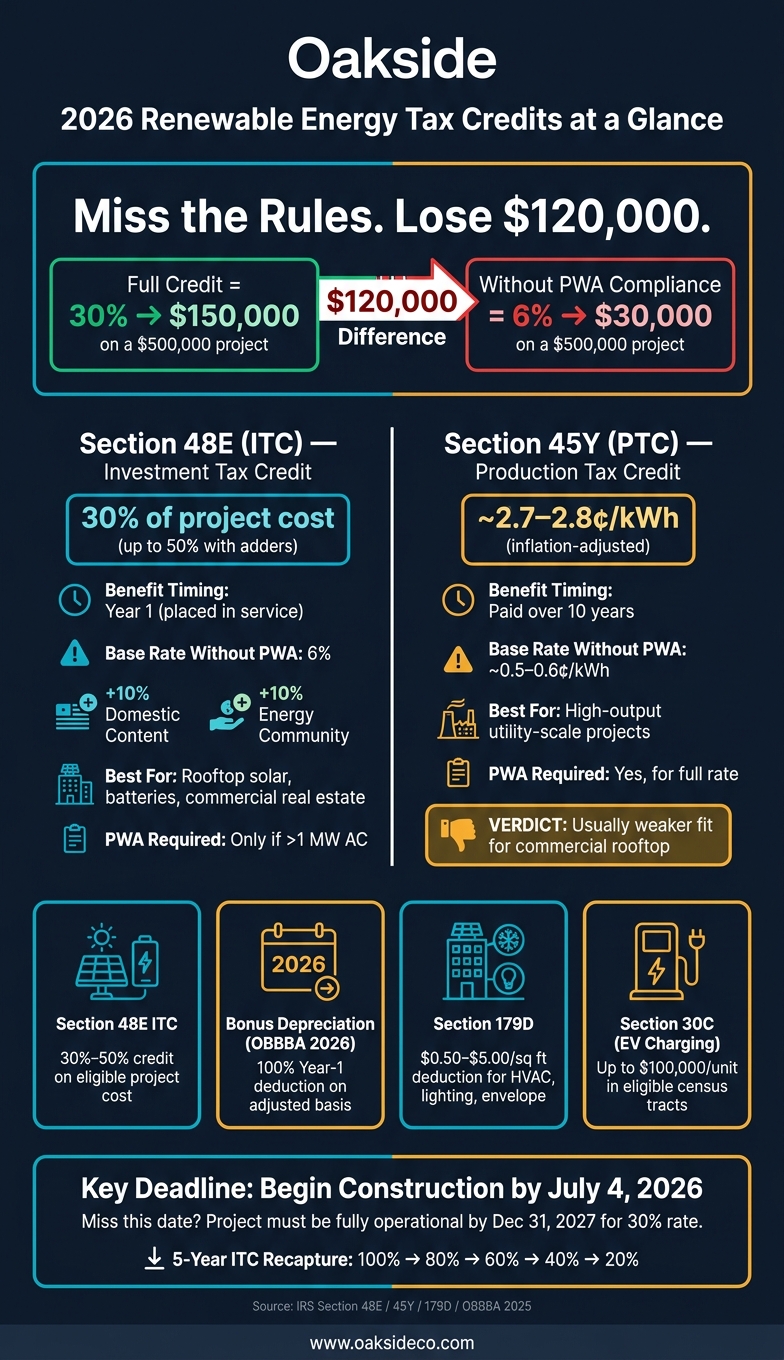

If I’m planning a commercial solar, battery, lighting, HVAC, or EV charging project in 2026, the biggest issues are simple: start on time, use the right credit, and keep the paperwork clean. For many owners, the top federal credit is still 30%, but missing labor, sourcing, or timing rules can drop that to 6%. On a $500,000 project, that is a swing of $120,000.

Here’s the short version:

- I can usually choose between Section 48E and Section 45Y

- For many commercial rooftop solar projects, 48E is the better fit because it gives the credit upfront

- The main deadline is July 4, 2026, to begin construction under the current rules

- Bonus depreciation is 100% in 2026 for solar property under the article’s cited OBBBA rule

- Section 179D may also apply for lighting, HVAC, and building envelope work

- State rebates, grants, and utility programs can help, but some of them reduce federal credit basis

- The ITC has a 5-year recapture period if the asset is sold or stops qualifying

If I own self-storage or boat/RV property, the fit can be strong because these sites often have large roofs, steady power use, and common-area loads. That can make solar, storage, and building upgrades pencil out better when I model credits, deductions, and depreciation together.

2026 Renewable Energy Tax Credits: Section 48E vs 45Y & Key Incentives Compared

Quick comparison

| Item | What it does | 2026 headline point |

|---|---|---|

| Section 48E | Credit based on project cost | 30% with full rules met; often the top choice for commercial rooftop solar |

| Section 45Y | Credit based on power produced | Paid over 10 years; often a weaker fit for these property types |

| Section 179D | Deduction for building upgrades | Applies to lighting, HVAC, insulation, windows, doors, roofing |

| Bonus depreciation | Year-1 deduction on adjusted basis | Article states 100% for 2026 solar property |

| State / utility incentives | Rebates or performance payments | Can help returns, but some rebates cut ITC basis |

| Section 30C | EV charging credit | Limited to eligible census tracts and capped per unit |

The bottom line: if I want the full tax upside in 2026, I need to line up construction start, labor records, sourcing support, basis calculations, and placed-in-service timing before work begins.

sbb-itb-09b4138

Federal Clean Energy Credits Available in 2026

The two main federal credits for commercial property owners in 2026 are Section 48E and Section 45Y. Section 48E is the Clean Electricity Investment Tax Credit, and Section 45Y is the Clean Electricity Production Tax Credit. These credits replaced older, technology-specific programs starting in 2025 and 2026. They now apply to facilities that generate electricity with zero or near-zero greenhouse gas emissions.

For most self-storage and boat/RV properties, the job is pretty simple: match the project to the credit that fits best.

Section 45Y vs. Section 48E for Commercial Properties

Here’s the plain-English version: Section 48E cuts tax liability in the year the project is placed in service because it’s based on a percentage of eligible project cost. Section 45Y cuts tax liability over a 10-year period because it’s tied to how much electricity the system produces.

For most self-storage and boat/RV owners, 48E is usually the better fit. These properties tend to have moderate electricity output compared with what the project costs to build. So an upfront credit based on project cost often beats a per-kilowatt-hour credit paid out over 10 years.

The big line in the sand is Prevailing Wage and Apprenticeship (PWA) compliance. If you meet PWA rules, the credit can be 30%. If you miss them, the base rate drops to 6%. On a $500,000 project, that difference equals $120,000.

For projects larger than 1 MW AC, PWA compliance is required to get the full credit. Many self-storage rooftop systems stay under 1 MW AC, which usually means they are exempt from PWA rules while still qualifying for the full 30% rate.

| Feature | Section 48E (ITC) | Section 45Y (PTC) |

|---|---|---|

| Incentive Type | Investment-based (% of cost) | Production-based (per kWh) |

| Full Credit Value | 30% of eligible basis | ~2.7–2.8¢/kWh (inflation-adjusted) |

| Base Rate Without PWA | 6% of eligible basis | ~0.5–0.6¢/kWh |

| Benefit Period | Year 1 (placed in service) | 10 years of production |

| Labor Requirements | PWA required if >1 MW AC | PWA required for full rate |

| Construction-Start Deadline | Begin construction by July 4, 2026 | Begin construction by July 4, 2026 |

| Typical Relevance | High – rooftop solar, batteries, commercial real estate | Low – better for projects with high annual output |

Bonus adders can push the ITC past 30%. Meeting domestic content rules adds 10%, and being in a qualifying Energy Community adds another 10%. That can bring the total credit to 50% or more.

Once the federal credit is set, the next move is to look at deductions and depreciation so you can stack more tax savings.

Solar, Battery Storage, and Other Qualifying Projects

In 2026, the most common qualifying projects for these property types include rooftop solar PV, solar carports or canopy structures, and standalone battery storage systems with at least 5 kWh of capacity. Interconnection costs for projects up to 5 MW AC can also be included in the ITC basis, which can increase the amount of project cost eligible for the credit.

Timing matters just as much as project size now. July 4, 2026, is the key deadline for beginning construction under the current favorable rules.

If a project begins construction before that date, it can use the Continuity Safe Harbor, which gives up to four years to finish the project and place it in service. Miss that date, and the rules get tighter: the project must be fully operational by December 31, 2027, to qualify for the 30% rate.

There’s also a simpler path for smaller systems. For projects under 1.5 MW, spending at least 5% of total project costs before the deadline meets the beginning-of-construction test.

For rooftop solar and storage at self-storage and boat/RV properties, the takeaway is direct: permitting, procurement, and placed-in-service timing all need to line up with the July 4, 2026, construction-start deadline. Starting early is the clearest way to protect credit eligibility.

Deductions, Depreciation, and Combining Benefits

Credits like Section 48E are only part of the picture. Owners can also cut taxable income through deductions and bonus depreciation. When you use these tools together, they can lower the after-tax cost of a project in a big way. The key is simple: sort costs into the right buckets for credits, deductions, and depreciation.

Section 179D for Energy-Efficient Commercial Building Upgrades

Section 179D is a deduction for permanent upgrades to lighting, HVAC, and the building envelope, including insulation, windows, doors, and roofing, measured against ASHRAE 90.1 standards. For self-storage and boat/RV properties, the most likely fits are climate-controlled storage buildings with upgraded HVAC, office areas with LED lighting retrofits, and service bays with better insulation.

The deduction starts at $0.50 to $1.00 per square foot at the base level and increases to $2.50 to $5.00 per square foot when prevailing wage and apprenticeship (PW/A) rules are met.

After you map out building-system deductions, you can layer project-level credits and depreciation onto the remaining basis.

Bonus Depreciation and Stacking Rules with Credits

The basis-reduction rule for the Section 48E ITC is shown in the table below. On a $500,000 solar installation with a 30% ITC, the credit equals $150,000. The depreciable basis is then reduced by $75,000, which leaves $425,000 available for depreciation.

That remaining basis can then be deducted through bonus depreciation. Under the One Big Beautiful Bill Act (OBBBA) passed in 2025, bonus depreciation for solar property placed in service in 2026 is 100%. In plain English, that means the full remaining basis can be deducted in Year 1.

Here’s the order to use:

- Claim the ITC in the year the system is placed in service

- Reduce the depreciable basis by 50% of the credit

- Apply 100% bonus depreciation to the adjusted basis

For building-efficiency work like HVAC or lighting, claim Section 179D on its own. Since 179D applies to building systems and the ITC applies to energy property, you can track the two incentives against separate costs and records. For self-storage and boat/RV projects, that means keeping solar, HVAC, and lighting costs split out in both the project budget and the tax file. It’s not glamorous, but it keeps each benefit stream clean and audit-ready.

| Benefit Type | Code Section | 2026 Benefit | Basis Impact | Typical Use Case |

|---|---|---|---|---|

| Investment Tax Credit | Section 48E | 30%–50% credit | Reduces depreciable basis by 50% of the credit | Solar PV, battery storage, solar-plus-storage |

| Bonus Depreciation | Section 168(k) | 100% deduction for solar property under OBBBA | Recovers remaining adjusted basis | Rapid capital recovery for solar equipment |

| Building Deduction | Section 179D | $0.50–$5.00 per sq. ft. | No impact on ITC basis | HVAC, lighting, envelope upgrades |

State, local, and utility incentives can improve returns even more, but each one comes with its own eligibility rules and filing steps. Next, layer in state, local, and utility programs where the project qualifies.

State Incentives, Eligibility Rules, and Compliance

State, Local, and Utility Incentives That Can Improve Project Returns

State and utility incentives can make a project look a lot better on paper. But there’s a catch: each one can change eligible basis, tax treatment, or both.

Here’s the big split:

- Upfront rebates and grants usually reduce eligible basis, which cuts the federal ITC amount.

- Performance-based incentives often stack with the ITC, but the payments are usually taxable business income.

| State | Technology | Incentive Type | Typical Benefit Structure | Interaction with Federal Benefits |

|---|---|---|---|---|

| New Jersey | Solar PV | SREC-II / SuSI | Fixed-rate certificates for 15 years | Additive; revenue is taxable income |

| California | Storage | SGIP | Rebate based on capacity (kWh) | Reduces eligible basis for ITC |

| Massachusetts | Solar PV | SMART 3.0 | Fixed per-kWh incentive for 10 years | Additive; payments are taxable income |

| New York | Solar PV | NY-Sun | Upfront capacity-based block incentive | Reduces eligible basis for ITC |

| Illinois | Solar PV | Illinois Shines | 15-year SREC contracts | Additive; revenue is taxable income |

| Texas | Solar/Wind | Property Tax Exemption | Exemption on value added by system | No impact on federal basis |

Federal programs matter too, especially for EV charging. Section 30C limits the commercial credit to $100,000 per unit and only applies in eligible low-income or non-urban census tracts.

Once you map the incentives, the next job is simple in theory and painful in practice: prove the project qualifies and keep the credit in place.

Eligibility Requirements and Documentation for Self-Storage and Boat/RV Owners

Getting the credit is one thing. Defending it in an audit is another.

The IRS expects project-level backup, including certified payroll records, apprenticeship logs, and manufacturer certifications for domestic content. A smart move here is to require monthly certified payroll reports in the EPC contract.

| Issue | Impact on Tax Benefit | Recommended Control |

|---|---|---|

| Missing PW/A Records | Credit drops from 30% to 6% | Require certified payroll and apprentice registration cards for all trades in the EPC contract |

| FEOC Equipment Sourcing | Total loss of Section 48E credit eligibility | Obtain supplier chain affidavits for battery cells and minerals before purchase |

| Roof/Structural Costs in Basis | Audit adjustment and interest penalties | Use itemized invoices separating solar equipment from structural work |

| Asset Sale Within 5 Years | Pro-rated recapture of claimed ITC | Include tax credit indemnity and recapture clauses in sale agreements |

| Interconnection Delay | Shifts credit to the following tax year | Match the placed-in-service date to the utility’s Permission to Operate (PTO) letter |

| Ineligible Basis Items | Partial credit denial or recapture | Separate land, financing costs, and routine maintenance from eligible basis calculations |

Prevailing wage and apprenticeship rules can have a major effect on the credit value. If PW/A records are missing, the credit can fall from 30% to 6%. On top of that, apprenticeship rules say that 15% of total labor hours must be done by qualified apprentices.

Timing also matters. The federal ITC has a five-year recapture window. If the property is sold or the system stops qualifying during that period, the IRS can claw back the credit on a sliding scale:

- 100% in Year 1

- 80% in Year 2

- 60% in Year 3

- 40% in Year 4

- 20% in Year 5

That’s why recapture should be built into underwriting from the start.

Keep payroll records, equipment records, invoices, and PTO letters in one file from day one. Also track the construction start date, placed-in-service date, and PTO date in the tax file.

Oakside’s Advisory Perspective and Key Takeaways for 2026 Planning

Using Tax Benefits in Underwriting, Valuation, and Capital Planning

After the tax structure is set, the next step is simple: figure out what it does to underwriting and exit value.

This is where timing matters. Tax incentives do the most work when they’re built into the model before pricing, financing, and design are locked in. For self-storage and boat/RV owners, that can push net project cost down in a big way, which can change how both buyers and lenders look at the asset.

When credits and depreciation are modeled together, solar can cut net cost and improve IRR.

That’s where advisory work starts to matter. It takes tax savings off the page and turns them into deal value. Oakside Co folds incentive modeling into acquisition, repositioning, and disposition analysis, including credit selection, location screening, and documentation planning.

The five-year recapture window also needs to be built into transaction terms from day one.

Conclusion: Key Decisions Owners Should Make Before Starting a Project

Before a project starts, owners should lock four decisions into the pro forma.

- First, choose the credit that fits the project’s size, output, and hold period.

- Second, model credit basis reduction, bonus depreciation, and Section 179D together.

- Third, include state, local, and utility incentives in the pro forma before final pricing.

- Fourth, put documentation and recapture controls in place before construction begins.

That last point can hit hard. If certified payroll records, apprenticeship logs, or equipment sourcing certifications are missing, a 30% credit can fall to 6% – a $96,000 gap on a $400,000 system.

The full 30% ITC window also closes soon. Projects must establish construction commencement by July 4, 2026, using either the Physical Work Test or the 5% Safe Harbor.

FAQs

Which credit is better for my project: 48E or 45Y?

It depends on your project’s financial setup and how the asset will run. 48E is a one-time credit tied to a share of upfront capital costs, so it often makes sense for projects with high up-front spend.

45Y works differently. It’s tied to the electricity the project actually produces during its first 10 years. That can make it a better fit for projects with high capacity factors or strong power output.

As Nolen Masserman, Managing Director at Oakside, emphasizes, cash-flow modeling is key.

What counts as beginning construction before July 4, 2026?

To show construction began by July 4, 2026, you usually need to satisfy one of two IRS-approved tests.

The Physical Work Test means significant physical work must have started. That work can happen on-site or off-site.

The Five Percent Safe Harbor gives projects another path. Under this test, a project can qualify by incurring at least 5% of total project costs through binding commitments or expenditures. This option applies to projects of any size, including those that are 1.5 megawatts or less.

Which incentives reduce my federal tax credit basis?

If you claim the Section 48E Investment Tax Credit, your depreciable basis for MACRS drops by half the credit amount.

Here’s the simple version: if you get a 30% tax credit, your depreciable basis goes down by 15% of the total system cost. That means you can depreciate the remaining 85% of the cost.

That detail matters more than it might seem at first glance. A small mistake in basis calculations can affect the tax outcome in a big way.

As Nolen Masserman, Managing Director at Oakside, notes, precise cost allocation helps maximize benefits while staying compliant with IRS requirements.